By Barry Eichengreen, Project Syndicate | May 11, 2026

NEW YORK—Gold may be a “barbarous relic,” as John Maynard Keynes once observed, but it remains the relic of choice among central banks. Emerging-market central banks have been loading up on gold reserves ever since the 2008 global financial crisis, more than doubling their holdings. Does the anomalous behavior of gold prices since the outbreak of the war with Iran call this strategy into question, or is something else going on?

Gold’s allure derives from its reputation as a safe haven and inflation hedge. Yet in March, following the start of the war, an event that should have supported demand for gold on both grounds, its dollar price fell by 10%. Prices then remained flat in April. Evidently gold is not quite the safe haven and inflation hedge investors thought it was.

Various explanations have been offered for this anomalous behavior. Traders incurring losses on other investments may have sold gold futures and funds to meet margin calls. Higher interest rates, or at least diminished expectations of interest-rate cuts, may have caused investors to shift from gold to bonds. Turkey’s central bank sold gold to obtain the foreign exchange needed to support the country’s currency, the lira. Other central banks may have followed suit.

In any case, this episode is a reminder that gold prices can be volatile. So, should central bankers re-think their investment strategies?

Consider why central banks hold gold. Holding bullion has history on its side, having long been a sign of respectability for central banks. Any global investor will want to include in its portfolio a “commodity play,” an investment correlated with commodity prices. Being long on gold is one way to obtain this exposure, although in a world with commodity and future ETFs there are other instruments offering better combinations of risk and return.

The most important factor, though, is that gold kept at home is free of sanctions risk. Foreign-exchange reserves held as bank deposits and securities abroad are at risk of being immobilized, or even garnished, by a foreign government using sanctions for deterrence purposes, as Russia was reminded following its attack on Ukraine in 2022.

Russia was not unaware of the danger: the share of its foreign reserves held in gold more than doubled from 2014, just prior to its annexation of Crimea, to its full-scale invasion of Ukraine in 2022. It repatriated all of it, vaulting it in St. Petersburg and Moscow.

The People’s Bank of China has been less forthcoming about its gold operations but is thought to have been the single most important central-bank purchaser in recent years. The PBOC is thought to store the vast majority of that gold in Beijing and Shanghai, presumably because it is cognizant of sanctions risk.

My own research with co-authors suggests that the pattern is general: exposure to US financial sanctions significantly increases the share of reserves that emerging and developing economies hold in the form of gold. More generally, the largest central-bank gold purchases in recent years have been by countries that are significantly exposed to geopolitical risk, not just Russia and China but also Poland, India, and—before last March—Turkey.

A further indication of what central banks are thinking is that the share of official gold reserves held in custody at the Federal Reserve Bank of New York has fallen from 30% of the global total in 2005 to barely 20% today. Policymakers in other countries are questioning whether the US is a reliable ally and whether the New York Fed is a reliable custodian. Recent reports link popular pressure for gold repatriation in Germany and Italy to political tensions with the United States and threats to the Fed’s independence. Who would have thought?

But gold vaulted at home can’t be lent, swapped, or posted as collateral, unlike gold vaulted in London and New York. It is clunky when used for payments. In 2019, Venezuela’s government, subject to US sanctions, chartered a Boeing 777 from a Russian company to ferry 7.4 tons of gold to Uganda, where it was refined and resold. Venezuela received $300 million worth of euros to pay for merchandise that would have been unavailable to the country otherwise.

Venezuela did it again in 2020, paying for oil-field equipment and services from Iran, also sanctioned, by hiring a fleet of 747s to transport gold bars. These operations, complex and unwieldy, were exceptions that proved the rule.

In this sense, central-bank purchases and repatriation of gold are a symptom of deglobalization. They signal the advent of a more geopolitically fragmented world in which cross-border transactions of all kinds are poised to become more difficult and costly.

Barry Eichengreen, Professor of Economics and Political Science at the University of California, Berkeley, is a former senior policy adviser at the International Monetary Fund. He is the author of many books, including Money Beyond Borders: Global Currencies From Croesus to Crypto (Princeton University Press, 2026).

Copyright Project Syndicate

👉 Show & Tell 🔥 The Signals

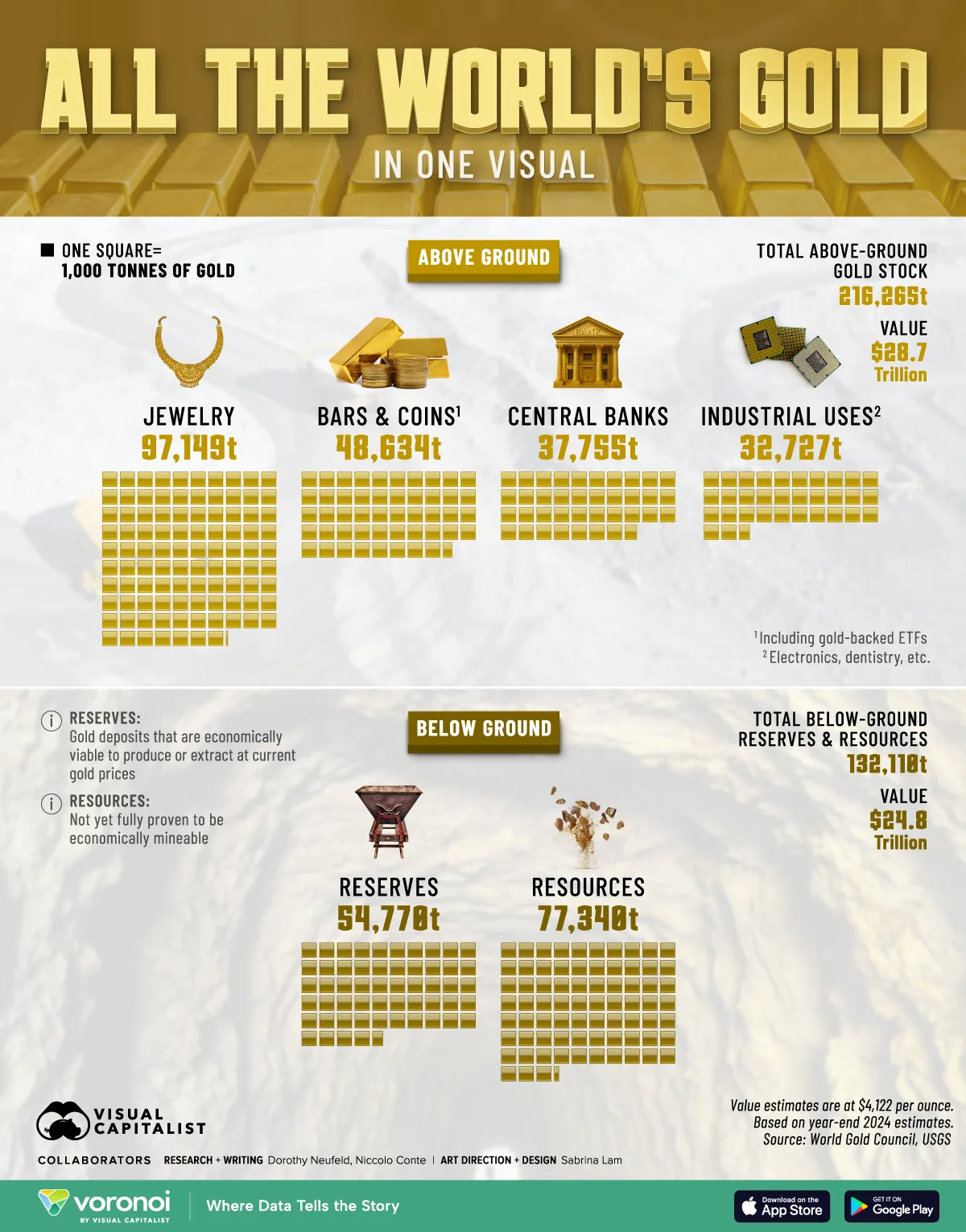

I. Gold Above Ground Is Worth Nearly $29 Trillion

An estimated 216,265 tonnes of gold exist above ground globally, valued at roughly $28.7 trillion. Nearly half is held in jewelry, while central banks now control more than 37,000 tonnes as nations continue rebuilding gold reserves.

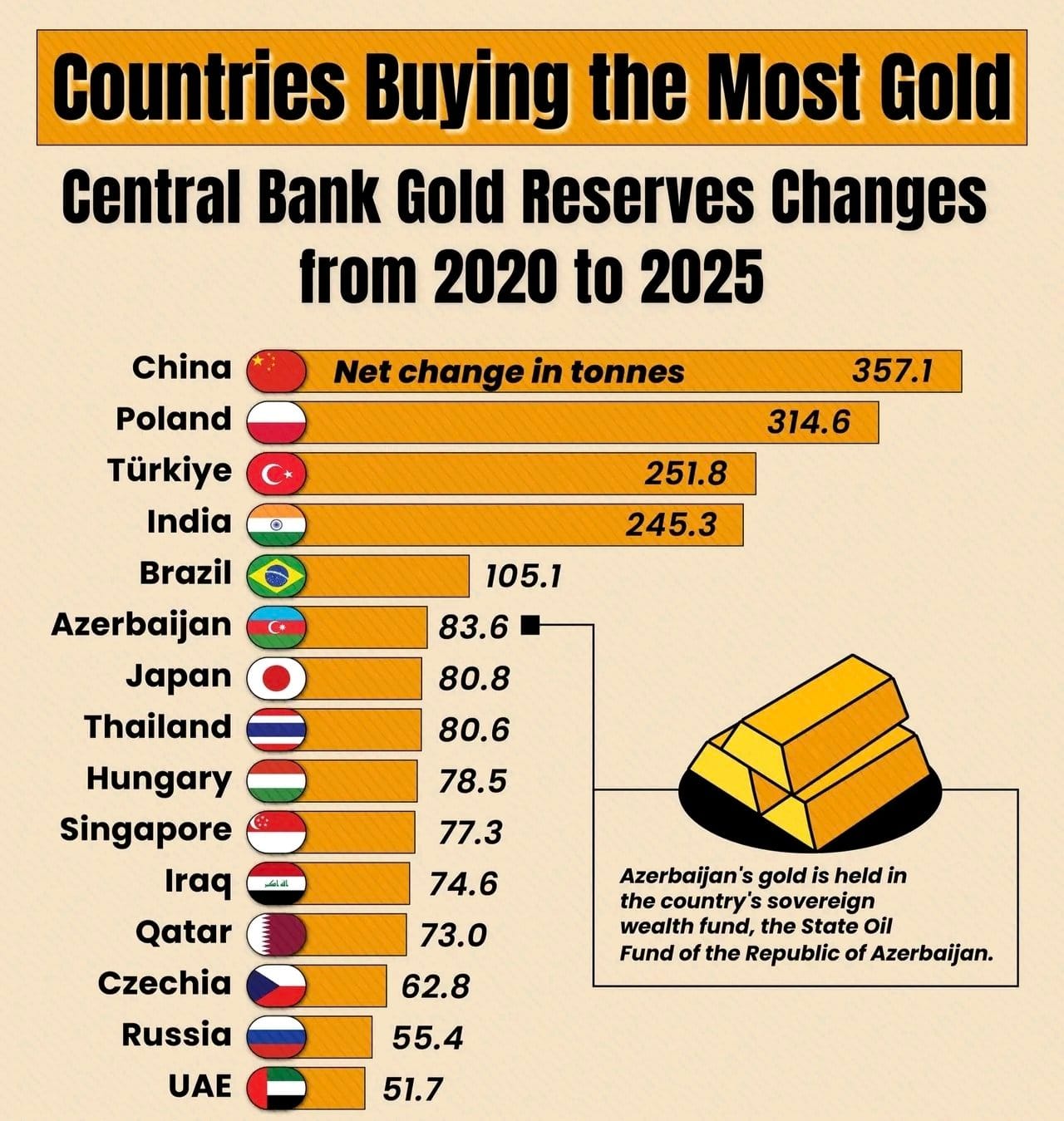

II. China Leads Global Central Bank Gold Buying

China added an estimated 357 tonnes of gold reserves between 2020 and 2025, the largest increase in the world. Poland, Türkiye, and India also made major additions as central banks accelerated diversification away from fiat reserve assets.

📊 Market Mood — Wednesday, May 13, 2026

🟩 Markets are steady for now, but investors remain uneasy as President Donald Trump heads to China with the Iran conflict and trade tensions hanging over the talks.

🟧 Inflation fears are back in focus after another strong CPI reading, with higher oil prices and the Strait of Hormuz disruption raising concerns about a broader global energy shock.

🟦 Treasury yields are climbing as traders scale back hopes for Fed rate cuts and begin pricing in the risk of future hikes if inflation stays elevated.

🟨 Oil eased slightly Wednesday but remains above $100 a barrel as investors doubt a near-term breakthrough between Washington and Tehran.

🗓️ Key Economic Events — Wednesday, May 13, 2026

🟧 8:30 a.m. ET — Producer Price Index (PPI) (April)

Forecast: +0.5% month over month vs. +0.5% previous. Markets will watch whether wholesale inflation is accelerating further after recent energy-driven price pressures.

🟧 10:30 a.m. ET — Crude Oil Inventories

Forecast: -2.0M barrels vs. -2.313M previous. Another inventory draw could reinforce concerns about tight global oil supplies amid Middle East tensions.

🟧 1:00 p.m. ET — 30-Year Treasury Bond Auction

Previous yield: 4.876%. Investors will watch demand closely as rising inflation fears push long-term Treasury yields higher.

Letters to the editor email: editor-tippinsights@technometrica.com

Subscribe Today And Make A Difference. Consider supporting Independent Journalism by upgrading to a paid subscription or making a donation. Your support helps tippinsights thrive as a reader-supported publication. Contact us to discuss your research or polling needs.

Reach our audience. For sponsorship and advertising opportunities, visit our Partner With Us page.