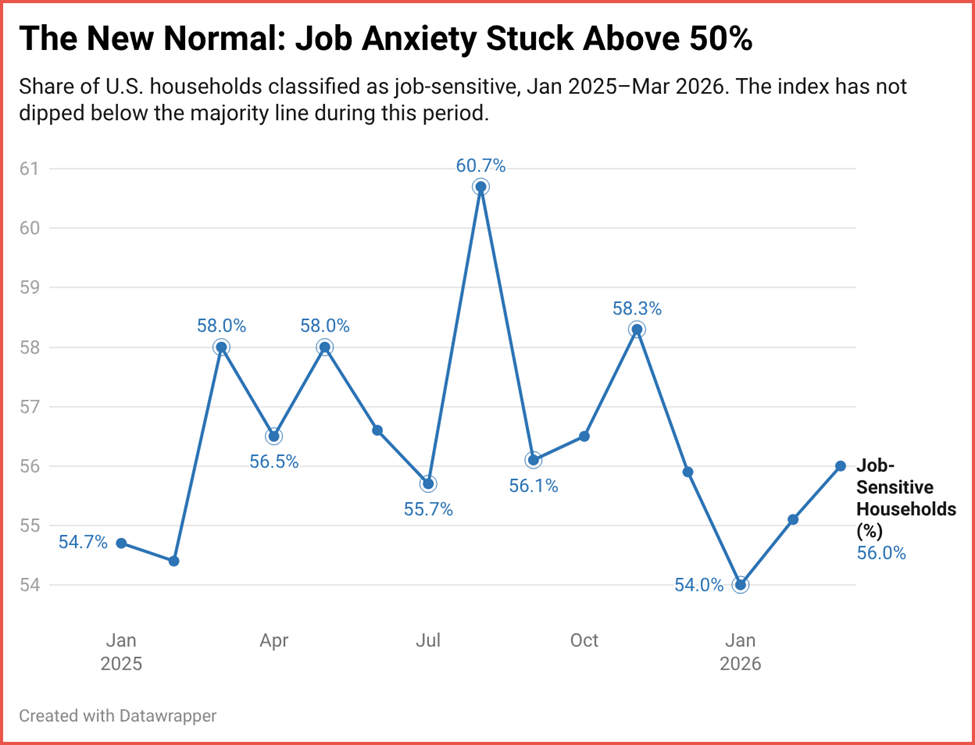

Here’s a number that should bother you: 56%.

That’s the share of American households in March 2026 that qualify as “job sensitive” in the TIPP Poll, meaning someone in the house is out of work and looking, or someone is worried about getting laid off in the next year, or both. Most American families have been in this position for 15 straight months.

What stands out most in the data isn’t the level. It’s the stubbornness. Since January 2025, the reading has bounced between 54% and 61%, not once dropping below the halfway mark. In August 2025, it spiked to nearly 61%. By this January, it dipped to 54%. Then it climbed right back. The national average over this fifteen-month stretch is 56.4%.

If you’re used to watching the official unemployment rate, which looks pretty tame, this might seem off. But the TIPP Job Sensitivity Index measures something the BLS doesn’t: the texture of household economic life. A family where Dad is working but Mom has been searching for three months, where a twenty-something kid just moved back home because his contract ended, and where rumors of a company restructuring have everyone on edge. That family shows up in these numbers even if no one in it counts as “unemployed” under the government’s definition.

Look at the chart above. That line barely moves, and that’s the story. This isn’t sudden. It’s been building, and it’s not easing.

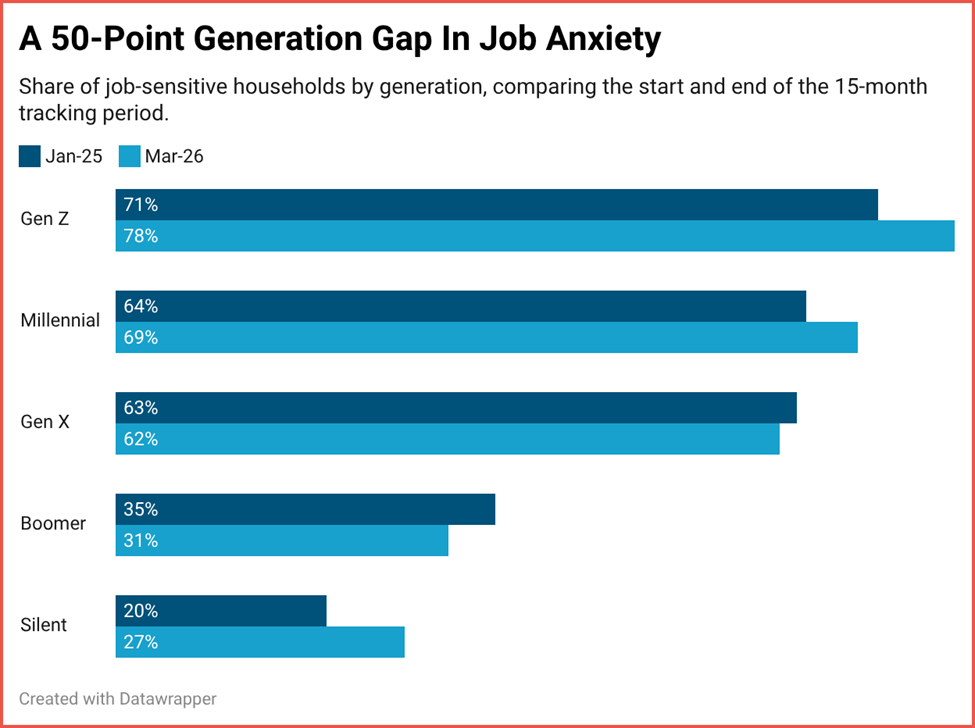

America’s Youth Are Living in a Different Economy

If you’re over 65 reading this, your experience of the job market is almost unrecognizably different from your grandchildren’s. Just 24% of households headed by someone 65 or older qualify as job sensitive. For 18-to-24-year-olds, it’s 81%.

Read that again. Four out of five young-adult households are either dealing with unemployment or dreading a layoff. And it’s getting worse, not better, up from 71% in January 2025.

The Gen Z number is 78%. Millennials are at 69%. Even Gen X (people in their mid-40s to late 50s), supposedly in their peak earning years, come in at 62%. Only once you get to Boomers does the figure drop below the majority line, at 31%. The Silent Generation sits at 27%.

The staircase effect in the generational data is glaring. Each younger generation is markedly more anxious than the one before it, and the gap between Gen Z and Boomers has actually widened over the past fifteen months. This is not just about young people being dramatic. Nearly a third of 18-to-24-year-olds report two or more people in their household actively job hunting. These households are living on the edge.

Know someone who should be reading TIPP Insights? Forward this email. Sponsor inquiries: editor-tippinsights@technometrica.com

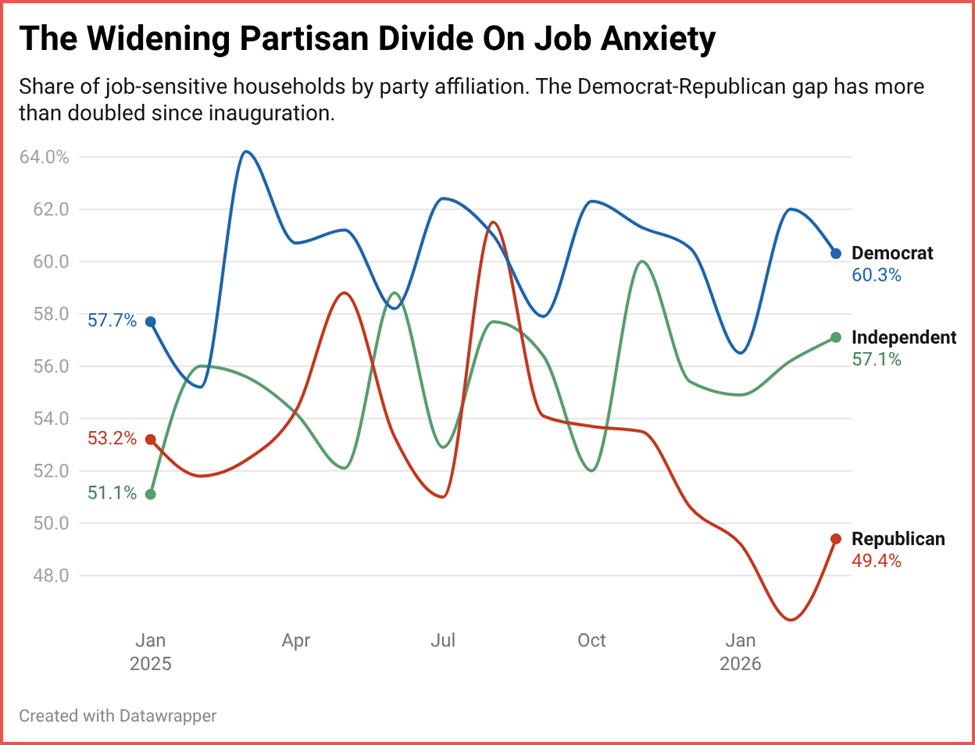

Democrats and Republicans Are Drifting Apart. Fast.

When President Trump took office, the partisan gap in job sensitivity was small enough to ignore: 58% of Democratic households versus 53% of Republican ones. A gap of 4.5 points. Today it’s nearly 11 points, and in February it briefly hit 16.

What’s happening is a two-way movement. Republicans are feeling better. Their job sensitivity has dropped from 53% to 49%, and the share of Republicans who say they’re “very concerned” about layoffs has fallen from 18% to just 12%, the lowest in the fifteen-month series. Democrats, meanwhile, aren’t budging. Their concern about layoffs has bounced between 33% and 45% with no meaningful improvement. Independents have drifted toward the Democrats, sitting at 57% today, up from 51% at the start.

The political science literature has a name for this: partisan economic perception. People tend to feel better about the economy when their team controls the White House. We know this. But it’s one thing to see it on a consumer confidence survey and another to see it on a concrete household measure. When Republicans report less job anxiety, is it because their actual employment situation improved, or because they feel more optimistic under a Republican president? The data can’t tell us. But the magnitude of the swing, especially on “very concerned,” which dropped by a third among Republicans, leans toward perception doing some heavy lifting.

The Familiar Fault Lines

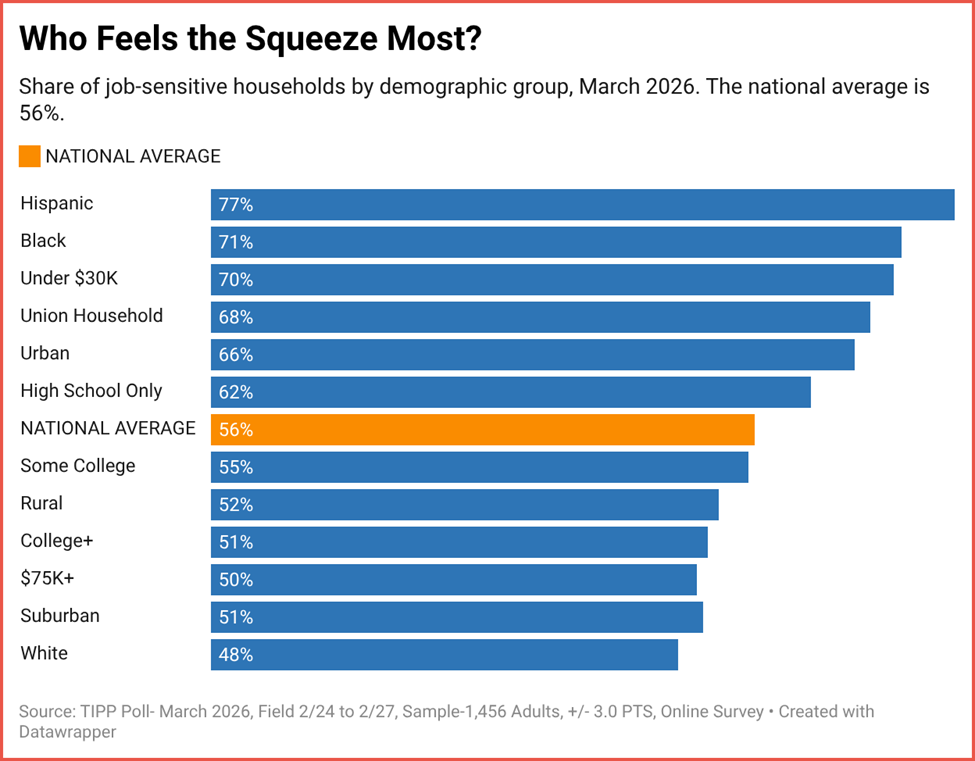

If you mapped job anxiety onto a demographic chart, the contours would look depressingly familiar. Black and Hispanic households haven’t dipped below 65% in any of the fifteen months. In March, the readings are Black (71%) and Hispanic (77%). White households came in at 48%. That’s a persistent 24-point gap that has barely budged.

The income story is similar. Households earning under $30,000 posted 70% job sensitivity in March, the highest reading for that bracket in the data set. The $75K-plus crowd registered at 50%. That’s a 20-point gap, wider than when the analysis period began.

Urban households consistently run about 15 points higher than suburban ones. Union households outpace non-union by 14 points. People without a college degree are 10 points more anxious than graduates. None of this is surprising, but seeing it hold so steady, month after month, drives home how structural these differences are.

The bar chart above is worth sitting with. Look at where the national average falls, and then look at how far above it Hispanic, Black, and low-income households sit. Those aren’t outliers. Combined, they represent tens of millions of families.

Is Anyone Listening?

Politicians love to cite the unemployment rate because it’s clean and it fits on a bumper sticker. But it doesn’t capture what families actually feel. The TIPP Job Sensitivity Index does. And what it says is that, for 15 months, through seasonal swings, news cycles, and policy changes, the majority of American households have been either coping with unemployment in their family or worrying about it.

Families are living this every day. And with midterm campaigns ramping up, it’s the reality that candidates are going to run into at every door they knock on.

The 56% isn’t going anywhere. The country knows it. The question is whether Washington does.

The TIPP Poll surveys approximately 1,400–1,500 U.S. adults monthly via an online panel. The Job Sensitivity Index combines two questions: household members currently seeking work and those concerned about layoffs within 12 months. A household is “job sensitive” if either condition is present. National credibility interval is approximately ±3.0 points; subgroup margins are wider. This editorial analyzes 15 monthly waves from January 2025 through March 2026.

👉 Show & Tell 🔥 The Signals

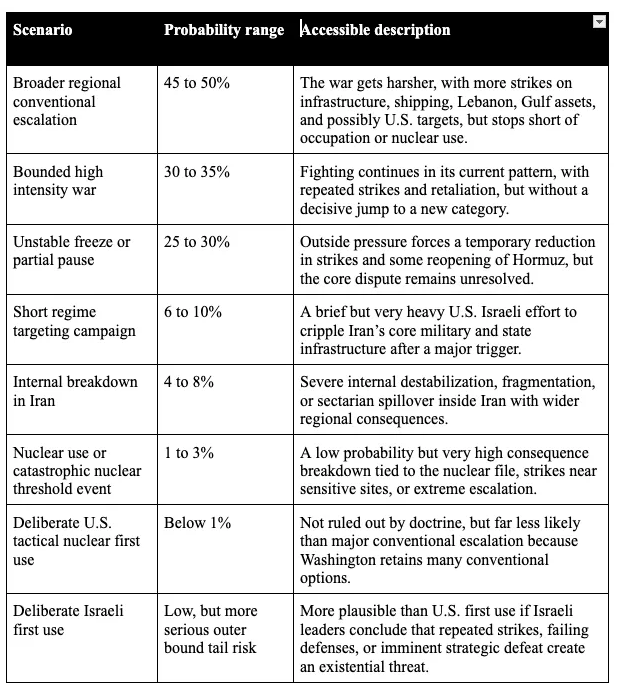

I. War Likely To Broaden, Not Break

The most probable outcome is a wider regional conflict that stops short of regime change or nuclear use. Scenarios cluster around escalation and prolonged fighting, with only a fragile pause as an alternative. Extreme outcomes remain low probability but high impact.

Scenario probabilities as of 23 March 2026

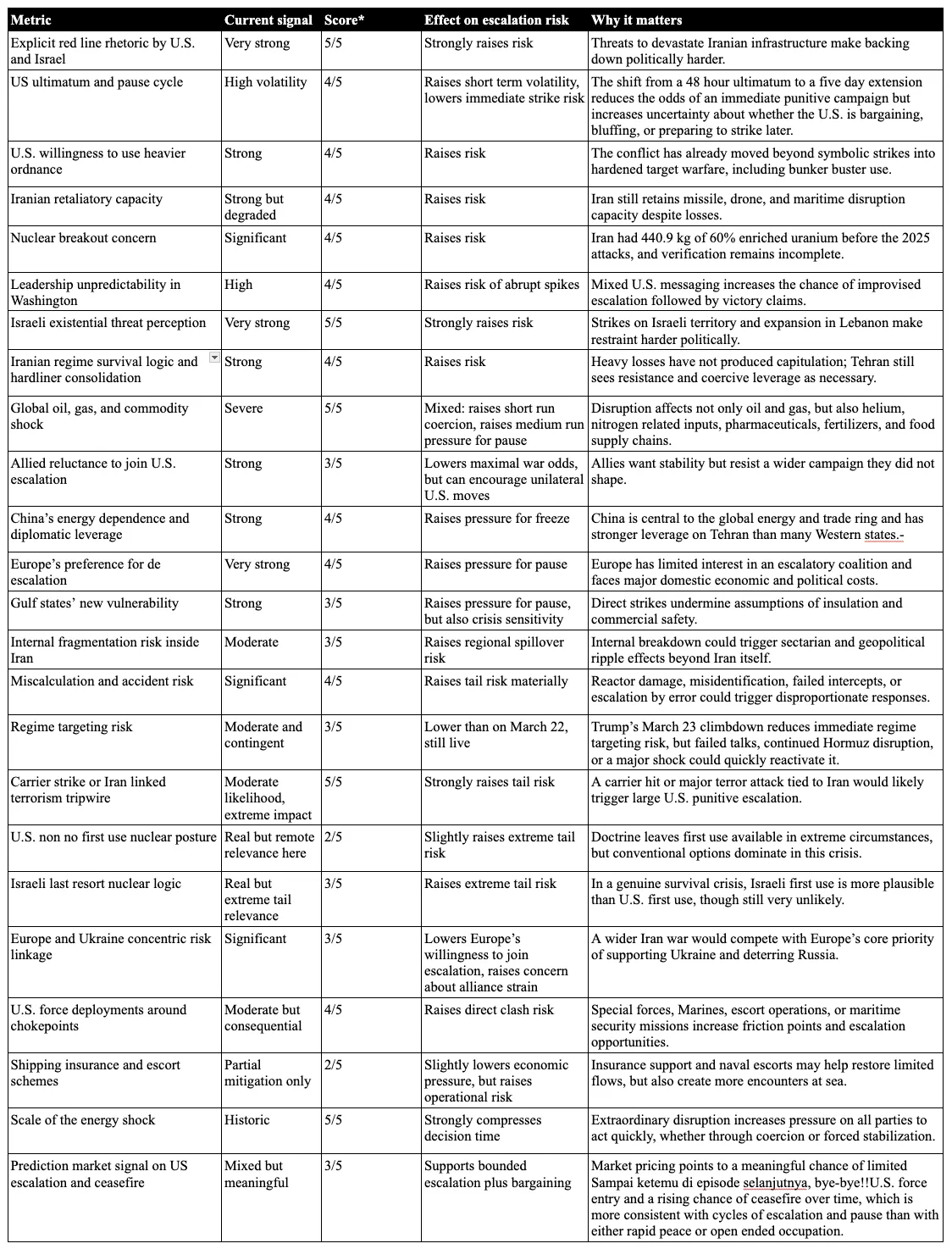

II. Escalation Risks Are Building Across The System

Nearly every major signal points toward rising escalation risk, from hardened rhetoric and heavier strikes to persistent Iranian retaliation capacity. Restraining forces exist, but they are weaker and slower moving. The system remains vulnerable to a sudden shock.

Driver matrix as of 23 March 2026

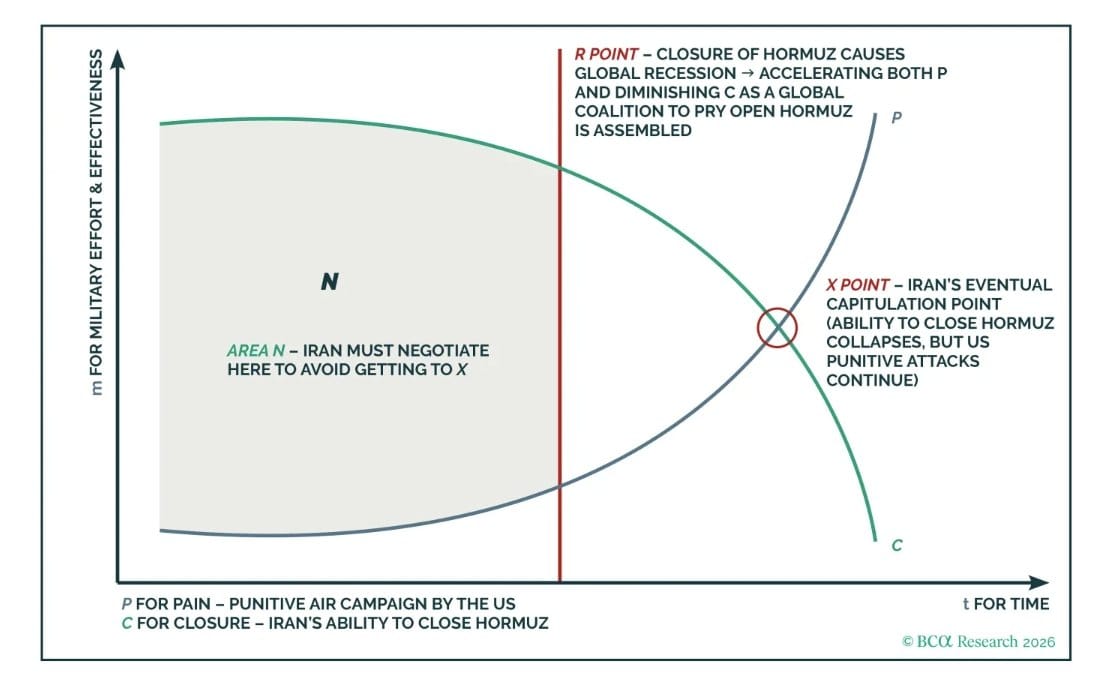

III. Iran Faces Narrow Window To Negotiate

This chart maps a race between pressure and capability. As U.S. military pressure rises, Iran’s ability to sustain resistance falls.

- The green curve shows Iran’s ability to keep fighting

- The blue curve shows U.S. pressure increasing over time

- The intersection (X point) is the tipping point — where Iran can no longer hold out

To avoid that outcome, Iran must negotiate earlier, in the “N zone”, before pressure overwhelms its position. If it waits too long, the choice is no longer negotiation — it becomes capitulation.

The TIPP Stack

Handpicked articles from TIPP Insights & beyond

1. There Is No GOP ‘Civil War’ Over Iran…—James Carden, Mises Wire

2. Treasury’s Bessent Says US Has ‘Plenty’ Of Funds For Iran War—Reuters Staff, The Daily Signal

3. Heartland Polling: Iran War Is Unpopular, But Not Hurting Trump—Steve Cortes, The Daily Signal

4. On The Road To Armageddon—Philip Giraldi, Ron Paul Institute for Peace and Prosperity

5. As The Wheels Come Off The Iran Conflict, It Compels The Decision: ‘Where Do We Stand?’—Alastair Crooke, Ron Paul Institute for Peace and Prosperity

6. Trump Stops Strikes On Iran’s Energy Infrastructure— Virginia Allen, The Daily Signal

7. Join The US Military – Kill And Die For Israel—Brian McGlinchey, Mises Wire

8. America First Trade Must Put American Companies First—Steve Cortes, Daily Caller

9. How The Human Rights Campaign Makes You Complicit In Child Victimization—Katy Faust, The Daily Signal

10. Justices Skeptical Of Counting Late-Arriving Ballots—Fred Lucas, The Daily Signal

11. Artificial Intelligence Is Taking Over Political Campaigns—George Caldwell, The Daily Signal

12. Abortion Is The Worst Way To Celebrate America 250—Joshua Mercer, The Daily Signal

13. In The Pink— David Gordon, Mises Wire

14. How Trump Is Protecting Parents’ Rights To Reject Children’s Transgender Identity—Elizabeth Troutman Mitchell, The Daily Signal

15. The Interesting Lies Of Samuelson: How We Naively Believed The Case Of Giffen Goods— Ali Hashemifara, Mises Wire

16. No, Following The Money Behind Antifa Is Not An Attack On The First Amendment— Tyler O'Neil, The Daily Signal

17. It Still Takes A Village—We Just Forgot How To Build One— Reagan Campbell, The Daily Signal

18. Some States Are Taxing Trump Accounts—What Families Need To Know—Fred Lucas, The Daily Signal

19. Pennsylvania Is Losing Businesses And Workers—Megan Martin, The Daily Signal

📊 Market Mood — Thursday, March 26, 2026

🟩 Markets Slip as Ceasefire Prospects Remain Unclear

European stocks edged lower as conflicting signals clouded hopes for a near-term Iran peace deal.

🟧 Oil Stays Elevated Despite Negotiation Hopes

Crude rose again as the Strait of Hormuz disruption continued to constrain global supply.

🟦 Inflation Risks Keep Central Banks on Alert

Policymakers signaled that energy-driven inflation could delay or even reverse rate cuts.

🟨 Geopolitical Uncertainty Keeps Volatility High

Markets remain highly sensitive to shifting headlines as investors balance peace hopes against escalation risks.

🗓️ Key Economic Events — Thursday, March 26, 2026

🟧 08:30 ET — Initial Jobless Claims

Weekly filings for unemployment benefits provide a timely read on labor market conditions and layoffs.

editor-tippinsights@technometrica.com

{kind=link}