By Vincent Cook, Mises Wire | July 01, 2026

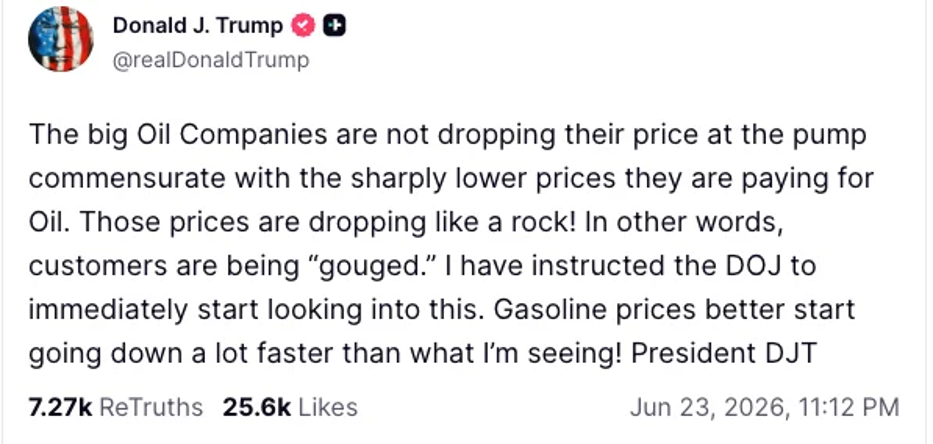

In his 6/23 Truth Social post (figure 1), President Trump noted that the prices paid by major American oil companies for foreign crude are falling much faster than the prices of their retail products, and suggested that there is something criminal about this that the Department of Justice (DOJ) needs to look into:

Figure 1: Trump Denounces Oil Price “Gouging”

Source: Truth Social

The political motivations for Trump’s grandstanding about oil prices are obvious—the financial interests of vast majority of voters are much more strongly affected by the retail costs they pay for oil than by the earnings their stock portfolios receive from ExxonMobil, the Royal Dutch/Shell group, Chevron, Marathon, Valero, and Phillips 66. Since the days of the ancient Roman Republic, politicians have always garnered applause from the economically ignorant by denouncing supposedly wicked price “gougers” who “hoard” goods by refusing to sell them at the allegedly “fair” prices the public is used to. Trump sees an opportunity to gain such applause in this particular situation, and he is of the contemporary bipartisan school of unprincipled policy-making that never lets a crisis go to waste.

Moreover, Trump has been taking a lot of political heat for gasoline prices soaring due to him starting an unconstitutional war of aggression against Iran and then failing to keep the Strait of Hormuz open despite all his vain boasting about having destroyed Iran’s military forces. Everybody knows that Trump is personally responsible for triggering an enormous global oil supply shock and its resulting gasoline price spike, so, of course, Trump wants to shift as much of the blame as he can onto others. “Big Oil” companies have been demonized for well over a hundred years, so of course they make excellent fall-guys to pin the blame on.

More thoughtful economists have long recognized that price “gouging” is not a bad thing, so Trump’s post seems like an excellent opportunity to explain, yet again, why prices behave the way they do during and after supply shocks and why consumers should welcome such moves.

The first thing to keep in mind is that production of any good requires time, often with the good moving through multiple stages of production. In the case of oil, the raw liquid pumped out of the ground might need to be lightly processed (to remove corrosive sulfur contaminants, for example) and then loaded onto a global network of tankers and/or pipelines to deliver it to refineries, where the crude oil is then converted into gasoline and other petroleum products. These refined products then need to be transported to retail outlets, in some cases involving very long distances (as in the case of fuel for the California market, whose state government has foolishly compelled the closure of most of its local refining capacity, thus necessitating expensive imports of refined fuel from far-away places like the Bahamas, India, and South Korea).

The second thing to keep in mind is that at many of these stages of production, it is possible to store the resulting outputs of the stage. Thus, as oil moves through the supply chain, any unusual fluctuations in the supply of inputs and/or the demand for outputs at a given stage can be buffered by increasing or decreasing that stage’s inventories. The effect of increasing the reserves stored at a given stage is to temporarily decrease the quantity of that stage’s outputs, thus temporarily driving output prices up relative to input prices. Likewise, drawing down reserves will increase that stage’s output quantities and thus drive prices down.

Keeping some of one’s product in reserve has a cost associated with it. Given a choice between selling a good now versus selling it in the future, storing the good for a future sale makes economic sense only if the price one expects to get in the future exceeds the present price by a large enough margin to cover the additional costs of storage, interest, insurance, etc. over the holding period. This incentivizes one to add to one’s inventory when demand becomes relatively slack or supplies become relatively abundant, and draw down one’s inventory when demand becomes relatively tight or supplies become relatively scarce.

This means that when a supply shock curtails outputs of an earlier stage of production, everybody anticipates that fewer goods will be moving through the supply chain to the consumer and output prices of all the later stages will be higher. Goods that were previously stored in inventories at the later stages of production are now mobilized to take advantage of the higher prices. However, the very fact that reserves are being drawn down at later stages means that prices won’t soar quite as much as they would have without the draw-down of reserves. Consumers clearly benefit from the dishoarding that occurs while the shock is in progress, since it mitigates the price increases and meets their more urgent needs.

So what happens when the shock at the earlier stage is finally mitigated, and its outputs reappear in the marketplace? The price of outputs at the earlier stage will “fall like a rock” (to use Trump’s phrase), but the inventories at all the later stages have been somewhat depleted over the course of the shock. Producers at later stages of production will have to take advantage of these lower prices to rebuild their inventories, temporarily reducing the supply available to consumers and slowing down the rate at which the prices paid by consumers fall. This delayed fall of retail prices reflects in part the additional costs of refilling reserves along the supply chain to enable it to respond to future supply shocks and demand spikes.

This delayed fall of prices at the retail stage also reflects the fact that there is still a time lag between larger quantities of the outputs of earlier stages becoming available versus larger quantities of retail products becoming available. The resumption of crude oil shipments coming out of Hormuz does not instantaneously make more gasoline or diesel appear at your local gas station. Ships still have to cross oceans, refineries still have to process crude inputs, etc. before additional supplies become available to consumers at the final retail stage. Your local retail outlet still has to set prices that balance consumer demand against whatever supplies it has available, which must remain constricted for some time.

Using the DOJ to compel reductions in retail prices would inhibit the recovery of inventories to meet future supply shocks and perhaps cause short-term shortages that would require some form of rationing of the supplies available to consumers. Federally-imposed price controls, rationing schemes, and heavy-handed regulation of domestic oil companies were a thing back in the 1970s; few of us old enough to remember the consequences of such policies would want to relive the experience.

The bottom line is that the market price system ultimately allocates scarce resources in line with the preferences of consumers. We may not like to confront unpleasant trade-offs between present and future needs that suddenly arise as a consequence of political blundering, but using further threats of force to intimidate or regulate producers only makes things more unpleasant for consumers. If anybody needs to be held accountable for increasing gasoline prices, it is the politicians who interfere with production, restrict commerce, and use military force to wreck global supply chains.

Vincent has a MA in Biophysics from the University of California, Berkeley. He worked as an analyst for thirty years in the University of California’s Office of the President, reporting statistics concerning technology transfers, research grants and expenditures, and faculty salaries on behalf of the ten campus UC system.

Original article link

{kind=link}