By Patrick Barron, The Mises Institute | August 26, 2023

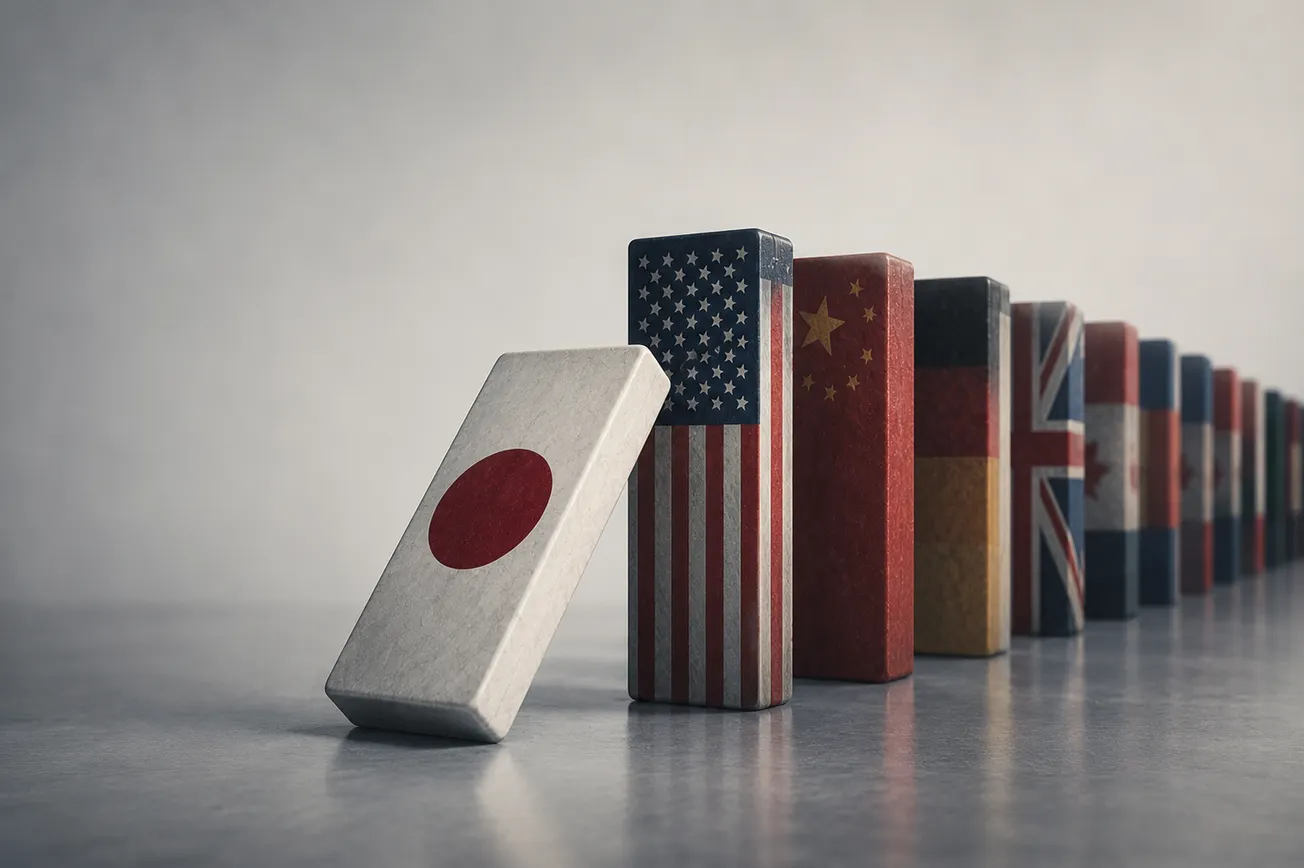

Leaders of the Western democracies are unprepared to deal with the forces that will end the fiat dollar’s dominance as the preferred medium of international trade settlement, in place since the end of the Bretton Woods Agreement in 1971.

The BRICS summit, currently taking place in Johannesburg, South Africa, is expected to include an agreement on a first step toward establishing an alternative international trade settlement system based on commodities, which would certainly include gold. Dozens of non-Western and even some Western-affiliated nations are attending and watching with great interest. Six new members have been invited to join Brazil, Russia, India, China, and South Africa—Argentina, Egypt, Ethiopia, Iran, Saudi Arabia, and the United Arab Emirates.

Although the coming change may be characterized as one between the Western democracies and the BRICS nations, the real battle is one of ideas—between Keynesian economic theory and gold. The winner will be gold.

As Murray N. Rothbard explained in What Has Government Done to Our Money?, gold was never proven to be inferior to fiat money. The gold standard was not replaced by a better monetary system. It was suppressed in stages to satisfy the state’s insatiable need for money—first to make war and then to corrupt the people via welfare. The result, of course, has been never-ending wars, a creeping expansion of the welfare state, unsustainable public deficits, and the accelerating debasement of the currency.

The challenge to the fiat dollar began with its debasement, which has lowered its purchasing power to gold by 98 percent since 1971, and this challenge accelerated with the introduction of the so-called Russian sanctions—freezing Russian-owned assets in the West and denying Russia access to the international dollar trade settlement messaging system known as SWIFT. Russian monetary expert Sergey Glazyev has led the movement toward an alternative system.

Putting “Paid” to Keynesian Fallacies

Introducing gold into the trading system will expose the main fallacy of Keynesian economics: the elevation of aggregate demand to prominence in a nation’s economy rather than production—the only means of satisfying the demand in the first place. Jean-Baptiste Say showed that production is required in order to enjoy the benefits of consumption. Instead, Keynes shunned Say’s law in his General Theory of Employment, Interest and Money in order to hide his theory’s internal contradictions. Keynes elevated the concept of “aggregate demand” over production, while Jean-Baptiste Say shows that production is required in order to enjoy the benefits of consumption.

On the face of it, it is hard to believe that anyone would believe that production either isn’t required for consumption or that it magically appears. Yet, this rather upside-down theory appealed to politicians for obvious reasons—it gave them carte blanche to spend, all with money created out of thin air by the central bank. Rather than economize and prioritize spending that was absolutely necessary for the benefit of the entire nation, politicians were told by Keynes that it was their duty to spend, even if it was only to pay people to dig holes and others to fill those holes back up.

Basics of a Gold Settlement System

The new international trade settlement system will require settlement in gold. A possible mechanism has been outlined by Alasdair Macleod of Goldmoney. The benefits of the new system will become obvious to every nation, not just the current BRICS members. The political benefit is that no one nation can control or manipulate the system for its unearned benefit. The economic benefit is that government spending will be minimized so that resources can be allocated to production rather than state aggrandizement. A member can expand imports only by expanding exports. This puts market pressure on member governments to reform their internal economies in order to increase production.

Artificially increasing demand, per Keynesian orthodoxy, would be counterproductive because gold would drain from the nation’s gold settlement account, and imports would be suspended. Therefore, the system encourages sound economic practices within its members’ individual economies. Printing money, excessive and unnecessary regulations, excessive taxation, and excessive government spending do nothing to aid a member’s ability to engage in trade. Nations like the United States, who have huge welfare obligations and who have politically connected industries that do not add to the nation’s capital base, will struggle. Having lots of nuclear weapons will be irrelevant, and having bases around the world will be liabilities rather than assets.

An important point made by Macleod is that, over time, the gold settlement system for international trade will expand into the members’ internal monetary systems. In other words, fiat currencies—which can be inflated or debased by governments—will be thrown on the ash heap of history. Instead of Keynes’s predictions in 1924 of the gold standard, the fiat currencies will instead become the “barbarous relics” themselves.

Patrick Barron is a private consultant to the banking industry. He has taught an introductory course in Austrian economics for several years at the University of Iowa. He has also taught at the Graduate School of Banking at the University of Wisconsin for over twenty-five years, and has delivered many presentations at the European Parliament.

Original article link