The American economy is growing. Corporate earnings are solid. The stock market, despite its wobbles, remains near historic highs. If you have money in the market, the world looks pretty good.

But the latest RealClearMarkets/TIPP data reveals something beneath that rosy picture. The economy is not failing. It is splitting. And the split is widening the gap between the rich and the nowhere-near-rich.

The March RCM/TIPP Economic Optimism Index, the first major monthly consumer confidence reading, came in at 47.5. That headline number, modest and unremarkable, masks one of the sharpest confidence divides we have recorded in 25 years of tracking American sentiment.

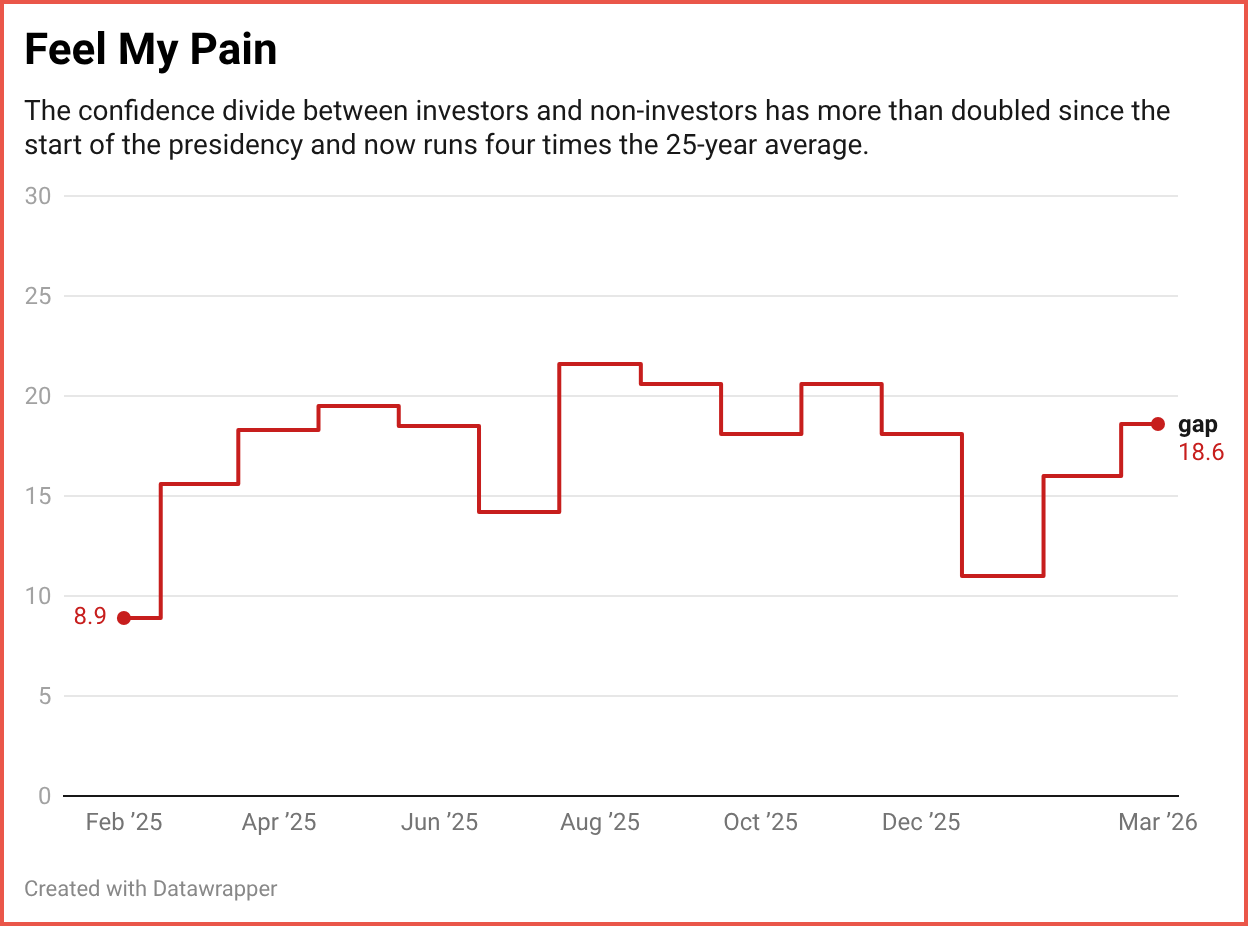

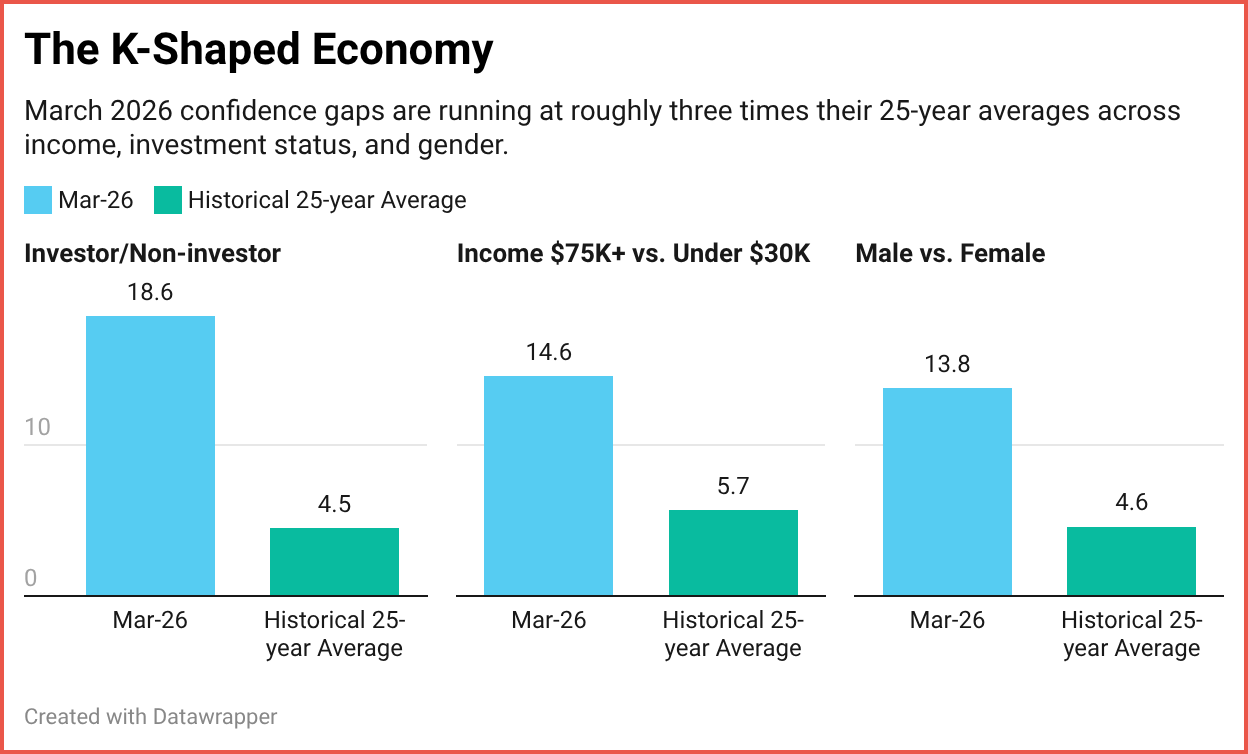

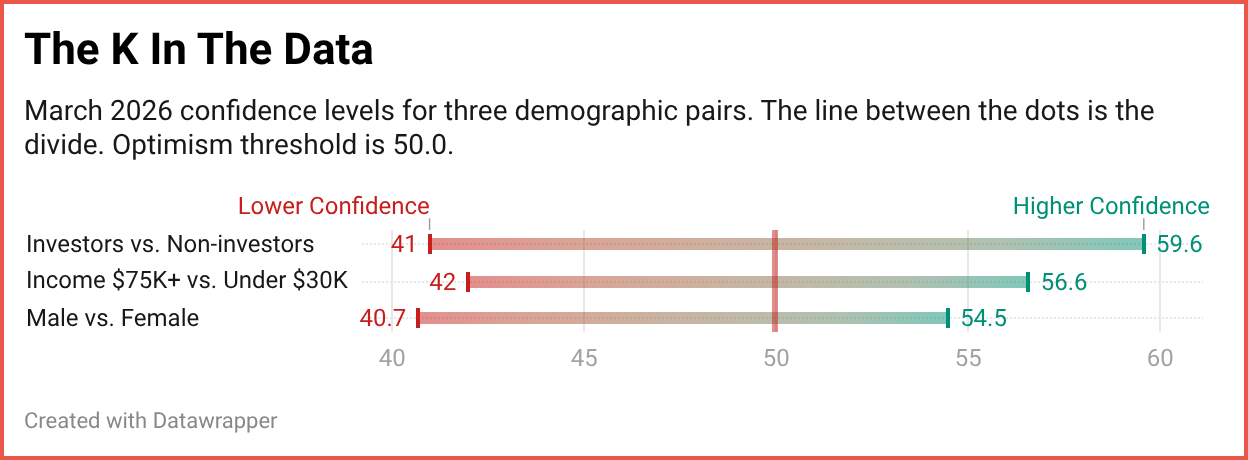

Start with investors versus non-investors. Respondents with at least $10,000 in the stock market registered 59.6 on the optimism index, comfortably above the neutral 50 line. Non-investors came in at 41.0. That 18.6-point gap is larger than the gap recorded in all but eight months of the Index's 302-month (25+ years) history. The historical average is 4.5 points.

The income picture tells the same story. Americans earning $75,000 or more posted a confidence reading of 56.6, solidly optimistic. Those earning under $30,000 came in at 42.0. The 14.6-point divergence between them is nearly three times the long-term average of 5.7.

And it is not just about money in the bank. There are other shades to the story.

The gender gap in March reached 13.8 points, with men at 54.5 and women at 40.7. The 25-year average is 4.6 points. March's reading is three times the norm and within striking distance of the all-time record of 18.2, which was set in March 2023. Men are solidly optimistic. Women are deep in pessimism territory.

The financial stress data confirms the pattern from the other side of the ledger. Black and Hispanic financial stress surged over 6 points in a single month, reaching 67.5. Young adults aged 18 to 24 jumped nearly 6 points to 67.9, the highest stress reading of any age group. The pressure rose by more than 3 points to 66.4 among the $30,000 to $50,000 income bracket.

Meanwhile, seniors saw their stress drop 1.7 points to 56.1, the lowest among age groups. White respondents dropped 1.3 points.

Economists call this a K-shaped economy. The letter itself tells the story. Picture the vertical line of the K as the economy standing upright. GDP is growing, jobs are being created, and the system is functioning. Now look at the two arms branching off from the middle. The upper arm angles upward. That is the investors, the higher earners, those with assets and market exposure. Their confidence is holding or rising. The lower arm angles downward. That is the segment earning less, the non-investors, those without a financial cushion. Their confidence is falling. The economy is growing, but they are not benefiting from it.

The two arms are moving apart. That is the critical point. It is not that all of America is going up or all of America is going down. Different groups of Americans are heading in opposite directions at the same time, and the March data shows this across income, gender, and investment status.

However, there is some encouraging news.

A K-shaped divide is not a recession. It is not even a downturn. It is a sign that the benefits of a growing economy have not yet reached everyone. That word, "yet," matters.

The economy is still expanding. Inflation is moderating, which tangibly helps lower-income households as they spend a larger share of their income on essentials. The labor market remains stable, with unemployment low across demographics.

The Personal Financial Outlook component of the Index stands at 54.3. That is above the optimism line. Americans, on the whole, still believe their household finances will improve over the next six months. That is a meaningful reservoir of confidence.

History tells us that the K does not have to stay open. When growth broadens, the two arms start to converge. The K begins to close. We saw this in the mid-2010s recovery and in the post-pandemic rebound, when wages at the bottom grew faster than wages at the top, and gaps that seemed entrenched began to narrow.

The question for policymakers is straightforward. The top of the K does not need help. The bottom does. Policies that reduce uncertainty, support wage growth, and expand market participation will do more to lift the overall index than anything else.

When the arms of the K fold back in, you are left with just the vertical line. Everyone is moving in the same direction. That is a broad-based recovery, the kind that sustains durable growth and lifts the national mood.

We are not there yet. But the path is visible. The K has become pronounced in March. It does not have to become permanent. That is the signal in the data, and it deserves attention.

👉 Show & Tell 🔥 The Signals

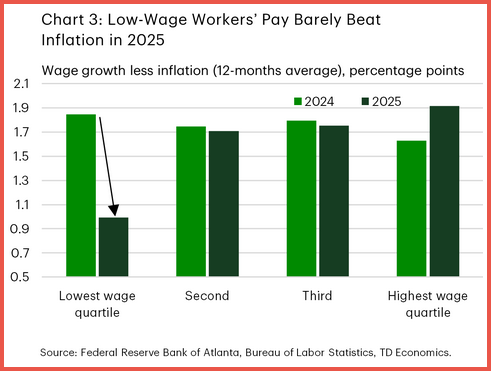

I. Low-Wage Workers’ Pay Barely Beat Inflation

Wage growth is losing momentum for lower-income workers. In 2025, real wage gains for the lowest-paid workers fell to about 1 percentage point, down sharply from roughly 1.8 points in 2024. Higher-income workers saw steadier gains, highlighting the uneven pace of income growth.

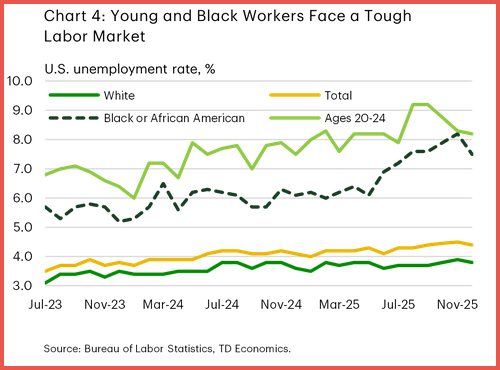

II. Young And Black Workers Face A Tougher Labor Market

Unemployment has risen more sharply for vulnerable groups. Black unemployment climbed toward 8% in late 2025, while the rate for workers ages 20–24 approached 9%. By contrast, unemployment among white workers remained below 4%, underscoring widening disparities in the labor market.

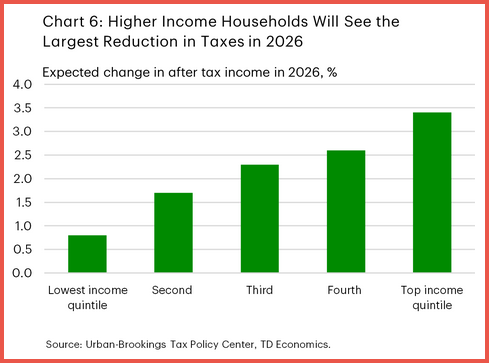

III. Higher-Income Households Gain Most From 2026 Tax Changes

Projected tax changes for 2026 are expected to deliver the largest boost to top earners. After-tax income for the highest-income households could rise by roughly 3–3.5%, compared with less than 1% for the lowest-income group, suggesting a widening gap in disposable income.

The TIPP Stack

Handpicked articles from TIPP Insights & beyond

1. Trump Says U.S. Must Help Choose Iran’s Next Leader—News Editor, TIPP Insights

2. US Military Leaders Tell Troops Trump Is Waging Iran War To Bring Forth Second Coming Of Jesus—blueapples, Ron Paul Institute for Peace and Prosperity

3. Bahrain’s Big Breakout—Gerry Nolan, Ron Paul Institute for Peace and Prosperity

4. Why US Firms Aren’t Racing Into Venezuela, Even With Political Incentives—Nicoleta Tanase, Mises Wire

5. Immigration Enforcement Saves Lives—Daniel McCarthy, The Daily Signal

6. Biden Judge Blocks ICE Detention Policy For Congress—Fred Lucas, The Daily Signal

📊 Market Mood — Friday, March 6, 2026

🟩 AI Data Center Boom Lifts Chip Stocks

Marvell surged in after-hours trading after raising its revenue outlook on strong AI-driven data center spending.

🟧 Oil Heads for Weekly Surge on Iran Conflict

Crude prices are set for big weekly gains as fighting in the Middle East threatens supply through the Strait of Hormuz.

🟦 Markets Cautious as Geopolitical Risk Persists

U.S. stock futures wavered while investors monitored the escalating Iran conflict and rising bond yields.

🟨 Investors Await February Jobs Report

Markets are watching the upcoming U.S. payrolls data for clues about labor market strength and the path of Federal Reserve policy.

🗓️ Key Economic Events — Friday, March 6, 2026

🟧 08:30 ET — U.S. Jobs Report (Feb)

Nonfarm payrolls, unemployment rate, and wage growth provide the clearest snapshot of labor market strength and wage pressures.

🟧 08:30 ET — Retail Sales (Jan)

Retail and core retail sales measure consumer spending momentum, a key driver of overall economic growth.

editor-tippinsights@technometrica.com

{kind=link}