The American economy has a habit of confounding the pessimists. Growth remains resilient, the labor market holds, and moderating inflation is gradually restoring purchasing power.

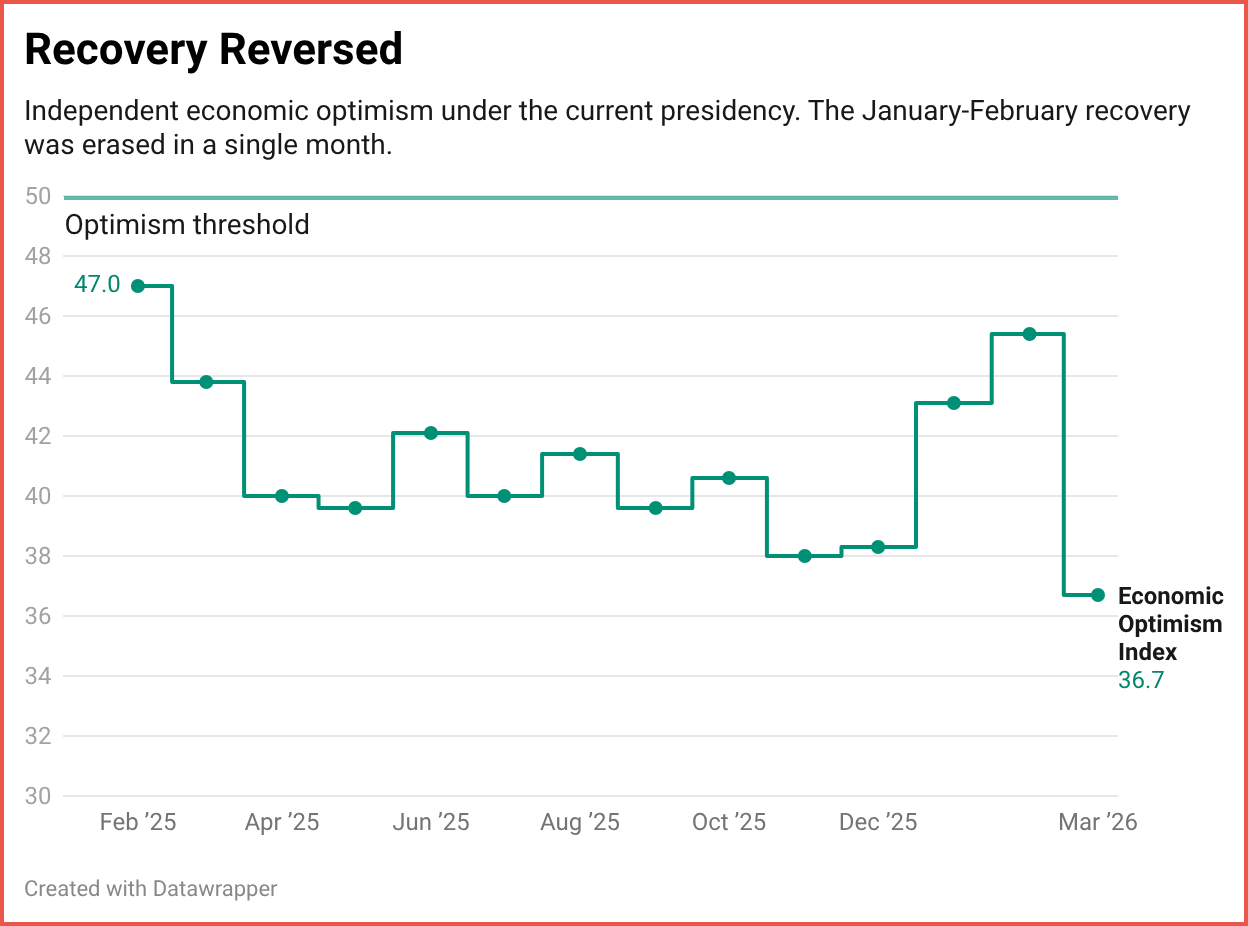

The latest RealClearMarkets/TIPP Economic Optimism Index, the first consumer confidence reading each month and a proven bellwether for the University of Michigan and Conference Board numbers that follow, shows the headline at 47.5, down modestly from 48.8 in February.

This modest decline is not a collapse, nor a crisis. But buried within that modest decline is one data point that deserves serious attention.

Independent voters just posted an 8.7-point plunge in economic optimism, falling from 45.4 to 36.7.

That is the fourth-largest single-month drop for this group in the 25-year history of the Index, rivaled only by the onset of COVID-19, the pandemic-induced lockdowns in the spring of 2020, and the aftermath of Hurricane Katrina in September 2005. It is also the lowest reading posted by independents for the current presidency.

Gold standard in polling — the only national pollster to get six presidential elections right. Talent on loan from God. Subscribe now → $99/year

Why does this matter more than the headline number?

Independents are the market signal in the political economy. Democrats and Republicans mostly move in predictable, partisan ways. When their party holds the White House, confidence rises. When it does not, confidence falls.

Independents have no such anchor. They react to current events, making them the closest thing we have to a real-time, unfiltered gauge of economic sentiment.

And what they saw in late February, when the latest RealClearMarkets/TIPP survey was conducted, was a Supreme Court ruling on tariffs that left trade policy uncertain and a massive U.S. military buildup pointing toward Iran.

Both events introduced the one thing pragmatic, non-ideological voters dislike most: ambiguity. Not necessarily bad outcomes, but unclear ones.

The timing makes the drop on the Index even more telling. Independents had been recovering. From a low of 38.0 in November, they climbed to 38.3 in December, 43.1 in January, and 45.4 in February- a steady, encouraging trajectory.

March did not merely pause that recovery. It erased it entirely and set a new floor.

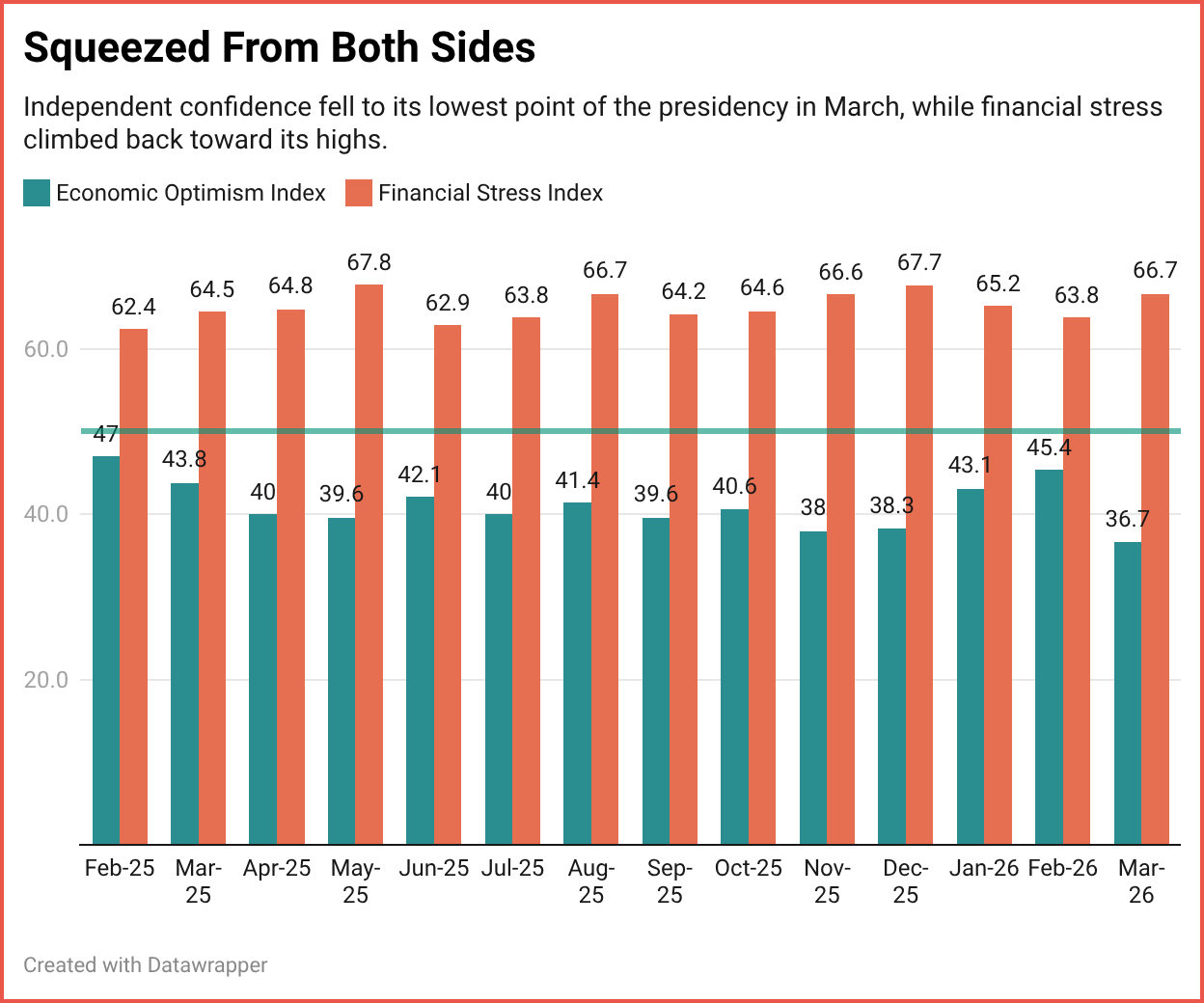

The financial stress data tells the same story from the other side of the ledger. Independent financial stress surged 2.9 points to 66.7 in March, pulling level with Democrats as the most financially stressed partisan group.

Here is what makes that significant. Democrats have structural reasons for elevated stress under a Republican administration. Independents have no such reason. When they report this level of strain, it reflects genuine economic anxiety, not political disposition.

Now, the optimist's case, and we make it advisedly.

The fundamentals have not deteriorated. The economy is still growing. Employment is stable. The Personal Financial Outlook component of the Index stands at 54.3, comfortably above the neutral 50 line.

Americans feel less confident about where things are headed. But they have not yet concluded that their own household finances are in trouble. That distinction matters enormously.

The nature of the drop also argues for a snapback.

Historically, event-driven declines in independent confidence have reversed once the triggering uncertainty resolves.

The COVID shock was an exception because it became a sustained economic reality. Hurricane Katrina was localized. The current triggers, tariff policy, and geopolitical brinksmanship are, by their nature, resolvable.

If the trade picture clears and the Iran situation stabilizes, history suggests independents will recover quickly, as the same volatility that caused the drop can drive the rebound.

Context matters, too. Republican confidence remains robust at 67.6. The investor class, those with at least $10,000 in the market, sits at 59.6, firmly in optimistic territory. And the partisan gap has narrowed from 34.4 points in February to 32.6 in March.

The question now is whether April confirms March or contradicts it. A single month, however dramatic, is a data point. Two consecutive months at this level would constitute a trend, and a worrying one, particularly with midterm positioning beginning to take shape.

Independents are not merely an economic indicator; they are the voters who decide elections.

The RCM/TIPP Index has tracked American consumer confidence through five presidencies, two recessions, a pandemic, and countless geopolitical crises. If there is one pattern that recurs, it is this: Americans are more resilient than any single month's data suggests.

The foundation has not cracked. But a tremor has been recorded. It is prudent to pay attention.

👉 Show & Tell 🔥 The Signals

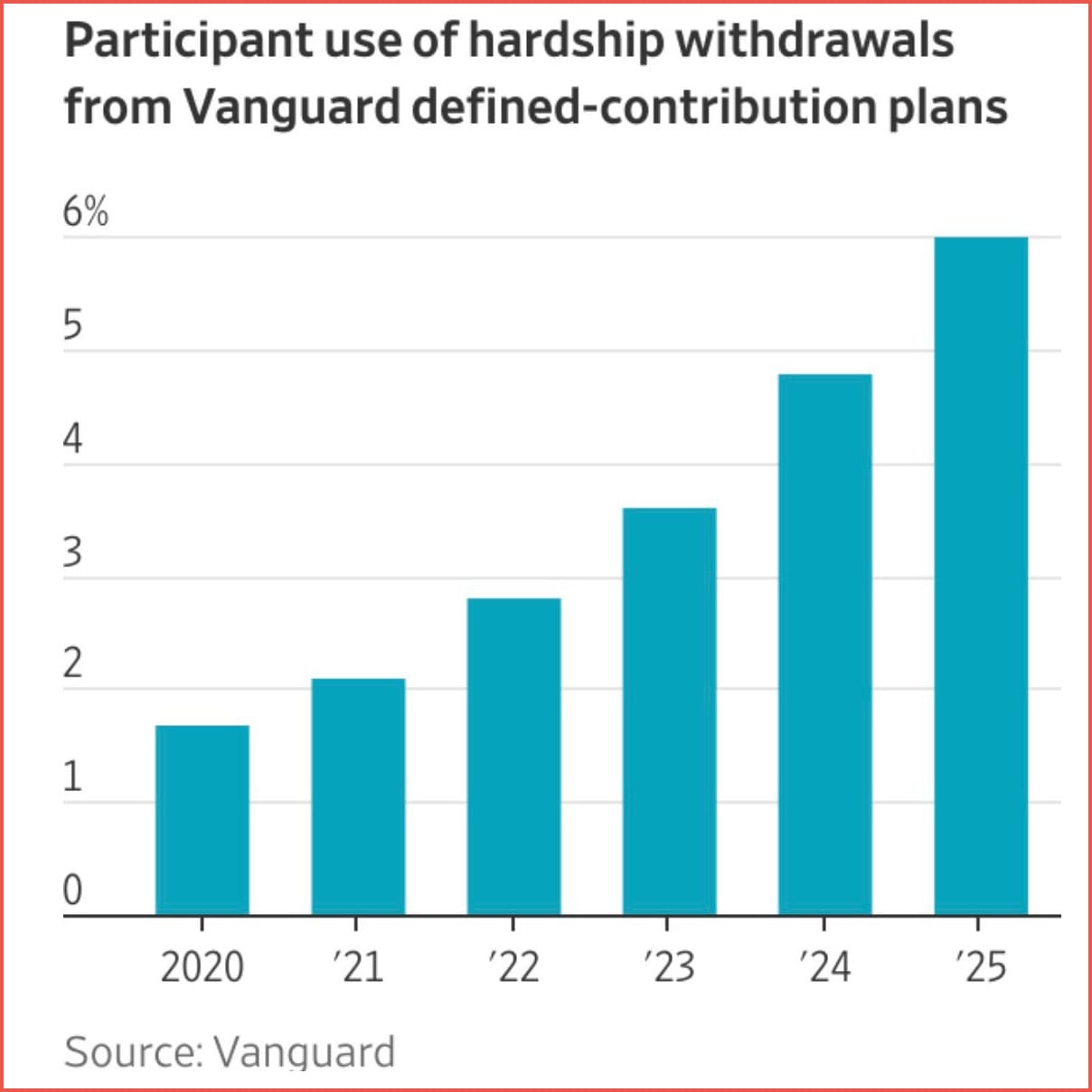

I. 401(k) Hardship Withdrawals Hit Record 6%

A record 6% of workers with Vanguard 401(k) plans took hardship withdrawals in 2025, triple the prepandemic norm. The steady climb from 2020 highlights a widening divide in household finances, where strong labor markets coexist with pockets of rising financial stress.

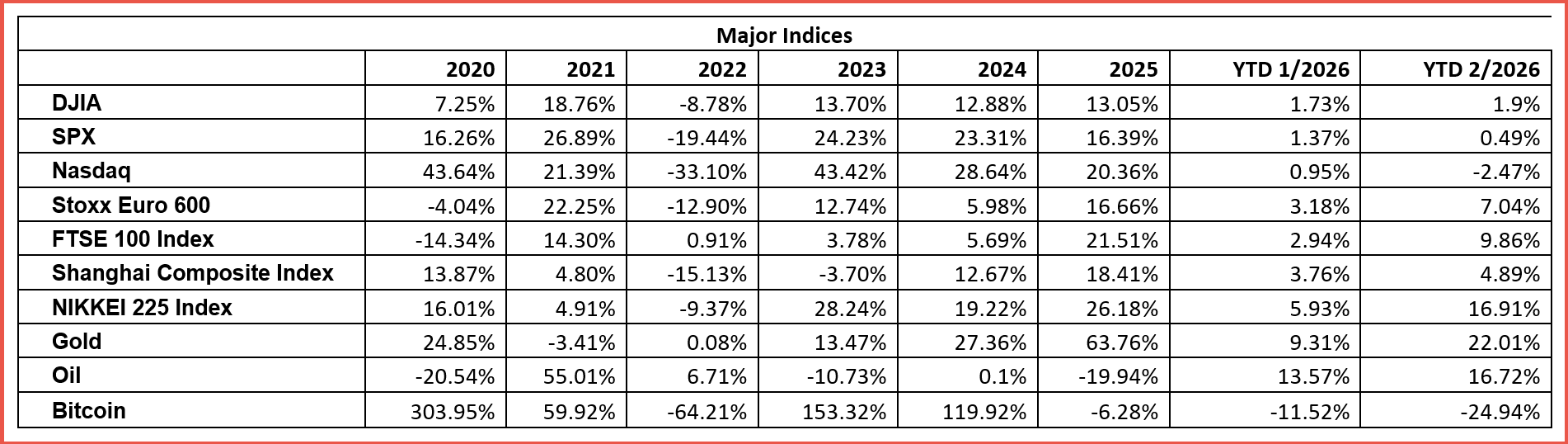

II. Global Markets Show Sharp Divergence

February markets illustrated widening dispersion across asset classes. While the S&P 500 and Nasdaq slipped, gains in Europe, Japan, and China helped offset losses globally. Gold surged while Bitcoin moved sharply in the opposite direction, underscoring increasingly fragmented market trends.

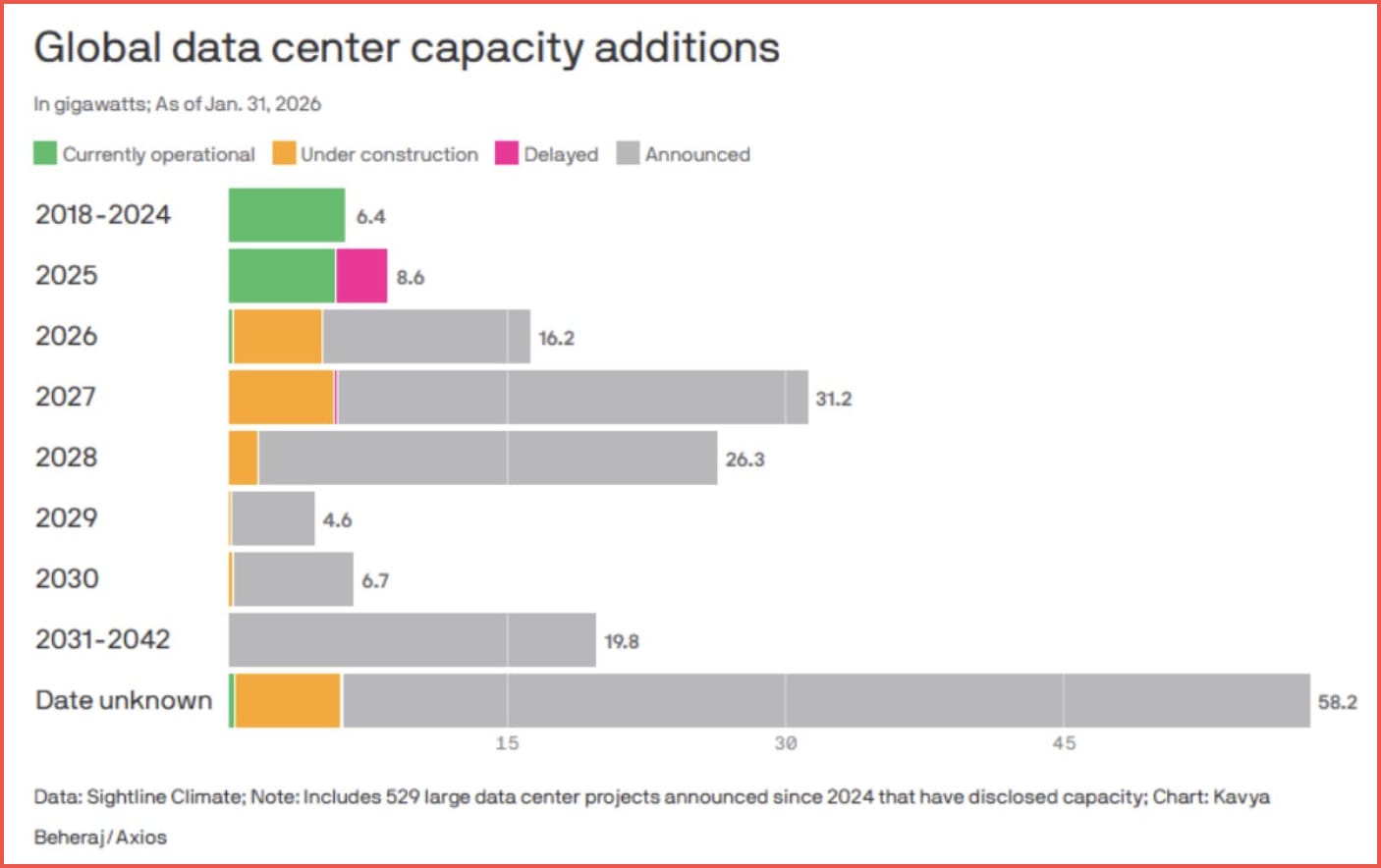

III. AI Boom Is Driving Massive Data-Center Expansion

Global data-center capacity is set to surge as the AI boom accelerates. Projects expected to come online by 2027 alone could exceed 30 gigawatts, reflecting enormous demand for computing power and the energy needed to support next-generation AI infrastructure.

The TIPP Stack

Handpicked articles from TIPP Insights & beyond

Victor Davis Hanson: Another Iran Quagmire Might Mean Big Losses For Republicans In The Midterms—Victor Davis Hanson, The Daily Signal

Epic Fury Abroad, Cyber Blowback At Home: Don’t Let Iran Retaliate Through Our Networks—Bridget E. Bean, The Daily Signal

Trump Administration Officials Reveal Why US Lost Faith In Diplomacy With Iran—Elizabeth Troutman Mitchell, The Daily Signal

Trump Orders Oil Tanker Insurance Support, Says Navy Could Escort Ships In Gulf—Jarrett Renshaw & Timothy Gardner, The Daily Signal

Trump’s War with Iran Is Even More Of A Disaster Than People Realize—Connor O'Keeffe, Mises Wire

The Iran War Exposes The Farce Of American “Representative Democracy”—Ryan McMaken, Mises Wire

GOP Senator Slams Noem For ‘Failure Of Leadership’—Virginia Allen, The Daily Signal

Epstein Probe Widens As Top Trump Official Agrees To Face House Panel—Fred Lucas, The Daily Signal

Blackburn Takes Aim At Big Tech For Harming Teens’ Mental Health—Reagan Campbell, The Daily Signal

All-Hands-On-Deck Energy Policy—Jack Spencer & Joseph Baranoski, The Daily Signal

Lincoln’s Second Inaugural Address Has A Sobering Message For America Today—Tyler O'Neil, The Daily Signal

Ohio’s Abortion Amendment Used To Block Fetal Remains Law—Rebecca Downs, The Daily Signal

A Tax Proposal Against Progress And Democracy—Jesús Huerta de Soto, Mises Wire

Who’s The Biggest Monopolist Of All? (Hint: It’s Not A Corporation)—Clyde Wayne Crews, Jr., Issues & Insights

📊 Market Mood — Thursday, March 5, 2026

🟩 AI Chip Rally Lifts Tech Sentiment

Broadcom jumped in after-hours trading after beating earnings expectations and issuing strong AI-driven revenue guidance.

🟧 Oil Extends Rally as Iran Conflict Threatens Supply

Crude prices climbed for a fifth straight session as attacks near the Strait of Hormuz raised fears of disruptions to global oil flows.

🟦 Stocks Pause as Middle East Tensions Persist

U.S. stock futures slipped as investors monitored the sixth day of fighting involving Iran, Israel, and U.S. forces.

🟨 China Signals Slower Growth Path for 2026

Beijing set a 4.5%–5% GDP target, its weakest in decades, reflecting a more cautious outlook for the world’s second-largest economy.

🗓️ Key Economic Events — Thursday, March 5, 2026

🟧 08:30 ET — Initial Jobless Claims

Weekly filings for unemployment benefits, a closely watched indicator of labor market strength and layoffs.

editor-tippinsights@technometrica.com

{kind=link}