A month ago, the RCM/TIPP Economic Optimism Index registered one of the most sweeping downturns in its history. Twenty of the 21 demographic groups we track moved lower in April; only independents bucked the trend, and only by 0.2 points. We called it a nation united in anxiety.

May reads like a mirror image, and not entirely a reassuring one.

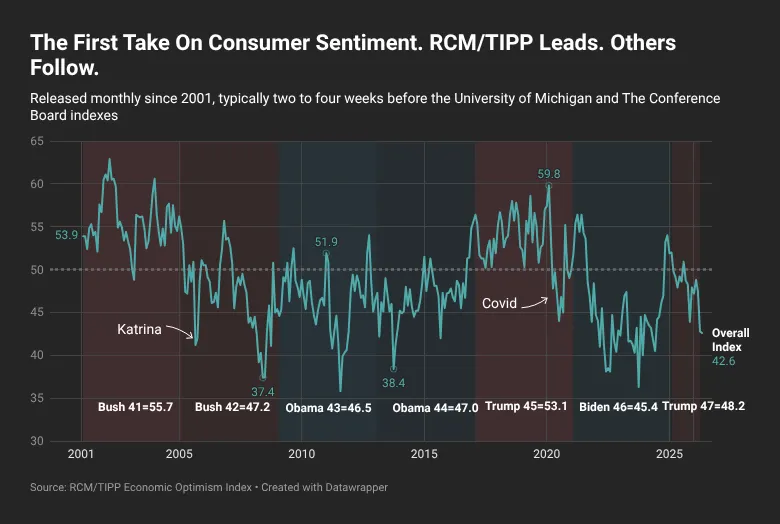

The RealClearMarkets/TIPP Economic Optimism Index, the first monthly read on U.S. consumer confidence, edged down to 42.6 from 42.8 in April, a decline of just 0.2 points. After last month’s 4.7-point plunge, May’s near-flat reading suggests the Index has settled into a holding pattern rather than continuing to fall. The pessimism streak now runs to nine consecutive months.

But the steadiness of the headline number conceals a more interesting story. The companion RCM/TIPP Financial-Related Stress Index dropped 3.6 points to 62.1, its sharpest monthly decline since December 2024. Twenty of the 21 demographic groups we track reported lower stress, the exact inverse of April’s 20-of-21 decline in optimism.

The immediate anxiety that surged with last month’s heightened geopolitical tensions has clearly receded. What hasn’t recovered is the forward-looking judgment about where the economy is headed and the trust in those steering it.

All Three Components, Three Different Stories

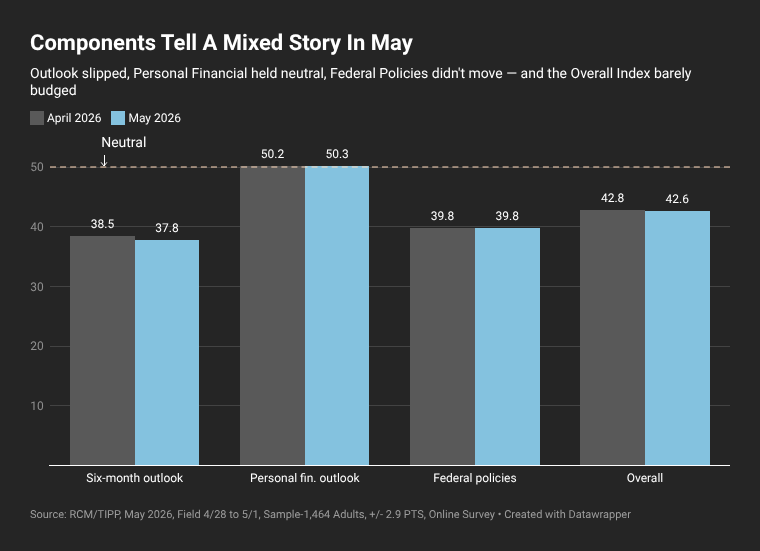

The Index has three key components. In April, all three fell. In May, they parted ways.

The Six-Month Economic Outlook, which measures consumers’ perception of the economy’s prospects over the next six months, fell to 37.8 from 38.5, its lowest reading since June 2024. This is the component most sensitive to forward-looking anxiety, and its continued slide is the clearest sign that Americans’ unease about what comes next has not lifted. April was a shock. May is the absence of resolution.

The Personal Financial Outlook, a measure of how Americans feel about their own finances over the next six months, held nearly flat at 50.3, up a marginal 0.1 from 50.2 in April. For nine months running, personal finances have been the one exception to the slide, holding above the neutral line even as the other two components have weakened. The margin is thin and getting thinner.

Confidence in Federal Economic Policies, a proprietary RCM/TIPP measure of views on the effectiveness of government economic policies, was unchanged at 39.8, identical to April’s reading. Between the April and May surveys, a Middle East ceasefire took hold and the Federal Reserve held its policy meeting. Neither development translated into renewed faith in the policy direction. Federal Policies confidence is now down 5.3 points over two months, and the May plateau looks less like stabilization and more like settled disapproval.

May’s reading of 42.6 sits 13.2% below the 304-month historical average of 49.1, and lands in the bottom 11% of all readings since the index began in February 2001.

Momentum: No Recovery In The Averages

A single month rarely tells you where the country is heading. However, the moving averages do.

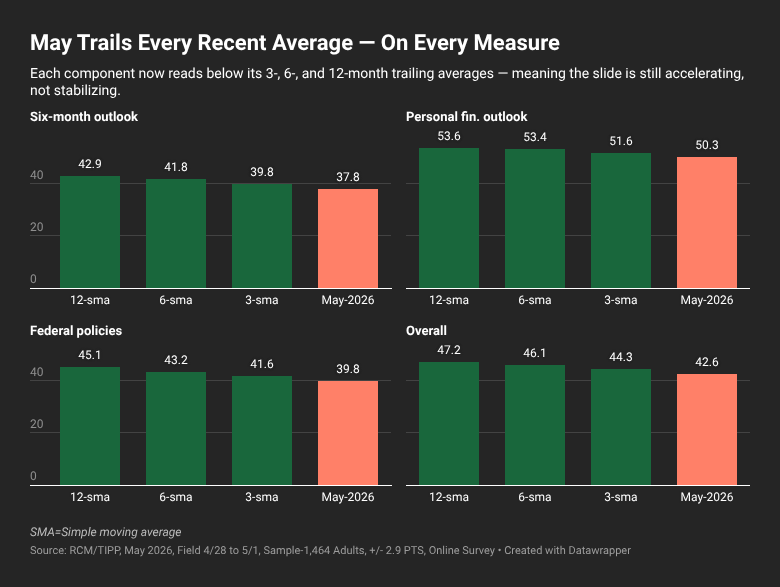

The Optimism Index at 42.6 sits below its three-month average (44.3), six-month average (46.1), and twelve-month average (47.2). All three benchmarks are still trending down. There is no sign in the numbers that May represents a change of course.

The Six-Month Outlook at 37.8 is below its three-month (39.8), six-month (41.8), and twelve-month (42.9) averages, and the gap is widening. The forward-looking component is decelerating, not stabilizing.

Personal Financial Outlook at 50.3 is below its three-month (51.6), six-month (53.4), and twelve-month (53.6) averages. The component most resistant to the broader decline is itself slipping.

Confidence in Federal Policies at 39.8 sits below its three-month (41.6), six-month (43.2), and twelve-month (45.1) averages, the steepest erosion of any component when measured against its own recent baseline.

Last month, we said a fragile recovery had been interrupted. This month, the moving averages confirm that the interruption continues. May’s holding pattern is a flat reading on a still-declining trajectory.

Party Dynamics: A Quiet Reshuffle

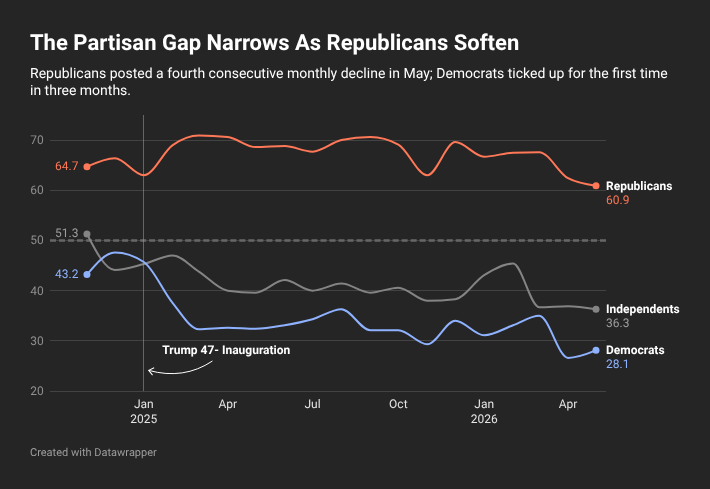

Where April’s decline cut across the board, May’s tells a different story.

Republicans dropped 1.5 points to 60.9, their fourth consecutive monthly decline, and posted their lowest reading of the Trump-47 administration. Democrats ticked up 1.5 points to 28.1, still deeply pessimistic but off their lows. Independents edged down 0.6 to 36.3.

The pattern shows up across all four indexes we track. On the headline Optimism Index, on the Six-Month Outlook, on Personal Financial, and on Federal Policies, Republicans moved down and Democrats moved up. The Democrat–Republican gap narrowed from 35.8 points in April to 32.8 in May.

The shifts are small, and the partisan gap remains historically wide. But the direction is worth marking. The Republican base, which has carried this index through fourteen months of generally weaker economy-wide readings, is showing signs of fatigue. Whether that reflects the policy environment, the geopolitical aftermath, or simply the cumulative weight of nine consecutive months of sub-50 readings, the optimism that lifted the index after the election is fading.

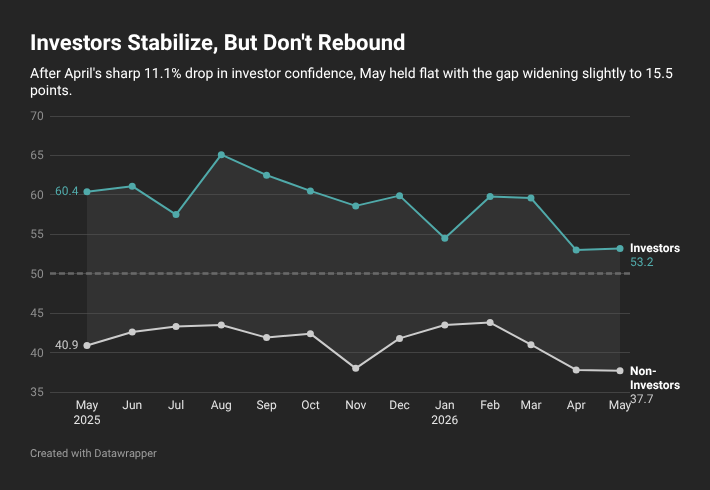

Investor Confidence: Stable, But Isolated

Respondents are considered “investors” if they currently have at least $10,000 invested in the stock market, either personally or jointly with a spouse, directly or through a retirement plan. Investors are typically the most confident segment we track, and remain so.

Investor confidence held practically flat at 53.2, up 0.2 from 53.0 in April. Non-investor confidence ticked down to 37.7 from 37.8. The investor–non-investor gap widened slightly, from 15.2 points to 15.5.

The story here is what didn’t happen. After April’s sharp 11.1% drop in investor confidence (what we described last month as geopolitical uncertainty piercing even the most insulated segment), May saw no rebound. Investors stabilized at the lower level rather than recovering. The advantage over non-investors holds; the recovery has not begun.

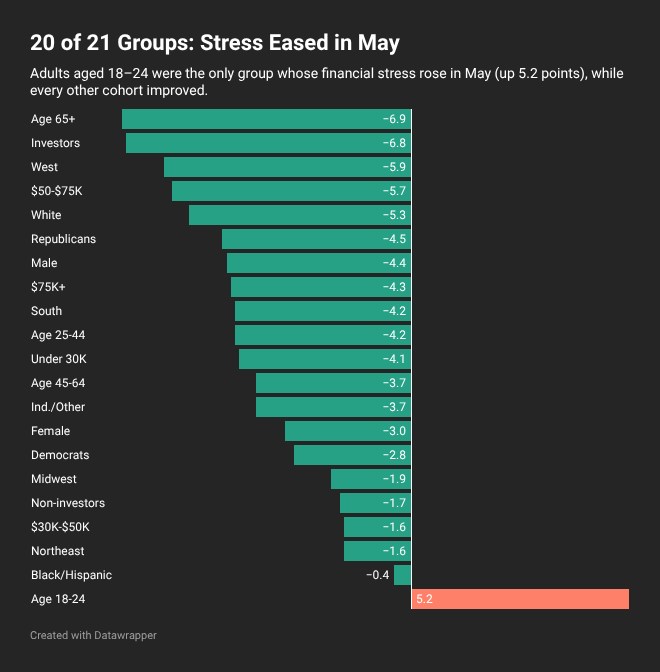

The Demographic Map: Stress Recedes, Optimism Doesn’t

The most striking single number this month sits in the stress data. Of the 21 demographic groups we track, 20 reported lower financial stress in May. The same count that drove April’s optimism story, in reverse.

The biggest stress drops came from groups that had registered the sharpest April spikes: seniors aged 65+ fell 6.9 points (from 67.8 to 60.9), investors fell 6.8 points (65.9 to 59.1), Westerners fell 5.9, middle-income households earning $50K–$75K fell 5.7, and white respondents fell 5.3. April's stress spike has substantially unwound.

However, there is one exception. Stress among adults aged 18–24 rose 5.2 points, from 58.3 to 63.5, the only demographic group to buck the trend. The same age cohort that registered April’s steepest optimism collapse (a 15.2-point drop) is also the only one whose stress kept climbing in May. Whatever is weighing on younger Americans appears structural, not cyclical: their stress is rising while everyone else’s is easing, and their optimism remains depressed at 39.6.

On the optimism side, the picture is harder to read. Only three of the 21 groups are in positive territory in May, the same as April: households earning $75K or more (51.5), Republicans (60.9), and investors (53.2). Nine of 21 groups improved month-over-month, a marked rebound from the single group that improved in April, but the average move was small. The Northeast tumbled 4.5 points to 37.1, the steepest regional decline. Adults aged 25–44, the post-election cohort that had held above 50 through the worst of the recent slide, fell 5.3 points to 47.0, dropping below neutral for the first time in this cycle.

The optimism map remains nearly empty. The map of relief, where stress eased, is nearly full. They are not the same map.

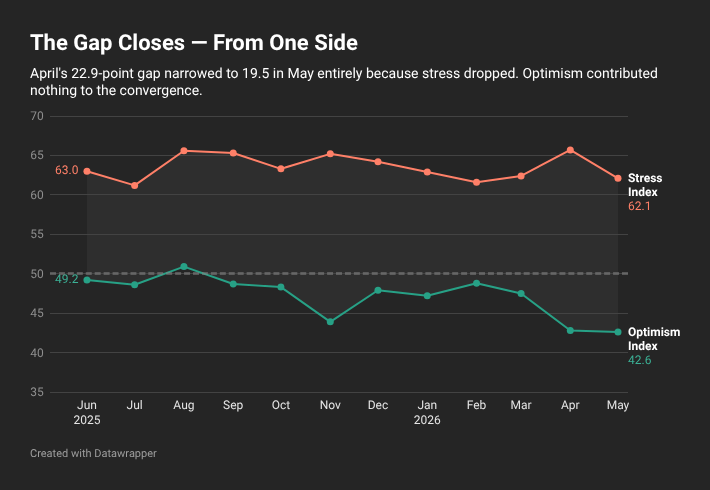

The Stress–Optimism Gap: Still Wide, but Narrower

Last month, we flagged the 22.9-point gap between the Stress Index (65.7) and the Optimism Index (42.8) as the widest in the past twelve months. Americans were not just less hopeful about the economy but visibly more anxious about their finances. In May, the gap narrowed to 19.5 points as stress retreated and optimism held.

A narrower gap is better than a wider one. But 19.5 is still well above the typical reading recorded in recent months, and it closed entirely from the stress side. Optimism contributed nothing to the convergence.

Suspension, Not Recovery

The simplest read of May’s data: the immediate fear lifted, and the underlying judgment did not.

Stress, the most reactive of our measures, fell sharply and broadly. Personal Financial Outlook held its narrow neutral position. But the Six-Month Outlook fell again, Federal Policies confidence was unchanged to the decimal, all moving averages are still declining, and the Republican base, which has supported the headline number for over a year, is showing signs of erosion.

A ceasefire and a Fed meeting closed out April. Neither improved confidence in Federal Policies by a single tenth of a point. Americans are responding emotionally to events, as the stress data shows. They are not responding with restored trust in the policy apparatus. The two are no longer moving together.

For nine consecutive months, this index has read below 50. Three of those nine readings have come below 43. The picture is one of fragile equilibrium: neither a collapse nor a recovery. May is what that suspension looks like in the numbers.

RealClearMarkets/TIPP surveyed 1,464 adults for the May Index from April 28 to May 1. The online survey was conducted using TIPP’s panel network. Results range from 0–100, with readings above 50 indicating optimism, below 50 signaling pessimism, and 50 indicating neutrality. The margin of error is ±2.9 percentage points.

The next report will be released at 10 a.m. EST on June 2, 2026

The TIPP Off

What you should be reading right now

Iran War/Foreign Affairs

US Sinking Iran Ships In Strait, Trump Says— George Caldwell, The Daily Signal

Rubio To Meet With Vatican And Italy Representatives Amid Tensions—George Caldwell, The Daily Signal

Kamikaze Diplomacy—Editorial Board, TIPP Insights

What China Will Learn from Orbán’s Defeat— Sam Chetwin George, Project Syndicate

Economy

The UK Is In Dire Need Of Deregulation—Elias Sánchez, Mises Wire

Government Regulations Create Monopolies And Stifle Competition— Jorge Besada, Mises Wire

Want To Cut Taxes? Reduce Government Spending.—Frank Shostak, Mises Wire

Why “Luck” Doesn’t Explain Wealth And Success In The Marketplace—Joshua Mawhorter, Mises Wire

Goodbye and Good Riddance, Spirit Airlines—Rajkamal Rao, TIPP Insights

Burned By A Red Hot Stove— David Gordon, Mises Wire

Politics

The Big Spending Developments That Could Shape The Midterms—George Caldwell, The Daily Signal

The Real Reason Why Barack Obama Condemned The Supreme Court’s Racial Redistricting Ruling— Tyler O’Neil, The Daily Signal

Nazi Tattoo? Hamas Defender? No Problem, Says Chuck Schumer—David Harsanyi, The Daily Signal

Trump’s New Pick For Surgeon General, Splitting Pro-Life And MAHA Voices— Virginia Grace McKinnon, The Daily Signal

Pro-Choicers Recognize That Abortion Is Too Evil To Even Describe—John Gerardi, The Daily Signal

The Tragedy Of Socialized Fertility—Michael S. Milano, Mises Wire

Trump Crackdown Yields Results: Illegal Aliens Sentenced For Drugs, Guns Trafficking, SNAP Fraud— Fred Lucas, The Daily Signal

Alito Pauses Appeals Court Decision, Keeping Abortion Pill Available Via Mail—Fred Lucas, The Daily Signal

When America Chose Empire— George Ford Smith, Mises Wire

Technology

House Resolution Calls For Tech Companies To Censor Speech—Kurt Nimmo, Ron Paul Institute for Peace and Prosperity

As AI Growth Brings Data Center Boom, Texas Legislators Rush To Protect Constituents—Elizabeth Troutman Mitchell, The Daily Signal

📊 Market Mood — Wednesday, May 6, 2026

🟩 Markets Rally on Hopes for Iran Deal

U.S. futures climbed as reports suggested Washington and Tehran are close to a framework agreement.

🟧 Oil Drops Sharply on De-Escalation Optimism

Crude plunged after signs the Strait of Hormuz could reopen under a potential deal.

🟦 AI Trade Reignites After AMD Blowout

AMD surged on strong earnings and upbeat guidance, reinforcing confidence in AI demand.

🟨 Inflation Fears Ease, But Risks Remain

Lower oil prices helped calm growth and inflation concerns, though energy costs remain elevated versus pre-war levels.

🗓️ Key Economic Events — Wednesday, May 6, 2026

🟧 08:15 ET — ADP Nonfarm Employment Change (Apr)

Expected at 118K (vs. 62K prior), offering an early read on private-sector hiring trends ahead of Friday’s jobs report.

🟧 10:30 ET — Crude Oil Inventories

Expected at -3.400M (vs. -6.234M prior), providing insight into supply conditions as oil markets react to Iran deal headlines.

Letters to the editor email: editor-tippinsights@technometrica.com

Subscribe Today And Make A Difference. Consider supporting Independent Journalism by upgrading to a paid subscription or making a donation. Your support helps tippinsights thrive as a reader-supported publication. Contact us to discuss your research or polling needs.

Reach our audience. For sponsorship and advertising opportunities, visit our Partner With Us page.

{kind=link}