Buried within the 1,100-page bill recently passed by the House of Representatives—the "One Big, Beautiful Bill" that reflects President Trump's priorities—are several provisions that, if enacted into law, could return the U.S. energy sector to a more capitalistic model.

President Joe Biden, with strong backing from environmental lobbyists and a last-minute defection from West Virginia Senator Joe Manchin, pushed through the Inflation Reduction Act and the Infrastructure Bill. These measures allocated billions of dollars in federal credits and loan guarantees to favored industries, all under the banner of environmental protection.

What followed was a Soviet-style industrial strategy in which a handful of Washington bureaucrats determined the winners and losers of America's energy future.

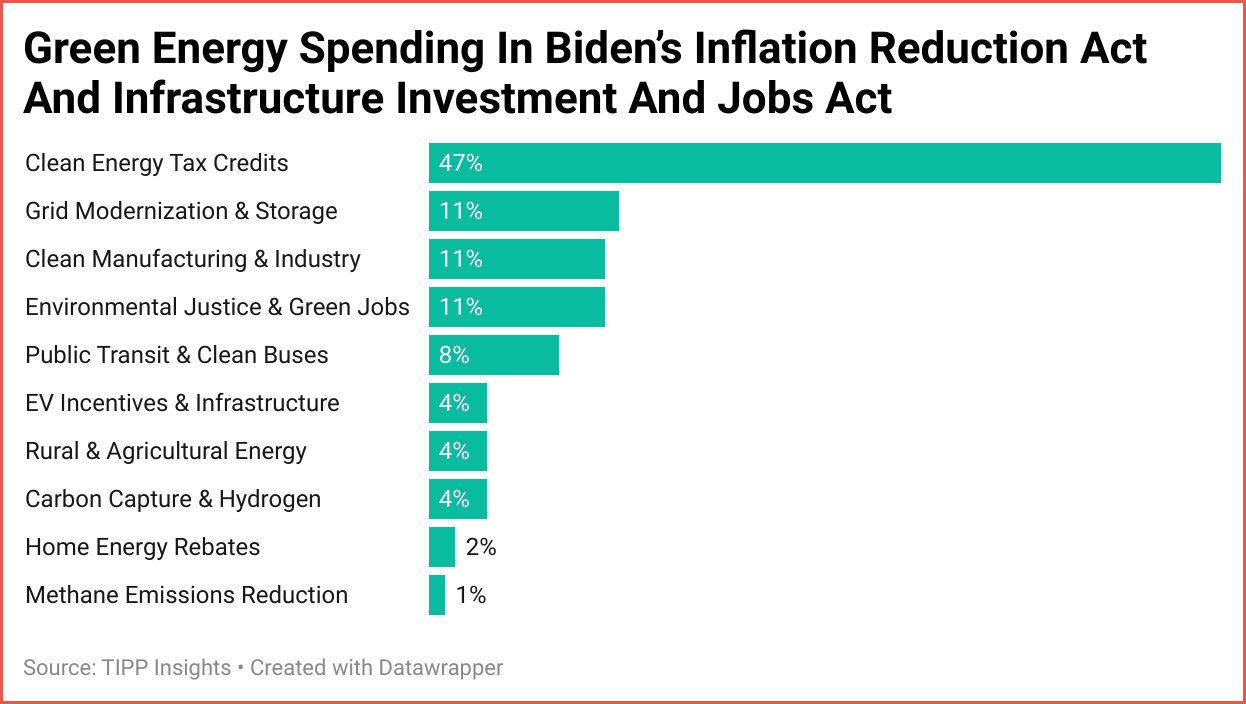

The Inflation Reduction Act (IRA) 2022 contained "Climate and energy investments" of approximately $369 billion over 10 years. These included $270 billion for clean energy tax credits to support wind, solar, geothermal, and other renewables; clean hydrogen production; and carbon capture and storage technologies. Buyers of electric vehicles would get up to a $7,500 tax credit for new EVs and up to a $4,000 tax credit for used EVs (with income and manufacturing origin restrictions). Tax credits and funding for domestic manufacturing of solar panels, wind turbines, batteries, and critical minerals exceeded $60 billion. Rebates for energy-efficient appliance upgrades, heat pumps, insulation, and home weatherization exceeded $60 billion under the Green Jobs and Environmental Justice banner.

With so much federal money up for grabs, greedy entrepreneurs flocked to risky green energy ventures, largely funded by grants and low-interest loans—funding they likely wouldn't have secured through private markets. We all remember the Obama-era Solyndra disaster, but Biden's approach was Solyndra-style investment on steroids.

What was worse, Biden used the vast levers of federal power to kneecap perfectly functioning industries. His administration was especially punitive toward the oil and gas sector: it suspended leases on federal land, blocked vast swaths of the Pacific, Atlantic, and Gulf coasts from new drilling, canceled major pipelines, and imposed regulatory hurdles that made it increasingly difficult for the fossil fuel industry to attract investment capital. As oil prices steadily rose, Biden's energy strategy relied on tapping the Strategic Petroleum Reserve and urging Saudi Arabia to increase production—an ironic move given his simultaneous efforts to restrict Russian oil exports during the Ukraine war.

President Trump, who campaigned once again on the "drill, baby, drill" message, has consistently opposed such government interference in the energy markets. He has long supported removing regulatory red tape and streamlining the permitting process to allow for increased oil production—lowering domestic prices and boosting exports. In December 2019, under Trump's administration, the U.S. Energy Information Administration announced that America had become a net exporter of oil for the first time in nearly 60 years.

Biden's green agenda had another critical flaw: financing. Much of it depended on borrowing from China—ironically benefiting Chinese companies dominating the very industries Biden sought to boost. Since the launch of China's "Made in China 2025" initiative, Chinese firms—heavily subsidized by their government—have taken over more than 85% of the global rooftop solar panel market. Battery components for solar installations have even higher Chinese market dominance. In effect, Biden borrowed money from China to finance the growth of Chinese companies that sold solar products to U.S. installers.

The new House bill aims to dismantle this entire framework in one stroke. It eliminates the trading of green credits between corporations, revokes low-interest green loans, and entirely phases out subsidies for renewable energy initiatives.

To those who claim this approach is irresponsible, we pose a simple question: How many more decades should the green energy sector rely on government aid to stay afloat? Sustainable energy and transition projects are essential, but they must prove their viability in the open market—just like oil and gas companies do every day. This is classic Adam Smith-style capitalism: let competition and innovation—not government favoritism—determine success.

Trump also supports nuclear power, one of the cleanest and most efficient methods of generating electricity. Critics on the Left often call nuclear energy dangerous, but even the most liberal nations—France, Germany, and Japan—have long depended on it. The only significant U.S. nuclear accident, Three Mile Island in the 1980s, did not result in any deaths. Despite Japan's vulnerability to natural disasters, it maintained a strong safety record until Fukushima. The U.S., by contrast, is less prone to earthquakes or tsunamis, yet Congress and successive administrations have consistently stymied progress on nuclear energy.

This week, Trump signed an executive order that could clear the way for small-scale nuclear plants to begin operations within the next 18 months. These modern reactors, based on cutting-edge American technology, are far safer than their predecessors and are designed to power small cities or neighborhoods rather than entire states. Every aspect of nuclear energy today—from fuel storage to waste disposal—is light-years ahead of where it was decades ago. It's a national disgrace that despite having world-class nuclear capabilities—including naval reactors and the world's second-largest nuclear arsenal—our federal policies have hampered the civilian nuclear industry.

By issuing appropriate permitting waivers, Trump aims to unlock this potential, even if a modest federal investment is necessary to overcome ideological resistance from the Left. Energy independence and security should have been the hallmarks of the Obama and Biden administrations. Instead, they catered to the demands of environmental activists and weakened America's energy position.

We are glad to say that the Green New Deal is dead.

TIPP Investing Weekly

Your Snapshot of Last Week's Best Performers

🧠 The TIPP 10

Week Ending: May 23, 2025

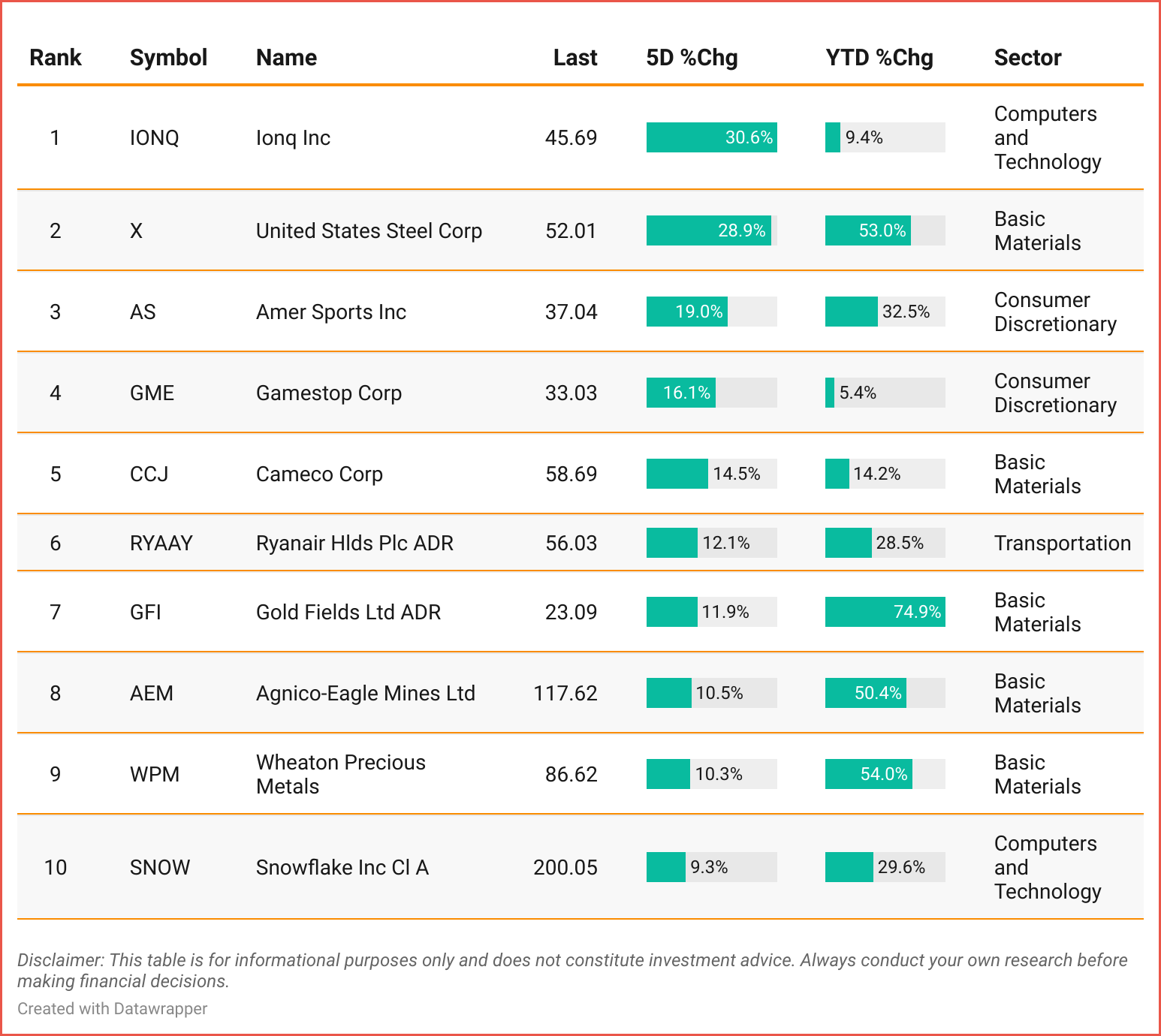

🧾Top 10 Stocks Last Week

A data-driven look at the 10 biggest winners, all above $20 in price, $10 billion in market cap, and 1M in volume.

Tickers: IONQ | X |AS | GME | CCJ | RYAAY | GFI | AEM | WPM | SNOW

🔍 Top Performing Stock Last Week: IonQ, Inc. (IONQ)

IonQ is a College Park, MD–based quantum computing company offering cloud access via Amazon Braket, Microsoft Azure, Google Cloud, and direct APIs.

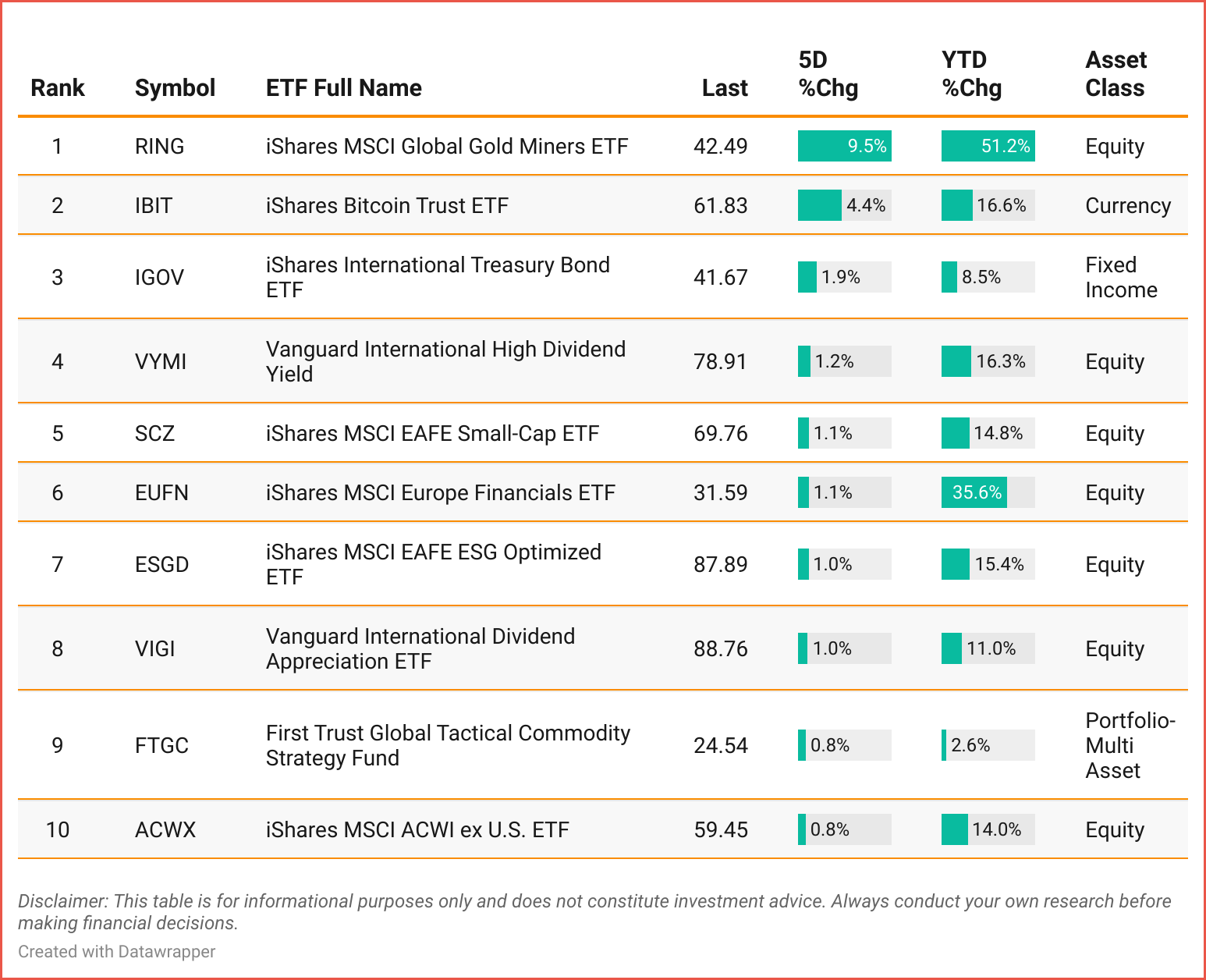

📊 Top 10 ETFs Last Week

A data-driven look at the 10 best-performing non-leveraged, long ETFs priced above $20, with over 300K in average volume and $250 million or more in assets.

Tickers: RING| IBIT |IGOV | VYMI | SCZ | EUFN| ESGD | VIGI | FTGC | ACWX

📈 Top Performing ETF Last Week: RING

RING is the iShares MSCI Global Gold Miners ETF, offering exposure to global companies primarily focused on gold mining.

📅 Key Events This Week

Tuesday, May 27

● 08:30 AM ET – Durable Goods Orders (Apr)

Monthly read on U.S. business investment and manufacturing demand.

● 10:00 AM ET – CB Consumer Confidence (May)

Measures consumer sentiment on current conditions and future expectations.

Wednesday, May 28

● 2:00 PM ET – FOMC Meeting Minutes

Detailed summary of the Fed’s last meeting, offering clues on rate policy.

Thursday, May 29

● 08:30 AM ET – GDP (Q1, QoQ)

Second estimate of economic growth; a key macro health check.

● 08:30 AM ET – Initial Jobless Claims

Weekly read on new unemployment filings, a key signal for labor market strength.

● 12:00 PM ET – Crude Oil Inventories

Weekly update on U.S. oil stockpiles, a vital gauge for energy markets.

Friday, May 30

● 08:30 AM ET – Core PCE Price Index (Apr, YoY & MoM)

The Fed’s preferred inflation measure is critical for rate expectations.

● 09:45 AM ET – Chicago PMI (May)

Snapshot of Midwest manufacturing activity and business conditions.

{kind=link}