By Ryan McMaken, Mises Wire | June 12, 2026

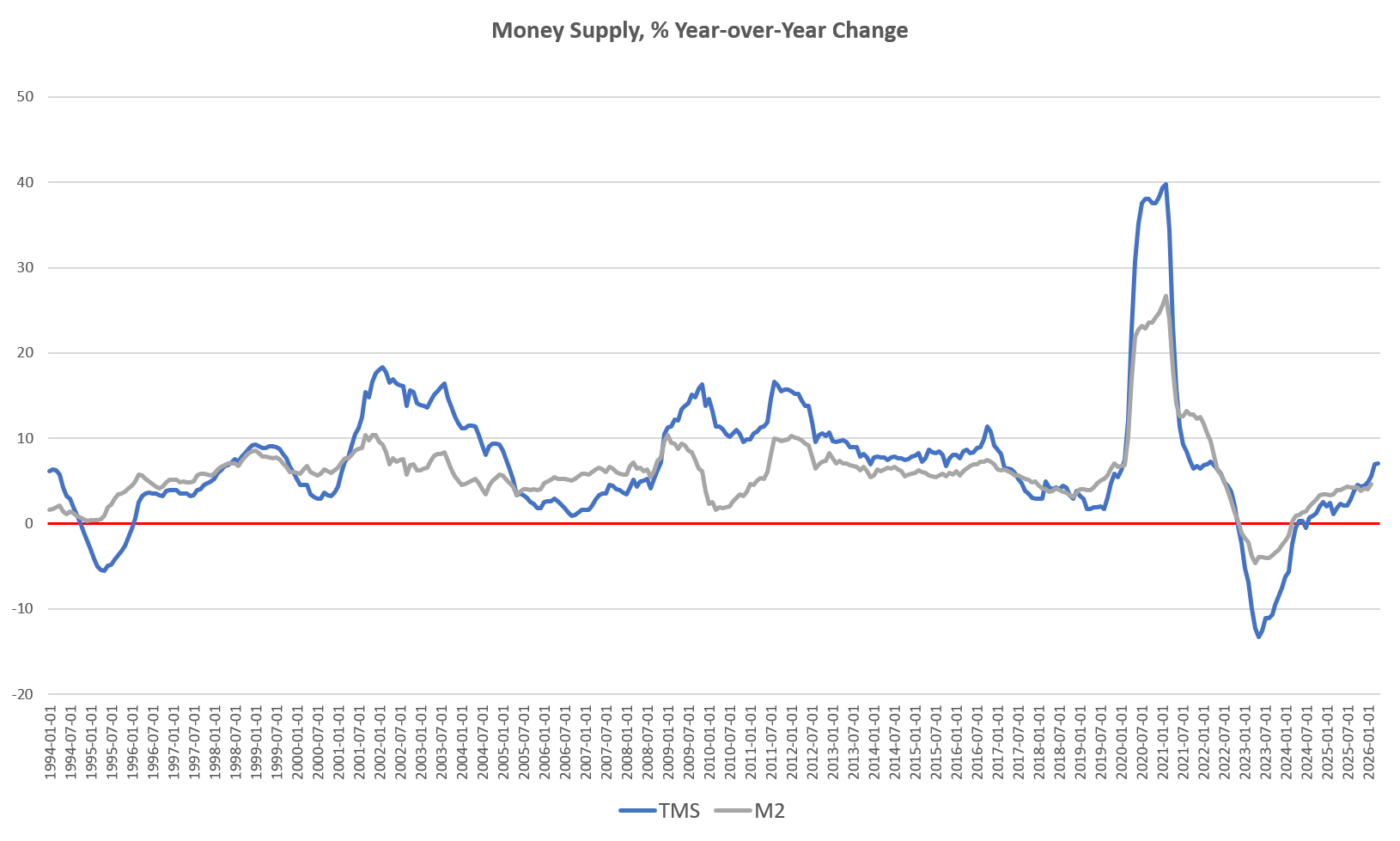

Money-supply growth rose year over year in April, marking the sixth month in a row of accelerating growth, and rising to the largest growth rate in forty-nine months. In spite of repeated claims from the Federal Reserve that monetary policy is at least moderately restrictive, there is no sign of any slowing in money-supply growth. Moreover, the overall fragility of the economy suggests that the Fed will continue to face political pressure toward easing monetary conditions, and this is likely to ensure that we see no real effort at the Fed toward monetary tightening.

More specifically, April’s year-over-year growth in the money supply was at 7.01 percent. That’s up from March’s year-over-year increase of 6.91 percent. April’s increase is also a big change from April 2025 when the year-over-year growth rate was a mere 1.8 percent. Monetary growth has now been positive for 21 months in a row, and Aprils’ growth rate was the highest since March of 2022.

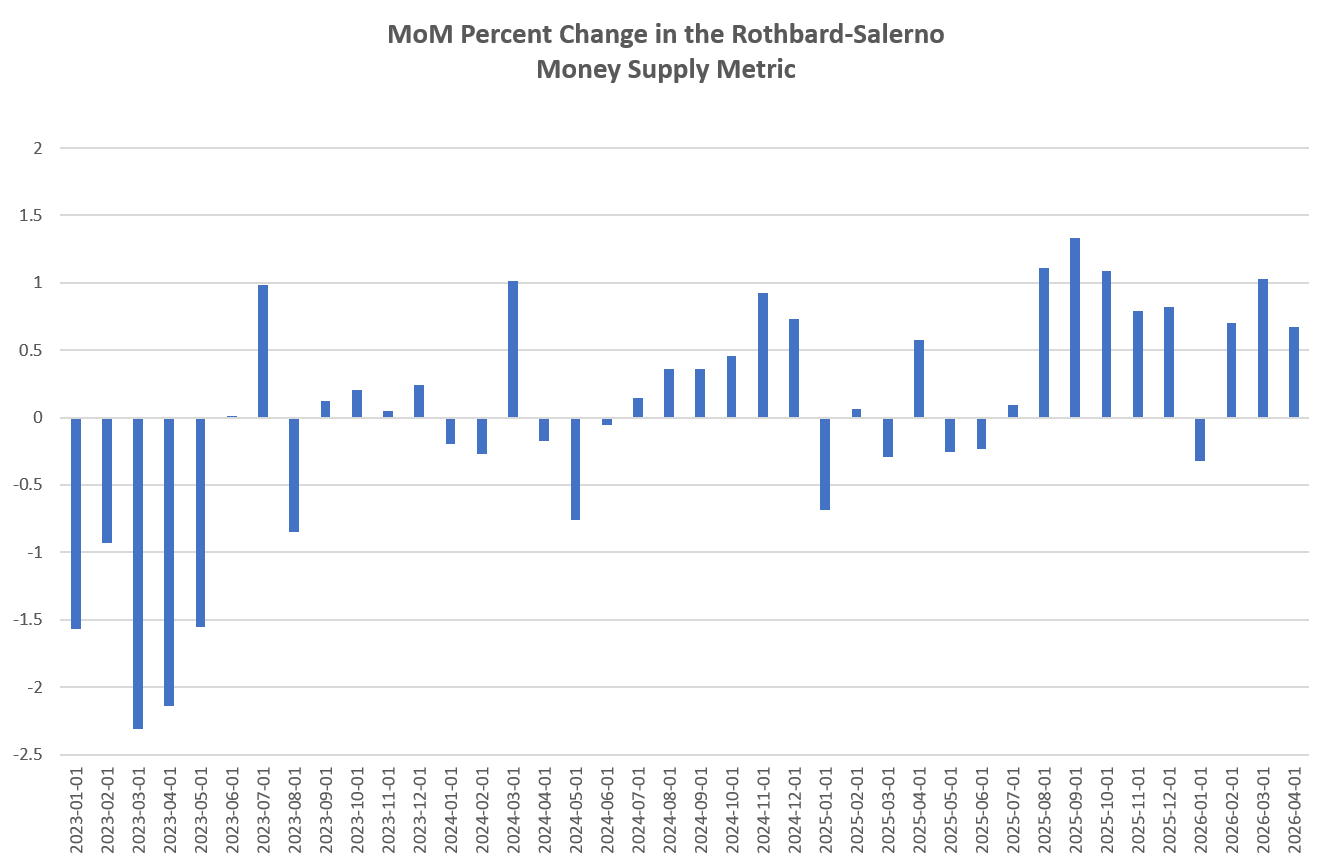

Looking at month-to-month changes in the money supply, we also find an upward trend. The money supply grew 0.6 percent from March to April of this year, the third month in a row for month-to-month growth. Over the past year, the money supply has increased, month over month, during nine of the twelve months:

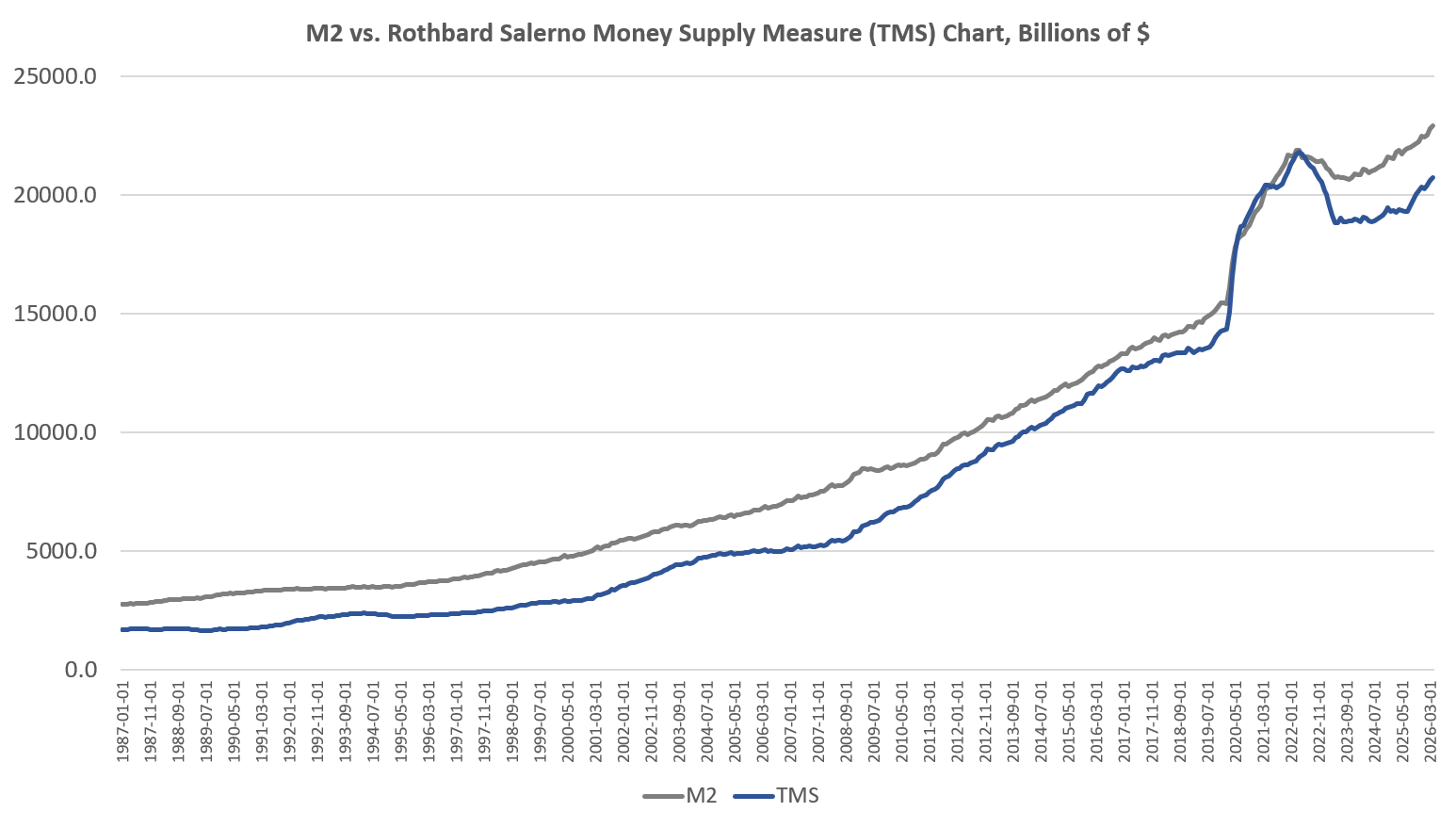

The money supply metric used here—the “true,” or Rothbard-Salerno, money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2. (The Mises Institute now offers regular updates on this metric and its growth.)

In recent months, M2 growth rates have followed a similar course to TMS growth rates, although M2 is growing more slowly than TMS. M2 is now nonetheless at the highest level it’s ever been, including totals reached during the inflationary surge of the covid panic. In April, the year-over-year M2 growth rate was 4.75 percent. That’s up from March’s growth rate of 4.57 percent. April’s growth rate was also up from April 2024’s rate of 3.92 percent. Month over month, M2 increased by 0.5 percent from March to April.

Although year-over-year and month-to-month growth rates may have generally moderated since the runaway monetary-growth years of the Covid Panic, the money-supply growth trend has never returned to where it was pre-2020. From 2020 to 2022, the Federal Reserve’s easy-money policies resulted in approximately 6.4 trillion dollars being added to the economy. This was done to help to finance the federal government’s enormous deficits driven by runaway covid stimulus programs. In order just to get to back to the money-creation trend that existed in 2019 before the “great covid inflation,” total money supply would need to fall by at least three trillion dollars.

Since 2009, the TMS money supply is now up by nearly 194 percent. (M2 has grown by nearly 156 percent in that period.) Out of the current money supply of $19.4 trillion, nearly 26 percent of that has been created since January 2020. Since 2009, in the wake of the global financial crisis, more than $12 trillion of the current money supply has been created. In other words, nearly two-thirds of the total existing money supply have been created just in the past thirteen years.

This acceleration in monetary inflation is likely reflected in recent trends we see in the federal governments economic data. For example, after employment data increasingly showed job-market stagnation throughout much of early 2026, May’s employment report from the BLs showed a re-acceleration in employment. Meanwhile, stock prices have continued to grow robustly, and even home prices—in spite of rising mortgage rates—have failed to fall significantly across the US market overall. Rising home prices are good for asset owners, of course, but less good for first-time home buyers. A similar troubling trend is found in consumer prices which have accelerated since January. In May, the CPI, year over year, rose to 4.1 percent. In that same period, growth in hourly earnings was only 3.4 percent. In other words, real wages in May fell behind price inflation.

None of this should be surprising when we consider that the money supply has grown by nearly half a trillion dollars since January, and that’s all in addition to the cumulative effects of monetary inflation over the past five years.

This mix of rising asset prices, flat wages, and rising consumer prices may also help to explain the public mood. Last month, for example, the Wall Street Journal published an article with the title: “The stock market has never been so good when people have felt so bad.” The article recognizes the disconnect between stock prices—which many have wrongly used as a barometer of market condition for ordinary people—and the general public’s view of economic conditions. For many, wages are not keeping up with prices inflation, and so the public is decidedly less sanguine about the economy than many wealthy asset holders. The WSJ article concludes: “[S]tock prices could be out of touch with the fundamentals of where the U.S. economy is headed and in danger of moving sharply lower. In other words, consumers are right to be unhappy.”

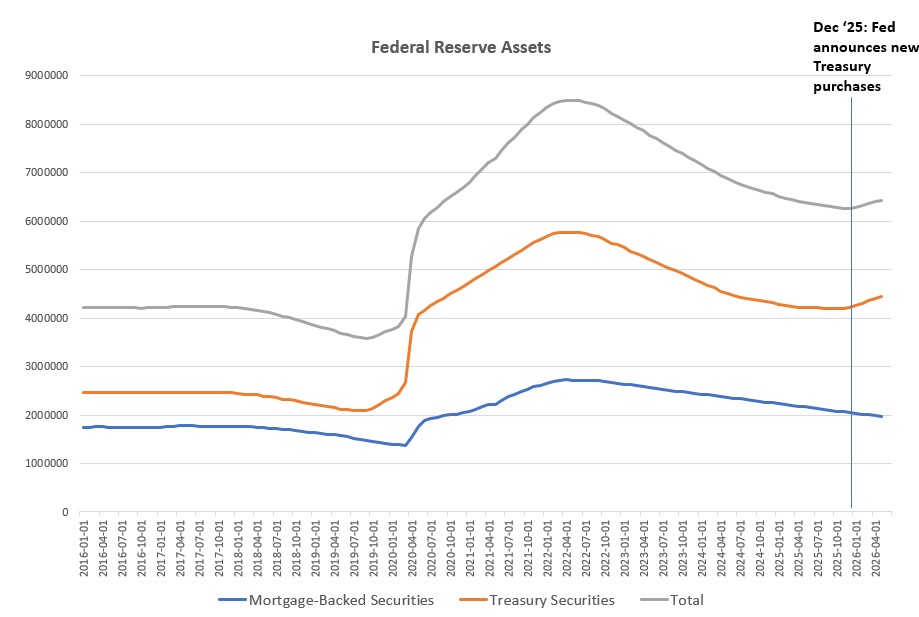

It’s not hard to see how we got here. The central bank has long faced a politically difficult choice. The Fed could back off its nearly two-decade-old policy of inflationist “experimental” monetary policy, but that would quickly lead to a recession and the implosion of countless financial bubbles that have developed from the Fed’s relentless easy-money policies since 2008. Over that period, the Fed bought up trillions in mortgage-backed securities to bail out bankers, while buying trillions more in Treasurys to finance ever-larger amounts of deficit spending. That has all been very good for certain politically connected groups. To abandon this inflationary scheme would be very bad for Wall Street bankers and many wealthy asset holders, and for the parasite class of government contrators and others who rely on deficit spending. At the same time, a return to more reasonable monetary policy would lead to falling prices for ordinary consumers, and a chance to regain some of their lost purchasing power.

That’s the first option.

The Fed—and the regime—have clearly decided to go with the other option. The other option is to pretend to embrace “restrictive” monetary policy while actually pushing monetary growth to multi-year highs and driving price inflation to a three -year high and double the Fed’s target rate. This ensures a continued bonanza for the stock market, at least in the short term, and keeps asset owners feeling wealthy. Trump has even stated that he wants to drive home prices up.

In other words, the regime, through its monetary policy, is picking winners and losers. The winners are wealthy asset owners, government contractors, and the government-parasite class in general. The losers are the young, those with moderate incomes, first-time home buyers, and anyone else with average earnings that aren’t keeping up with price inflation.

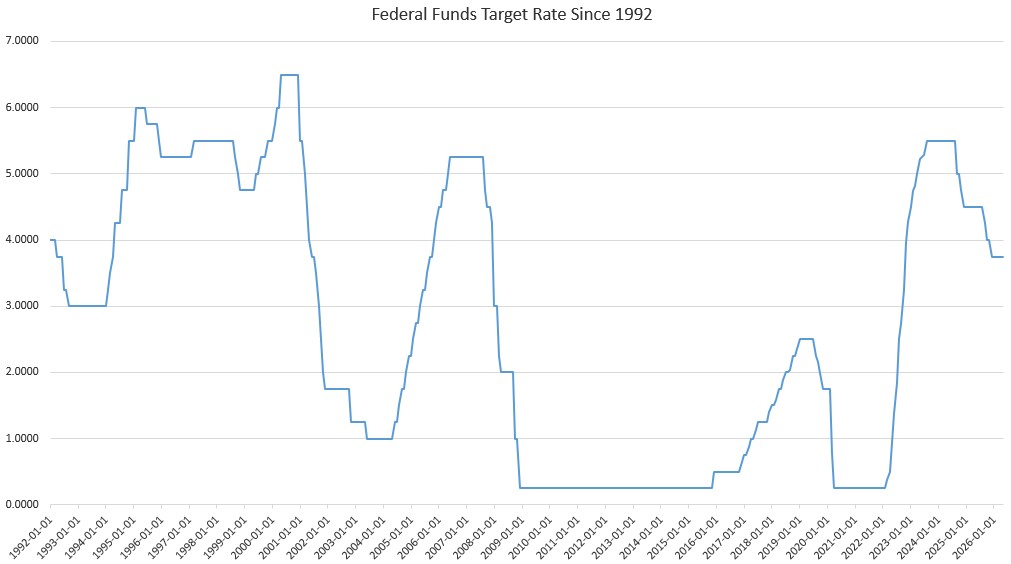

The Fed has chosen the inflationist path. Yet, for years the Fed—i.e., now-former Chair Jerome Powell—was claiming that Fed policy was restrictive. There is no evidence of this. Yes, as price inflation rose to 40-year highs in 2022, the Fed was forced to briefly allow interest rates to rise throughout much of 2023 and 2024. But the Fed reversed itself as quickly as possible, turning back to an easy money policy in late 2024, and forcing down the target policy interest rate by more than 150 basis points.

The following year, the Fed reversed itself on its very moderate balance sheet reductions, against turning back to buying up more than $160 billion in US Treasurys—bought with newly created money—since December of 2025. The Fed’s portfolio is now larger than it was a year ago.

Forcing down interest rates and buying up billions in assets requires infusions of new money. In other words, all of this belies the Fed’s claims of “restrictive” policy. Naturally, the result has been multi-year highs in monetary growth. With next week’s FOMC meeting—the first to be overseen by new Fed chair Kevin Warsh—we’ll get a sense of how the Fed will choose to deal with the upward trend in price inflation and stagnation in employment and wages. It is unlikely we’ll see any significant change from Powell, and the Fed will continue to attempt to create the mirage of monetary restriction and “anti-inflationary” policy while simultaneously refusing to do anything that might upset our current bubble economy and its easy-money largesse for those the regime favors.

Ryan McMaken is editor in chief at the Mises Institute, a former economist for the State of Colorado, and the author of two books: Breaking Away: The Case of Secession, Radical Decentralization, and Smaller Polities and Commie Cowboys: The Bourgeoisie and the Nation-State in the Western Genre. He is also the editor of The Struggle for Liberty: A Libertarian History of Political Thought. Ryan has a bachelor’s degree in economics and a master’s degree in public policy, finance, and international relations from the University of Colorado.

Original article link

{kind=link}