In the Book of Exodus, God sent Moses to Pharaoh with a simple demand: Let my people go. But the Pharaoh refused. So the plagues began, each one worse than the last. After each plague, Pharaoh had the chance to redeem himself. Sometimes he even agreed, then changed his mind once the pressure eased. By the tenth plague, he had lost his economy, his livestock, his crops, and his firstborn son. He could have settled early and lost almost nothing. His pride cost him everything.

Iran has now received its own series of plagues: sanctions, war, a collapsing currency, a naval blockade, and a ship seized at gunpoint. After each episode, the door to negotiation has opened. In every instance, Tehran has hesitated, postured, or walked away. The door is still open. But it will not stay open forever.

Iran is playing one of the oldest tricks in diplomacy: walk away from the table so you can walk back later claiming leverage.

It is a familiar performance. Denounce the other side. Call the process insulting. Threaten to suspend talks. Let domestic audiences see defiance. Then quietly return once concessions are offered, or the pressure eases.

The tactic works only when everyone believes you can afford to stay away.

Iran cannot.

That is why Tehran’s latest insistence that it will not attend talks in Pakistan should be read less as a strategy than as theater. Iranian officials publicly said no final decision had been made. Some insisted there were “no plans to participate.” They cited the U.S. blockade and the seizure of the Touska as obstacles. Yet Pakistani mediators report Tehran is still positively reviewing participation, even as a high-level U.S. delegation, including Vice President JD Vance, Jared Kushner, and Steve Witkoff, heads to Islamabad.

Publicly, Iran says “no talks.” Privately, it knows talks are unavoidable.

The reason is simple: the clock is ticking, and the bill is mounting. As this editorial board noted yesterday, the IRGC controls roughly a third of Iran’s economy and received 51% of all oil and gas export revenue in the latest budget. That machine has to make payroll. Every day without a deal, it gets harder to meet the payroll.

The Pakistan-brokered two-week ceasefire is due to expire midweek. President Trump has signaled that there will be no easy extension. If it lapses, military strikes can resume, the naval blockade can tighten, and the narrow opening for diplomacy can evaporate quickly.

Even without renewed conflict, the economic strain is crushing. The U.S. blockade has already halted roughly 1.8 million barrels per day of Iranian oil exports - a revenue lifeline. Iran’s storage capacity buys it only weeks, at most two months, before forced production cuts become inevitable.

Iran’s economy was already reeling before this crisis. Inflation hovers near 47%, with food prices up by more than 100% in recent months. The rial has plunged to record lows around 1.5 million per U.S. dollar. The central bank has been forced to issue a new 10-million-rial banknote, the largest ever, just to keep pace. Wartime damage to energy infrastructure, power plants, and steel facilities has compounded the pain. The government is increasingly hard-pressed to meet payrolls and public expectations.

The seizure of the Iranian-flagged cargo ship Touska this week proved the blockade is not mere talk. After a six-hour standoff, the USS Spruance disabled the vessel’s engine room with gunfire. Marines rappelled from the USS Tripoli and took custody of the ship. Tehran threatened retaliation but has not acted. The message was clear: the blockade is real and it is tightening.

Trump once wrote that the worst position in a deal is looking desperate to make it. Iran’s walkout is designed to project the opposite. But when your currency has lost 20,000 times its value, and your president is asking parliament where the money will come from, the desperation is visible from across the table.

Delay tactics can be useful when a government hopes pressure will ease or the other side will blink first. But delay is expensive when your economy is under strain, and the threat of retaliation is real.

This is where economics becomes more powerful than posturing. A government that has already faced waves of protests over inflation and living costs is not negotiating from a position of comfort. Facing wartime damage and a naval blockade, they are negotiating out of necessity.

That does not mean Iran has no cards to play. Geography matters. Energy markets matter. Iran can impose costs and create uncertainty.

But leverage is not the same thing as strength. Strength is having time on your side. Strength is having reserves to absorb pressure. Strength is being able to walk away and stay away.

Iran is not really walking away from the table. It is haggling over the terms of sitting back down. Sooner or later, the cameras stop rolling, and the numbers take over.

Pharaoh waited through ten plagues before he finally relented. By then, the cost was beyond calculation. Tehran may leave the room for appearances' sake. But the plagues are mounting, the ceasefire clock is ticking, and the bluff has been called.

👉 Show & Tell 🔥 The Signals

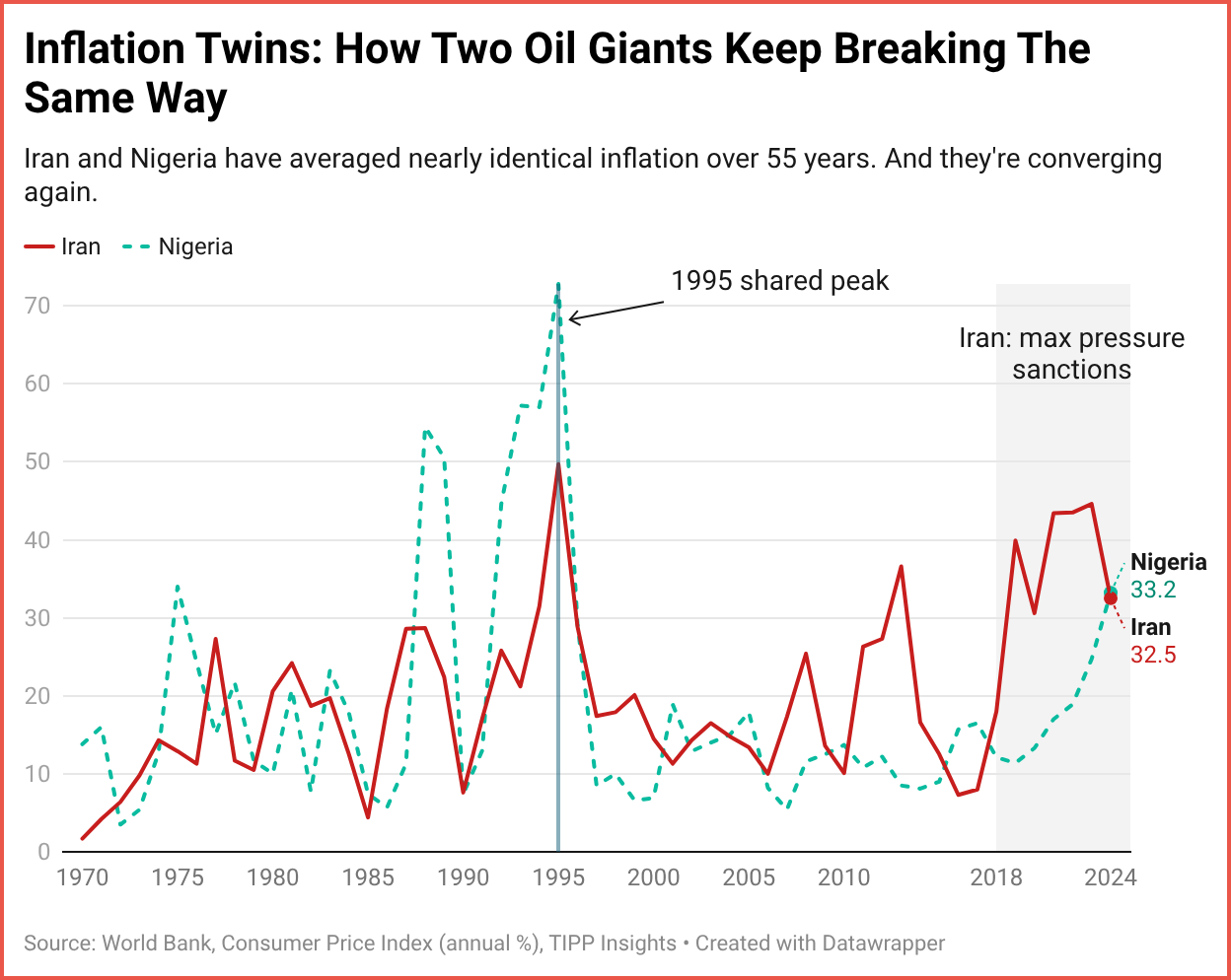

I. Iran And Nigeria: Two Peas In An Inflation Pod

A TIPP Insights analysis of World Bank inflation data reveals a striking pattern: Iran and Nigeria, two countries with almost nothing in common politically, have been breaking the same way economically for over half a century.

One is an Islamic theocracy under heavy sanctions. The other is a young democracy trying to liberalize its economy. But look at their inflation numbers side by side and the similarities are hard to ignore.

Over the past 55 years, Iran has averaged about 20% annual inflation. Nigeria sits at 18.6%. Both hit their worst point in the same year, 1995, with prices rising nearly 50% in Iran and over 70% in Nigeria. The correlation between the two is statistically significant, and it is not a coincidence.

The link is oil dependency. Both countries rely heavily on crude exports to fund their governments. When oil prices crash, both face the same ugly choice: print money, devalue the currency, or squeeze imports. Both tend to print and delay, which sends prices spiraling.

What makes this moment especially interesting is that the two are converging again. Iran has been stuck above 40% inflation for years, locked in by sanctions that cut off its access to global markets. Nigeria just crossed 33% after President Tinubu unified the exchange rate, causing the naira to plunge. Different policy triggers, same result for ordinary people watching the cost of groceries climb every week.

The question worth watching: is Nigeria sliding into the kind of entrenched inflation trap that Iran has been unable to escape? Or will opening up the economy eventually do what isolation never could?

📊 Market Mood — Tuesday, April 21, 2026

🟩 Markets Edge Higher as Ceasefire Clock Ticks

U.S. futures rose modestly as investors bet talks may extend the fragile U.S.-Iran truce.

🟧 Oil Slips on Hopes for Hormuz Relief

Crude eased as traders anticipated renewed negotiations could stabilize key supply routes.

🟦 Fed Independence Back in Spotlight

Kevin Warsh’s confirmation hearing renewed focus on rates, inflation, and central bank autonomy.

🟨 Earnings Wave Meets Leadership Shifts

A heavy earnings slate and Apple’s CEO transition added another layer for markets to digest.

🗓️ Key Economic Events — Tuesday, April 21, 2026

🟧 08:30 ET — Retail Sales (MoM, Mar)

Expected at +1.4% (vs. +0.6% prior), offering a key read on consumer spending momentum.

🟧 08:30 ET — Core Retail Sales (MoM, Mar)

Expected at +1.3% (vs. +0.5% prior), excluding autos and providing a cleaner view of underlying demand.

editor-tippinsights@technometrica.com

{kind=link}