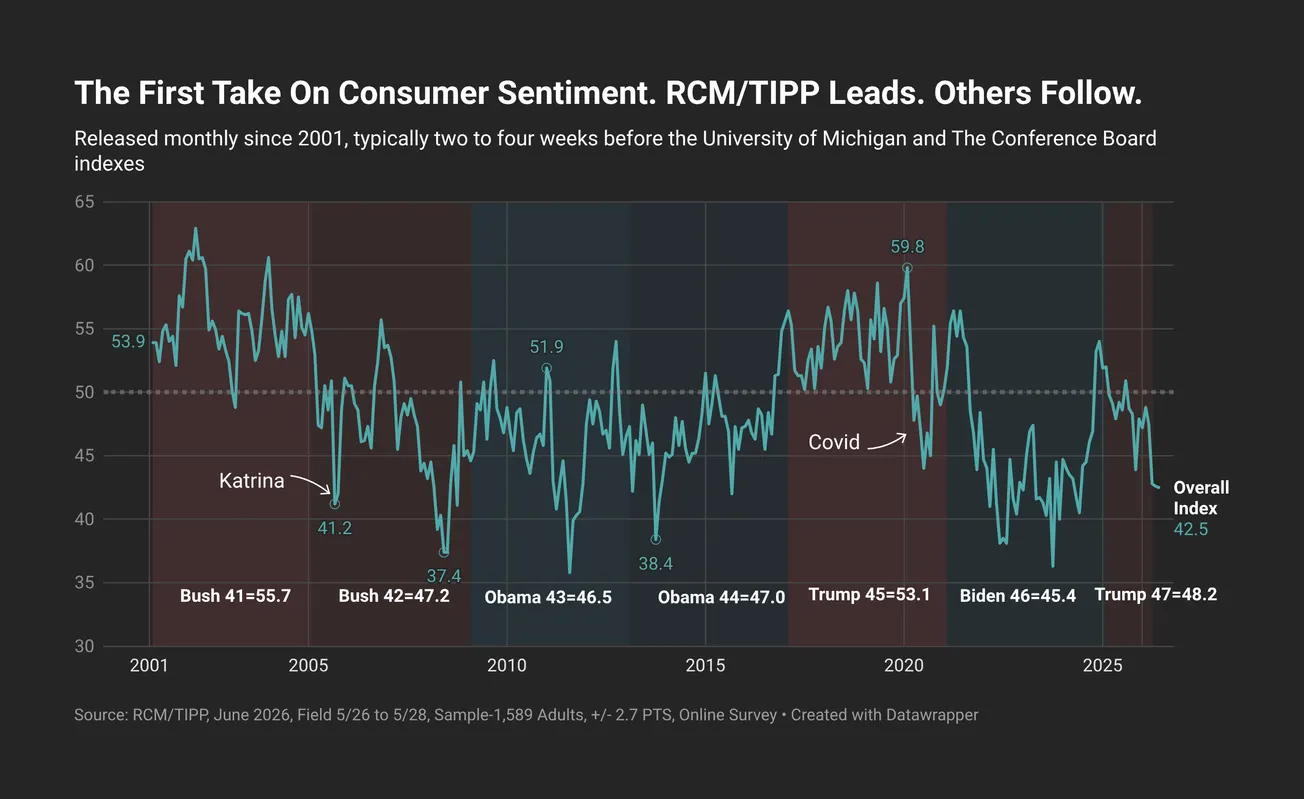

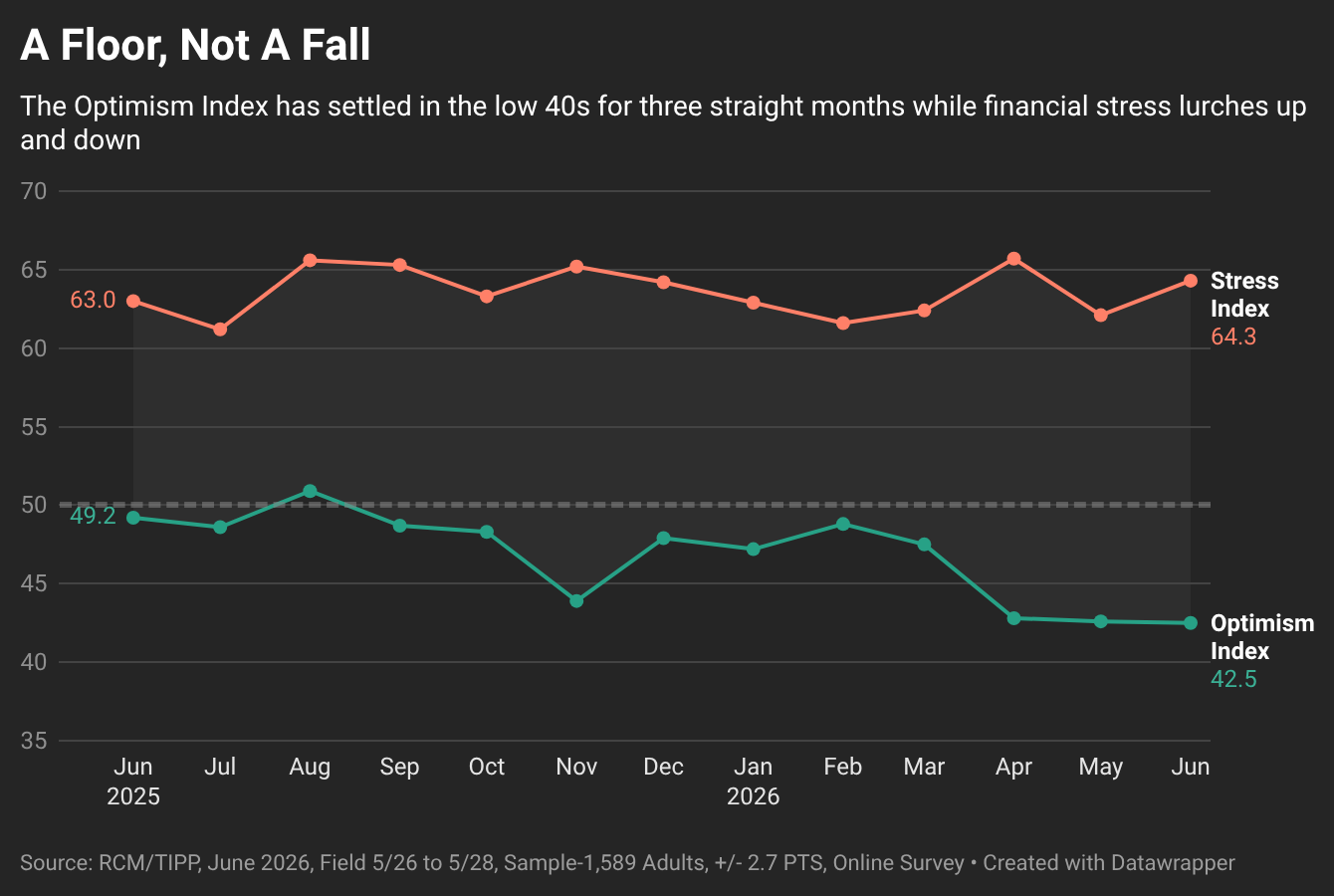

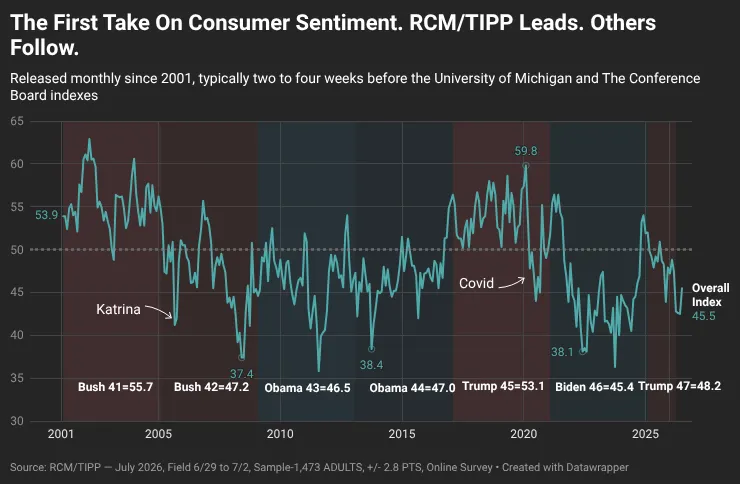

Consumer sentiment held near its lows in June. The RealClearMarkets/TIPP Economic Optimism Index, the first monthly read on U.S. consumer confidence, edged down to 42.5 from 42.6 in May, a decline of just 0.1 points. After April’s 4.7-point plunge, the headline has now spent three consecutive months parked in the low 40s: 42.8, 42.6, and 42.5. The decline has stabilized at a low level.

The index has now remained below the neutral 50 mark for ten consecutive months, keeping the nation in what we classify as the pessimism zone. The last reading at or above 50 was August 2025, at 50.9.

June’s reading of 42.5 is 13.4% below the 305-month historical average of 49.1, and ranks as the 35th-lowest reading out of 305 since the index began in February 2001.

The RCM/TIPP Economic Optimism Index has a strong track record of anticipating the consumer-confidence indicators later released by the University of Michigan and The Conference Board. From February 2001 to October 2023, TIPP released this index monthly in collaboration with its former sponsor and media partner, Investor’s Business Daily.

RCM/TIPP surveyed 1,589 adults for the June index from May 26 to 28, using TIPP’s panel network; the margin of error is ±2.7 percentage points. Results range from 0 to 100, with readings above 50 indicating optimism, below 50 signaling pessimism, and 50 neutral.

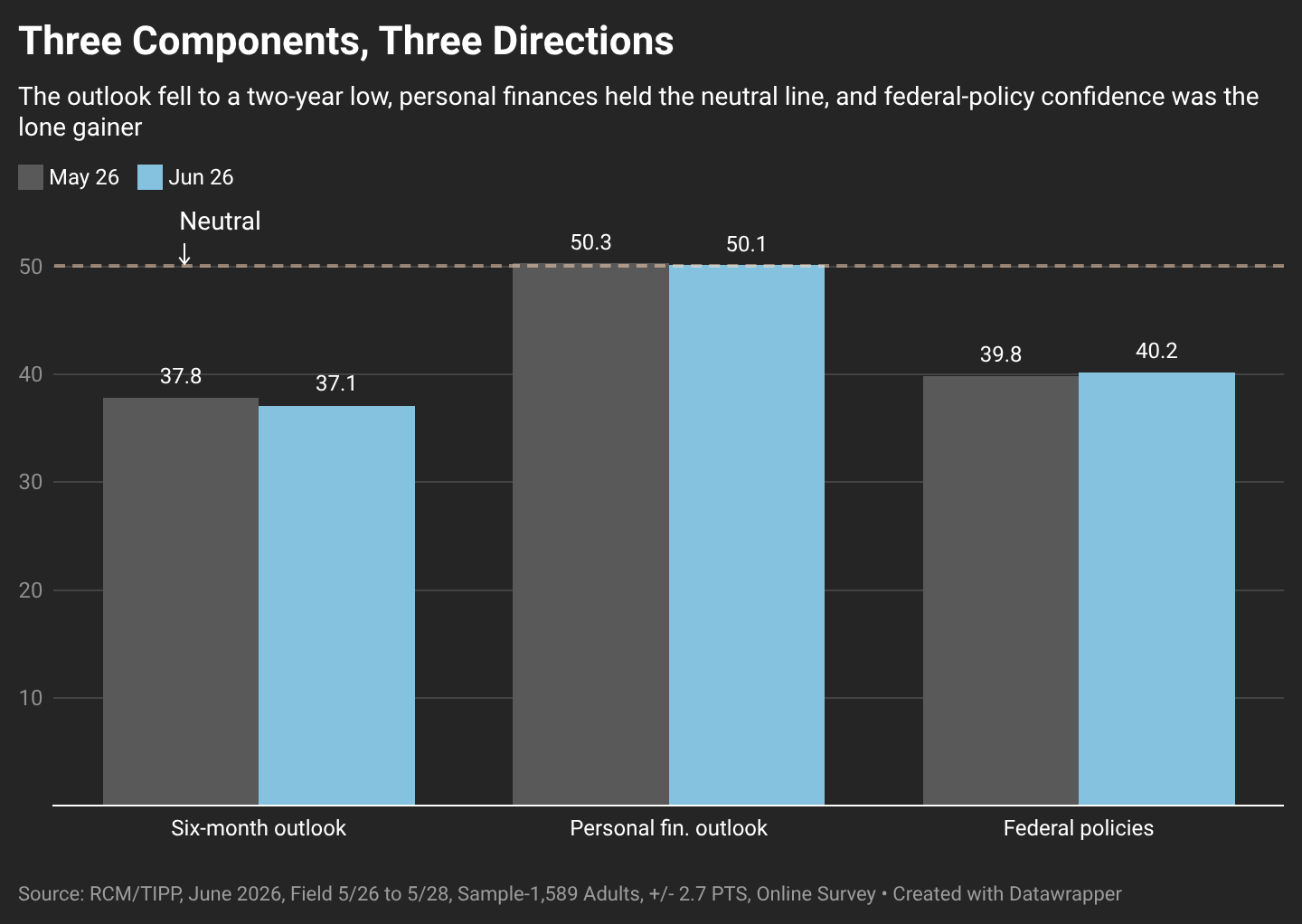

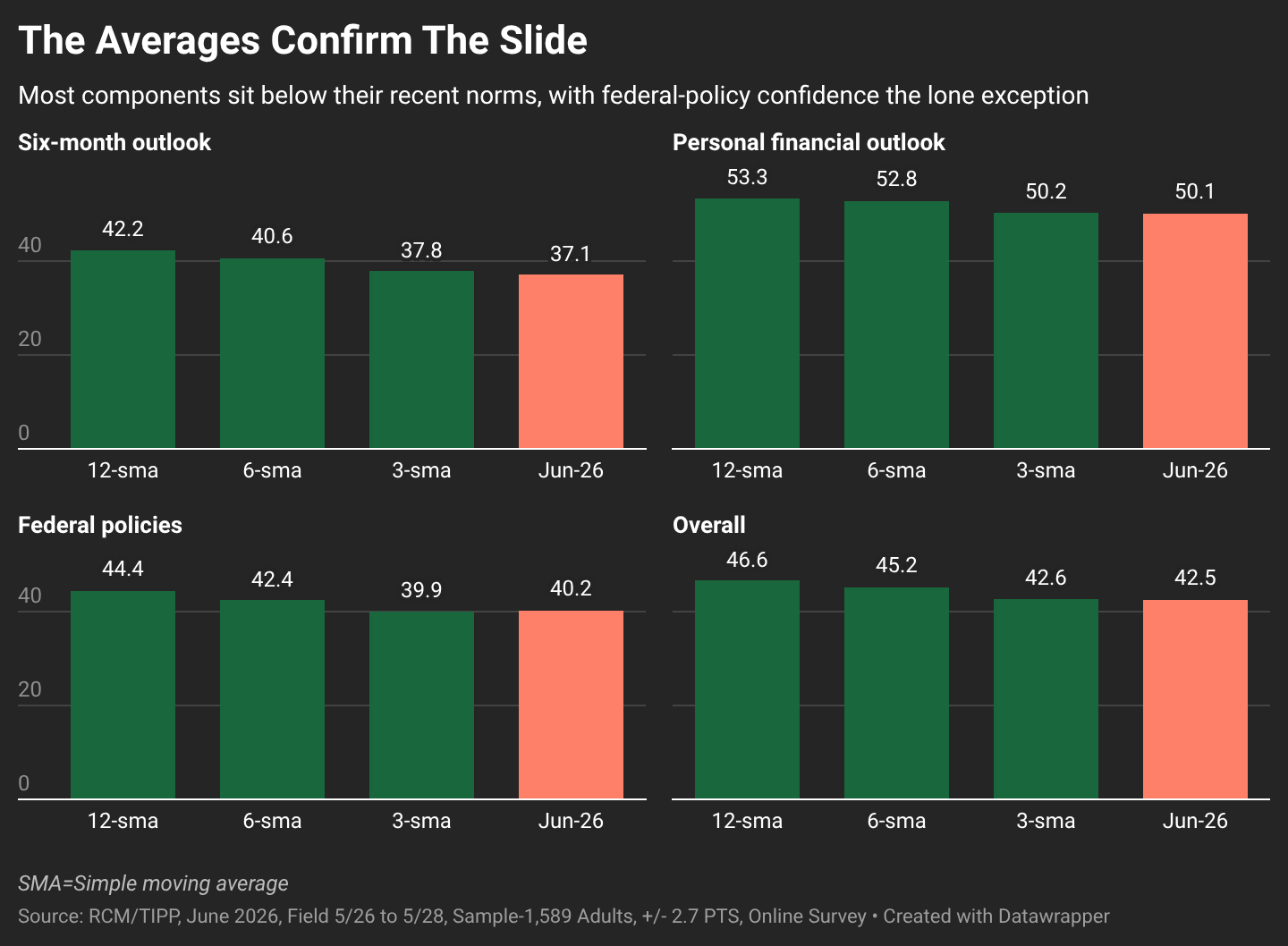

The RCM/TIPP Economic Optimism Index has three key components. In June the picture was again mixed: one fell further, one held near neutral, and one ticked higher.

- The Six-Month Economic Outlook, which measures how consumers perceive the economy’s prospects over the next six months, declined 1.9%, from 37.8 in May to 37.1 in June, its lowest reading in two years, last seen in June 2024.

- The Personal Financial Outlook, a measure of how Americans feel about their own finances over the next six months, held near neutral, edging down 0.4% from 50.3 to 50.1, still the only component anchored at the 50 line.

- Confidence in Federal Economic Policies, a proprietary RCM/TIPP measure of views on the effectiveness of government economic policies, rose 1.0%, from 39.8 to 40.2, the only one of the three components to gain ground this month.

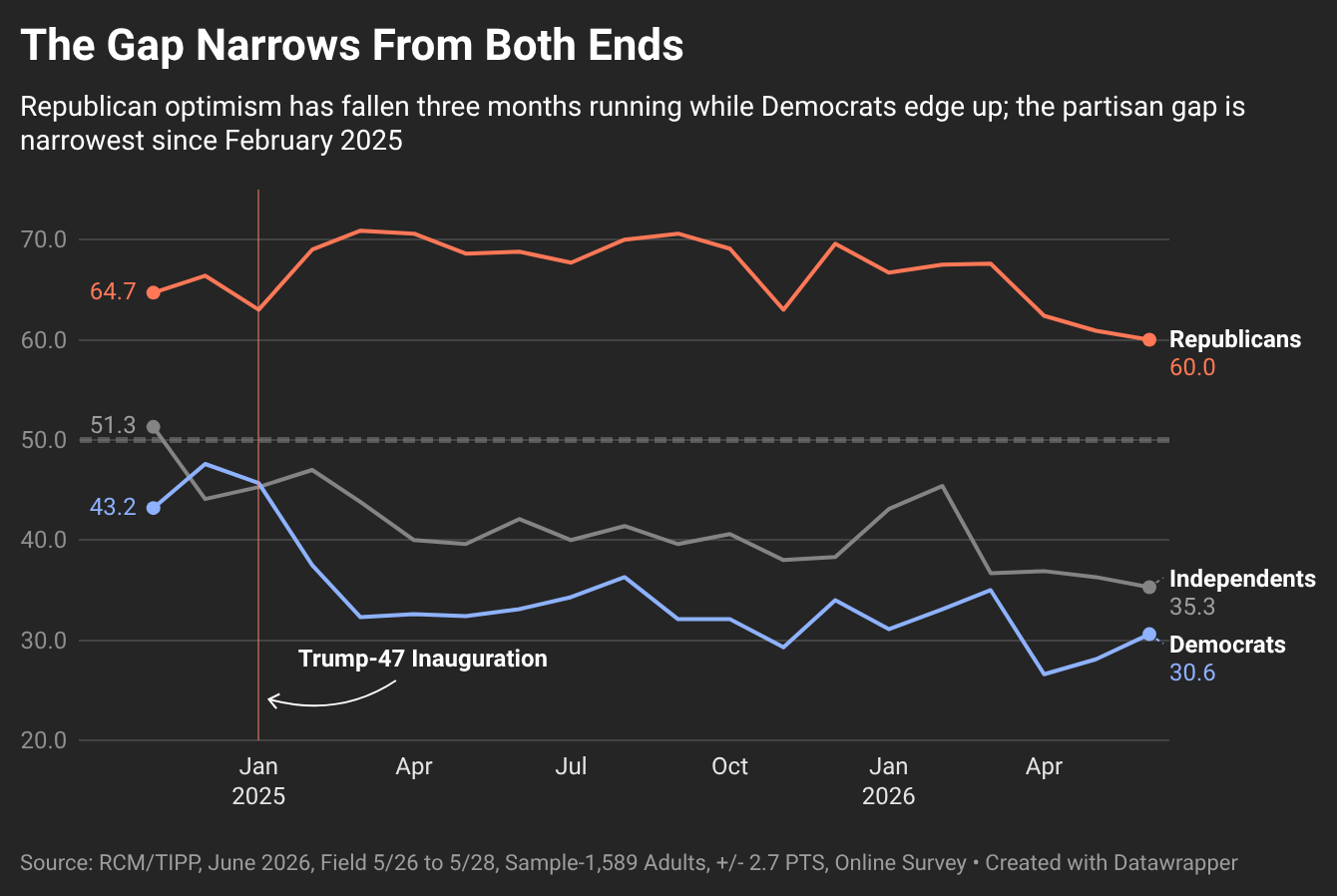

Party Dynamics

Republicans slipped 0.9 points to 60.0, a third straight monthly decline from a March peak of 67.6 and their lowest reading of the Trump-47 era. Democrats rose 2.5 points to 30.6, a second consecutive gain but still deeply pessimistic. Independents edged down 1.0 to 35.3. The Democrat-Republican gap narrowed from 32.8 points in May to 29.4 in June.

The moves are small and the partisan gulf remains historically wide, but the post-election lift that had propped up the headline continues to fade.

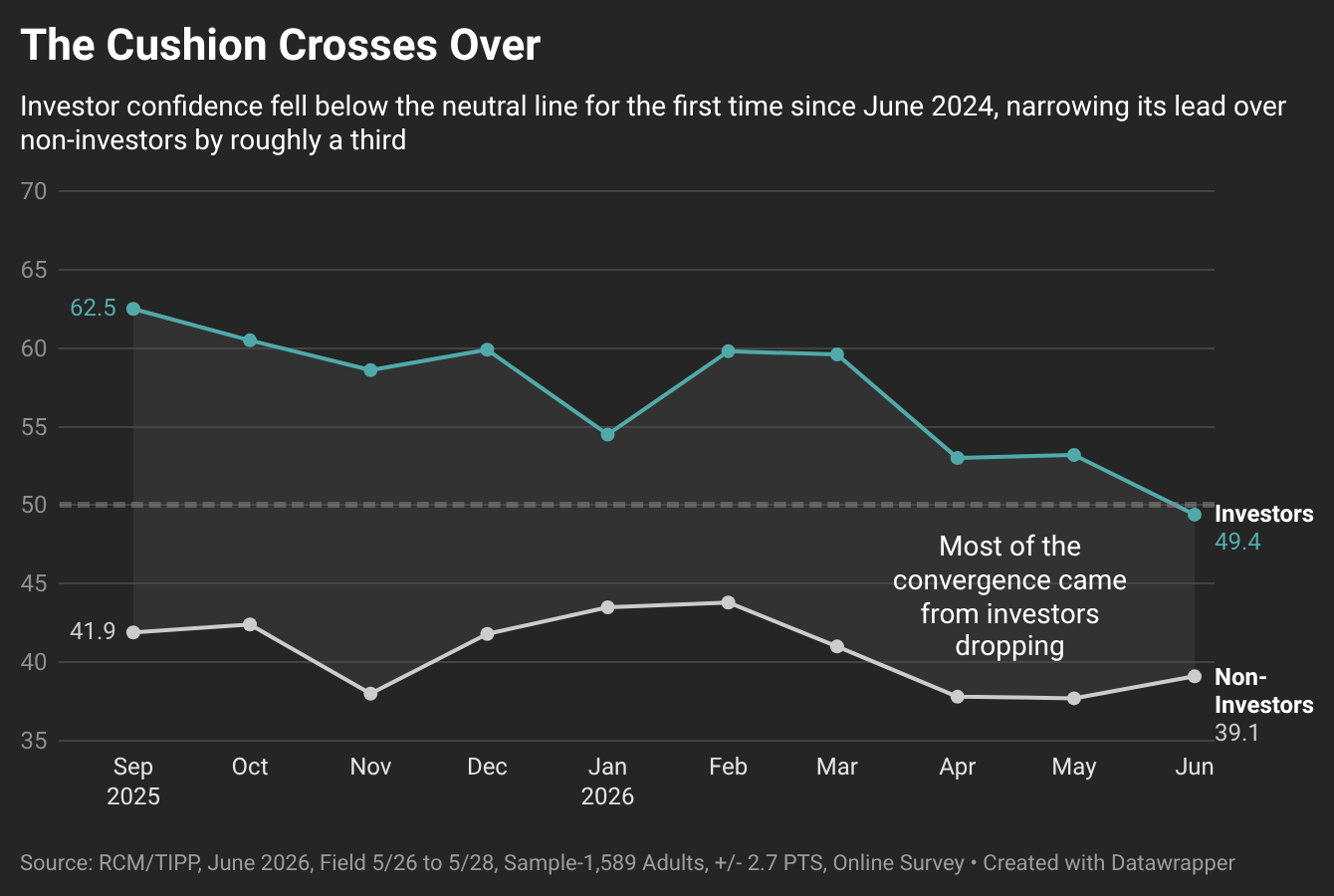

Investor Confidence

Respondents are counted as “investors” if they hold at least $10,000 in the stock market, personally or jointly, directly or through a retirement plan. They are typically the most confident segment we track. In June, that confidence slipped into pessimism for the first time in two years.

Investor confidence fell to 49.4 from 53.2, dropping below the neutral 50 line, while non-investor confidence rose to 39.1 from 37.7. The gap between the two narrowed sharply, from 15.5 points to 10.3. Most of that narrowing came from investors falling rather than non-investors gaining.

The decline shows up across investors’ own readings: their six-month outlook fell 4.6 points, their personal-finances reading fell 4.3, and their confidence in federal policies slipped 2.5, even as their financial stress barely moved. The shift reflects weaker expectations about the months ahead, the same force weighing on the headline.

Momentum

The Optimism Index at 42.5 now sits at or below its three-month (42.6), six-month (45.2), and twelve-month (46.6) averages, and the step down through those windows confirms a year-long loss of momentum. The Six-Month Outlook at 37.1 trails all three of its averages by the widest margin of any component, while the Personal Financial Outlook at 50.1 has slipped below its own benchmarks toward the neutral line it has defended all year. Confidence in Federal Policies, at 40.2, is the lone component to edge above its three-month average (39.9), though it remains well beneath its six- and twelve-month marks.

Demographic Analysis

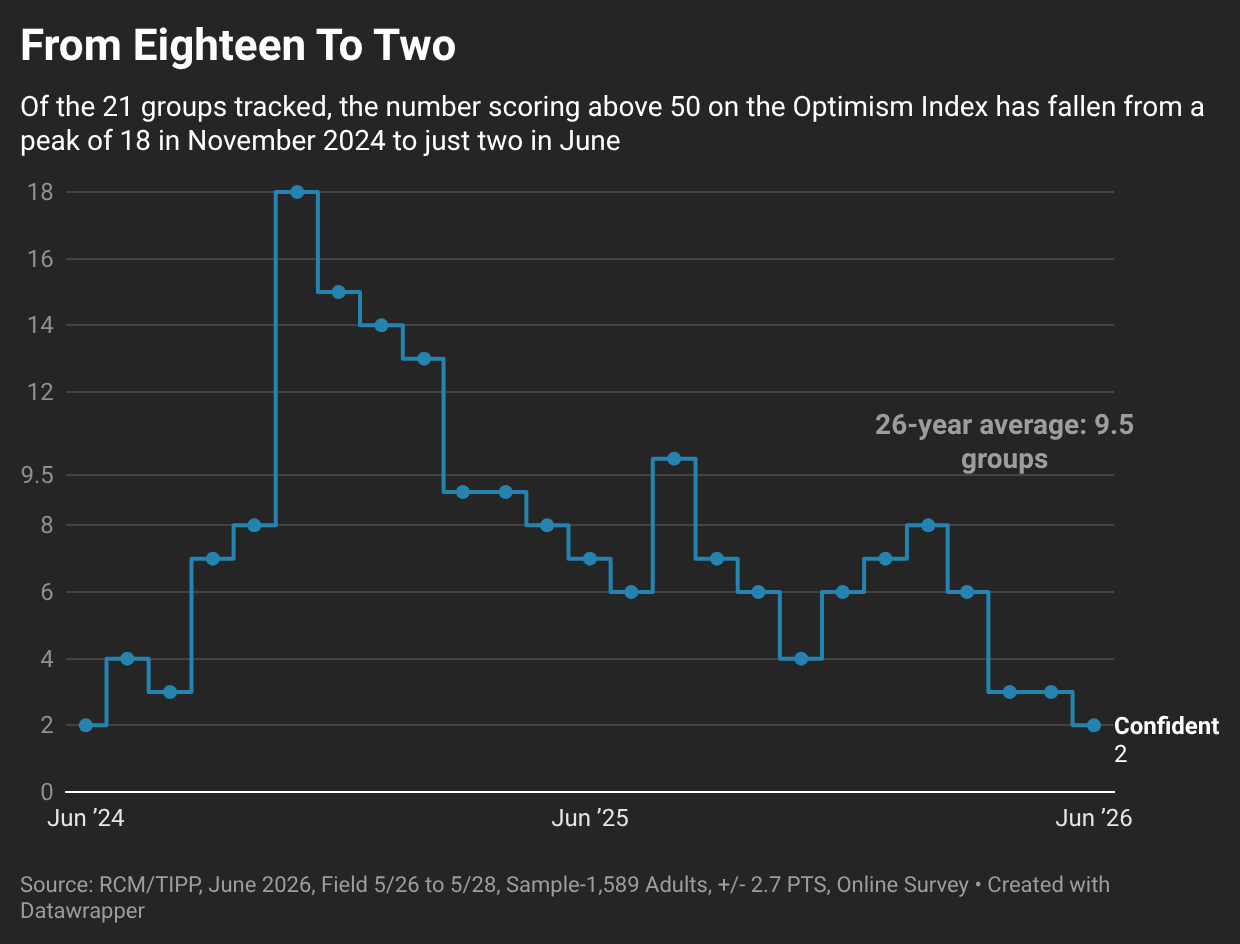

The number of groups in positive territory measures the breadth of optimism across American society. This month, only two of the 21 demographic groups RCM/TIPP tracks, the youngest adults (18–24) and Republicans, scored above 50 on the Economic Optimism Index, down from three in May and six in March. Nine groups improved their reading month over month.

Financial Stress

RCM/TIPP also releases a companion measure, the RCM/TIPP Financial-Related Stress Index, the only monthly metric tracking the financial stress Americans feel. The gauge runs opposite to the optimism index: the higher the number, the more stress, with readings above 50 signaling elevated strain and 50 neutral.

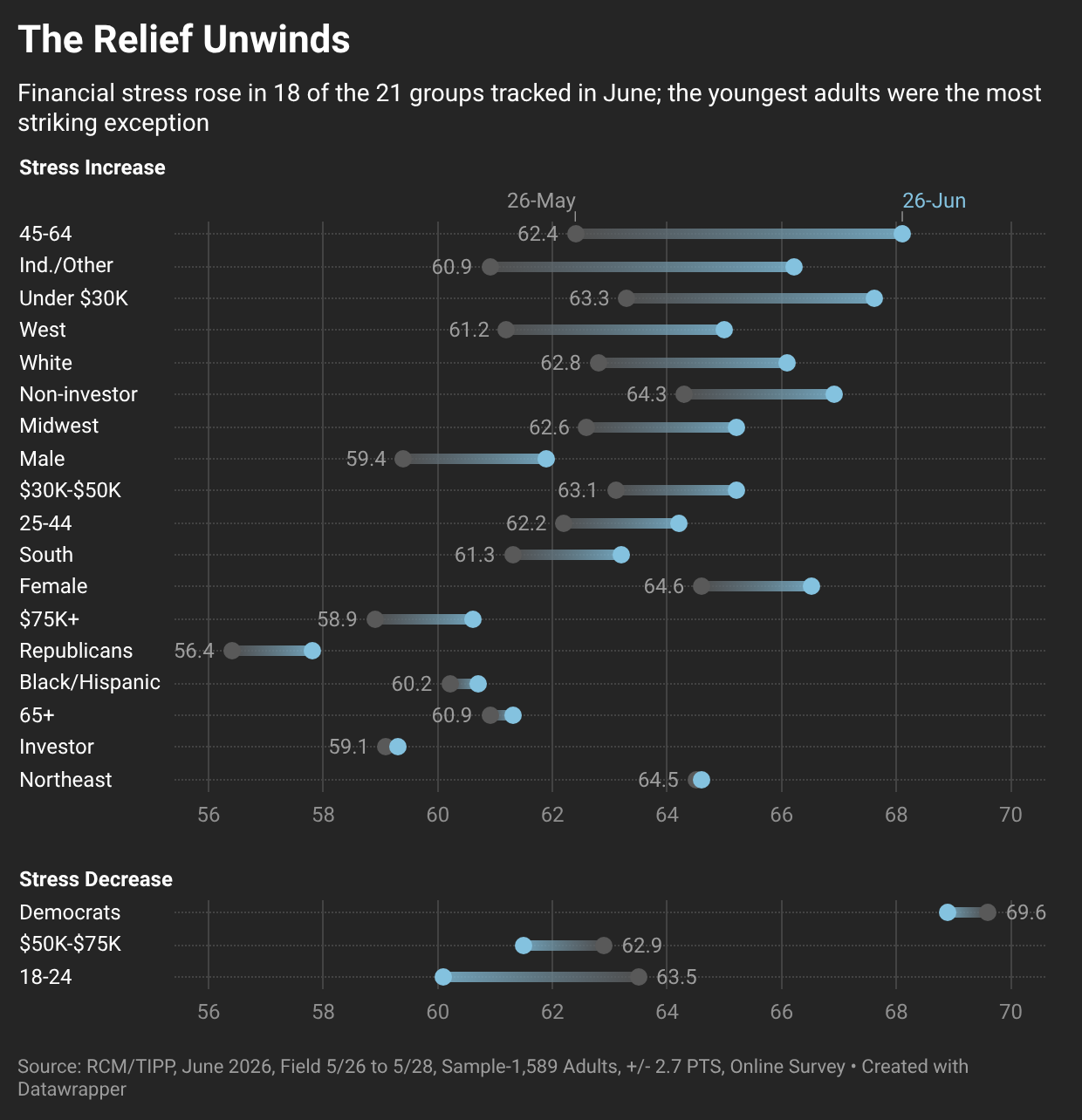

The Stress Index rose 2.2 points, or 3.5%, from 62.1 in May to 64.3 in June, giving back much of the relief recorded the prior month. It has averaged 60.5 since December 2007, and June’s reading sits 6.3% above that long-term norm. The last time it fell below 50 was February 2020, just before the pandemic, at 48.1.

The strain was broad. Eighteen of the 21 groups we track reported higher stress in June, a near-mirror of May, when 20 of 21 saw it ease. The sharpest increases came largely from the groups that had posted the deepest relief a month earlier, among them adults aged 45–64 (up 5.7 points to 68.1), independents (up 5.3), and lower-income households under $30K (up 4.3).

The striking exception was the youngest cohort. Adults aged 18–24, the only group whose stress rose in May, saw it ease in June, down 3.4 points to 60.1. Last month we read the weight on younger Americans as structural rather than cyclical; June argues the opposite, and in a small, high-variance subsample what looked like a structural break may simply be volatility.

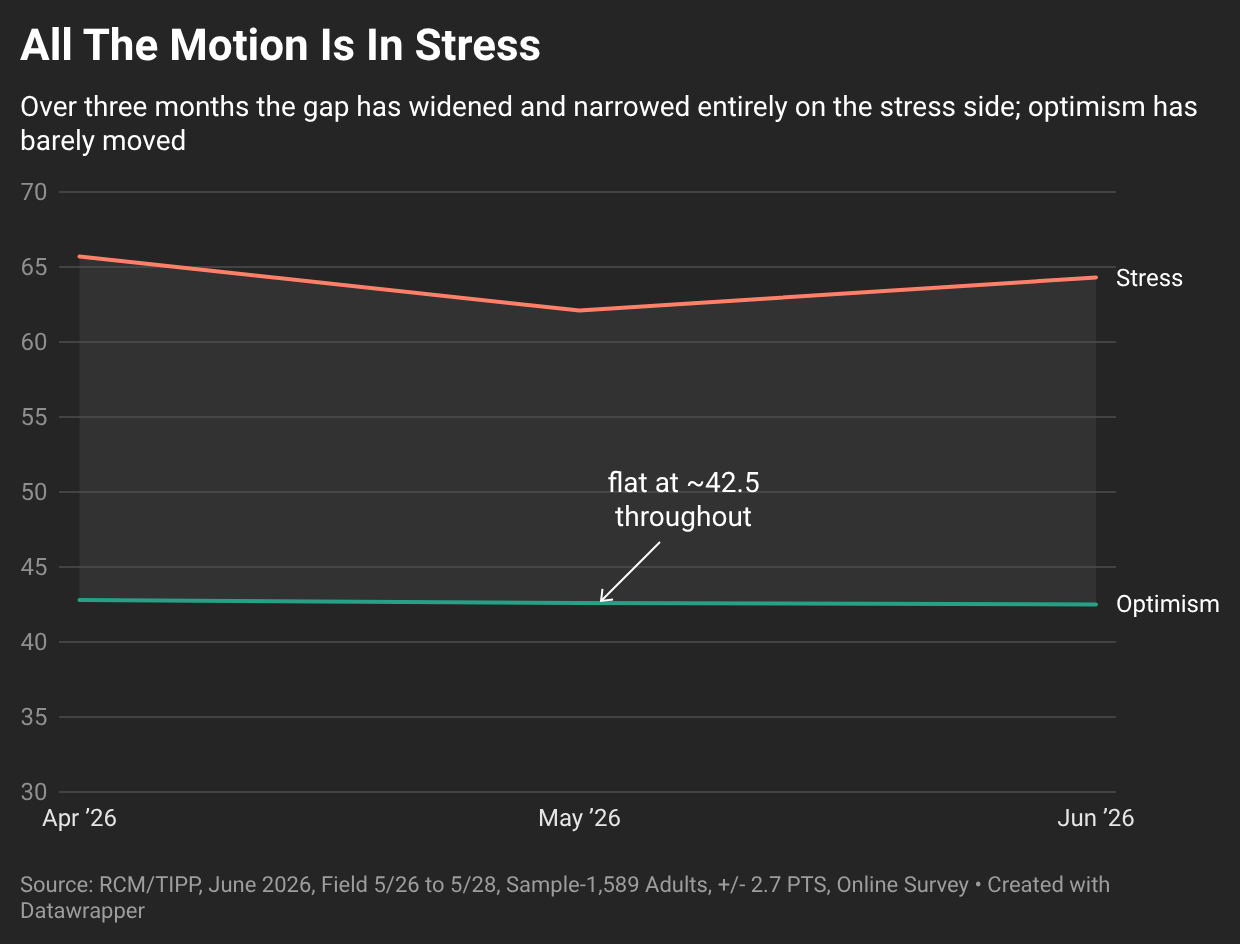

Stress And Optimism, Side By Side

The two gauges moved in opposite directions, but the motion was almost entirely on the stress side. In May, the distance between stress and optimism narrowed to 19.5 points; in June it widened back to 21.8. Both shifts came from stress, which fell hard in May and climbed back in June, while optimism barely moved, holding at 42.8, 42.6, and 42.5 across the three months.

For now, economic confidence appears to be holding at a low level, with no sign yet of a turn in either direction.

RealClearMarkets will release the next report at 10 a.m. EST on Tuesday, July 7, 2026.

The TIPP Off

What you should be reading right now

Global Affairs

Kuwait Airport Shuts Down After Iranian Drone And Missile Attack – TIPP News

Tropical Storm Amanda Forms In Pacific, Poses No Threat To Land – TIPP News

U.N. Researchers Highlight Growing Environmental Cost Of AI Expansion – TIPP News

Congress Quietly Moves To Integrate US And Israeli Militaries – Ben Freeman, Ron Paul Institute for Peace and Prosperity

National Affairs

Why Did NASA Declare The MAVEN Spacecraft Dead – TIPP News

What Led To The 12-Hour Standoff At A Bakersfield Chase Bank – TIPP News

Trump Praises Vance And Rubio As Top Republican Successors – TIPP News

DOJ Charges Newport Beach Executive With Supplying U.S. Equipment To Iran – TIPP News

Trump Backs Todd Blanche For Long-Term Leadership Of Justice Department – TIPP News

House Rebukes Trump With War Powers Vote On Iran Conflict – TIPP News

Trump Administration Targets Americans Opposed To Zionism – Kurt Nimmo, Ron Paul Institute for Peace and Prosperity

Time Is Almost Up On California’s Ticking Medicaid Time Bomb – Nicole Huyer & Christopher Lynch, The Daily Signal

Platner’s Sex Scandal Rocks Maine Senate Campaign – George Caldwell, The Daily Signal

The US Bares Its Fangs Against US Citizens – Jacob G. Hornberger, Ron Paul Institute for Peace and Prosperity

Democrats Are Ditching Karen Bass—And Rallying Behind Spencer Pratt – Angelina Delfin, The Daily Signal

Court Blocks Trump Transgender Military Ban As Driven By ‘Animus’ – Fred Lucas, The Daily Signal

Trump Admin Delivers Major Win Against Government Weaponization – Steve Cortes, TIPP Insights

Michigan Voters Say They’re Sick Of Mass Muslim Migration – Steve Cortes, The Daily Signal

Economy

New Microsoft Quantum Chip Delivers 1,000-Fold Improvement In Stability – TIPP News

Canada Extends Steel And Aluminum Tariff Measures Through 2027 – TIPP News

The Iran War Sounds The Death Knell Of EVs – Editorial Board, Issues & Insights

Trump’s $250 Bill Is Nice. But Reconciliation 3.0 Should Come First. – Robert B. Bluey, The Daily Signal

Theory Explains Data, Not The Other Way Around – Frank Shostak, Mises Wire

Warsh’s Concerning Interest In Redefining “Inflation” – Connor O’Keeffe, Mises Wire

📊 Market Mood — Thursday, June 4, 2026

🟩 Markets remained near record highs as investors balanced strong economic data and continued AI enthusiasm against renewed geopolitical uncertainty in the Middle East.

🟧 Broadcom's results reminded investors how high expectations have become in the AI sector. Revenue surged, but shares fell after guidance failed to deliver the upside many traders had anticipated.

🟦 Fresh diplomatic progress between Israel and Lebanon revived hopes that a broader U.S.-Iran agreement may still be within reach, helping ease some immediate concerns about a prolonged regional conflict.

🟨 Oil prices edged lower, but energy markets remain on alert as disruptions in the Strait of Hormuz continue to keep inflation risks and Fed policy concerns firmly in focus.

🗓️ Key Economic Events — Thursday, June 4, 2026

🟧 8:30 a.m. ET — Initial Jobless Claims

Forecast: 214K vs. 215K previous. Markets will watch for signs that the labor market remains resilient as the Fed weighs inflation risks against the possibility of slower economic growth.

Letters to the editor email: editor-tippinsights@technometrica.com

Subscribe Today And Make A Difference. Consider supporting Independent Journalism by upgrading to a paid subscription or making a donation. Your support helps tippinsights thrive as a reader-supported publication. Contact us to discuss your research or polling needs.

Reach our audience. For sponsorship and advertising opportunities, visit our Partner With Us page.

{kind=link}