Editor's note, July 18, 2026

Three economic reports released this week challenged one of the oldest assumptions in economics: that strong growth inevitably leads to higher inflation. In this special report, Larry Kudlow argues that cooling inflation, resilient consumer spending, rising productivity, and technological innovation may be creating a new version of the "Goldilocks economy"—one in which rapid growth no longer comes at the expense of price stability.

I: Prices Cool, Rate Hikes Fade

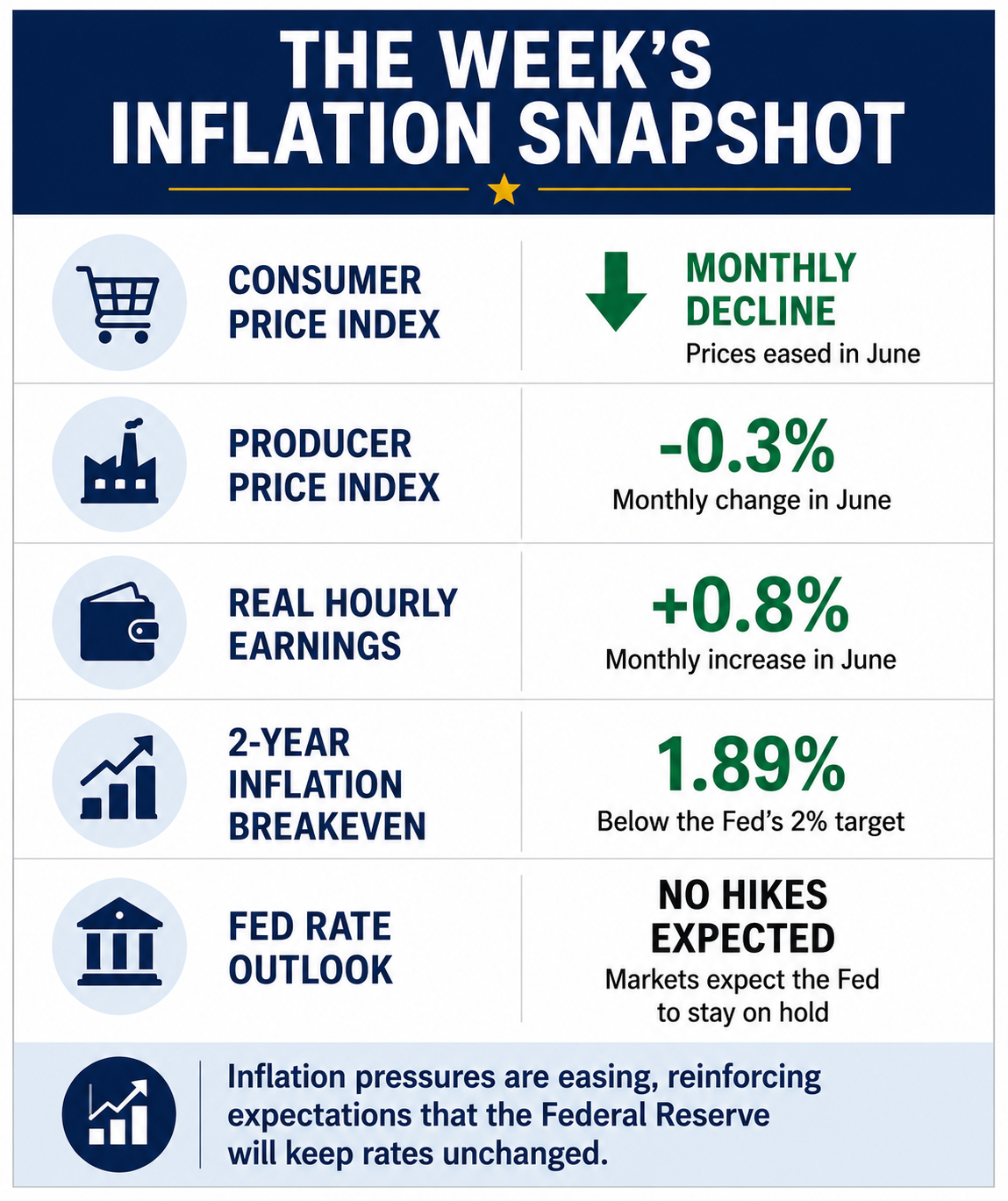

June's consumer and producer price reports surprised Wall Street, eased inflation fears, and strengthened the case that the Federal Reserve will keep interest rates unchanged.

Once again Wall Street was surprised by a deflationary wholesale price report where the level of the so-called producer price index actually dropped by three-tenths of a percent.

And it’s worth noting that after rising 1.1 percent in April, the PPI eased to 0.6 percent in May. And then the outright decline of three-tenths in June.

This follows yesterday’s deflationary CPI report. Both are a welcome relief from the inflationary reports of recent months.

Real average hourly earnings rose 0.8 percent in June. That’s the best monthly real wage gain in 11 years, excluding the pandemic.

Wall Street is also wrong about its prediction that the Fed will be raising rates, as these deflationary reports have taken rate hikes off the board, undoubtedly for the rest of the year I think.

Actually, my view is the Fed’s not going to change their target rates until Chairman Kevin Warsh’s various task forces report.

There are five panels with some very smart people on them. They’re gonna look at the appropriate inflation measures, the Fed’s balance sheet, communication and forward guidance, economic data quality, and productivity.

This is part of Mr. Warsh’s regime change. And it’s a very good idea. Yet my hunch is not to expect any big policy changes until those task forces publish their work, and the central bank figures out how to absorb the reports and then change them.

Meanwhile, even as President Trump steps up the bombing of Iran in response to the IRGC busting the ceasefire and the memorandum of understanding, inflationary expectations in our financial markets are actually coming down.

Indeed even the WTI oil price seems to have stopped rising. I think word money markets want to see regime change in Iran even more than regime change at the Fed.

For the record, the two-year CPI break-evens have dropped all the way to 1.89 percent, that’s below the Fed’s 2 percent target, the dollar is strong, and precious metals are soft.

Meanwhile profits, productivity, and stock prices are all soaring. After the pro-growth incentives of the One, Big, Beautiful Bill of a year ago.

So at least for now, we’ve got falling prices and a rising economy.

Has Goldilocks returned?

💡 TIPP Explains: Why Markets Changed Their Fed View

Earlier this year, investors expected inflation to remain stubborn and force additional Federal Reserve tightening.

This week's CPI and PPI reports altered that outlook.

Lower inflation readings have eased expectations for further rate hikes, while falling market-based inflation expectations suggest investors increasingly believe inflation is returning toward the Fed's target without significantly slowing economic growth.

Lower inflation tells only half the story. The other half is that consumers continue to spend, businesses continue to hire, and productivity appears to be accelerating.

II. Strong Spending Makes The Goldilocks Case

Retail sales, resilient hiring, improving manufacturing, and surging productivity strengthen the argument that the economy is growing rapidly even as inflation cools.

After two great inflation numbers where the level of both consumer and producer prices actually declined in June from the prior month, reported out Tuesday and Wednesday, today we get another big number this time on retail sales — also known as consumer spending.

Core sales have risen 8 percent at an annual rate over the past three months. And the biggest category was online sales, where non-store retailers have jumped by 1.9 percent in June, 1.4 percent in May, 1.5 percent in April, and 21 percent annually for the last 3 months. Those are big numbers.

By the way, car sales are up more than 20 percent annually in the second quarter. Another big number.

We will get manufacturing tomorrow, but two booming regional manufacturing reports from New York and Philadelphia have already been reported.

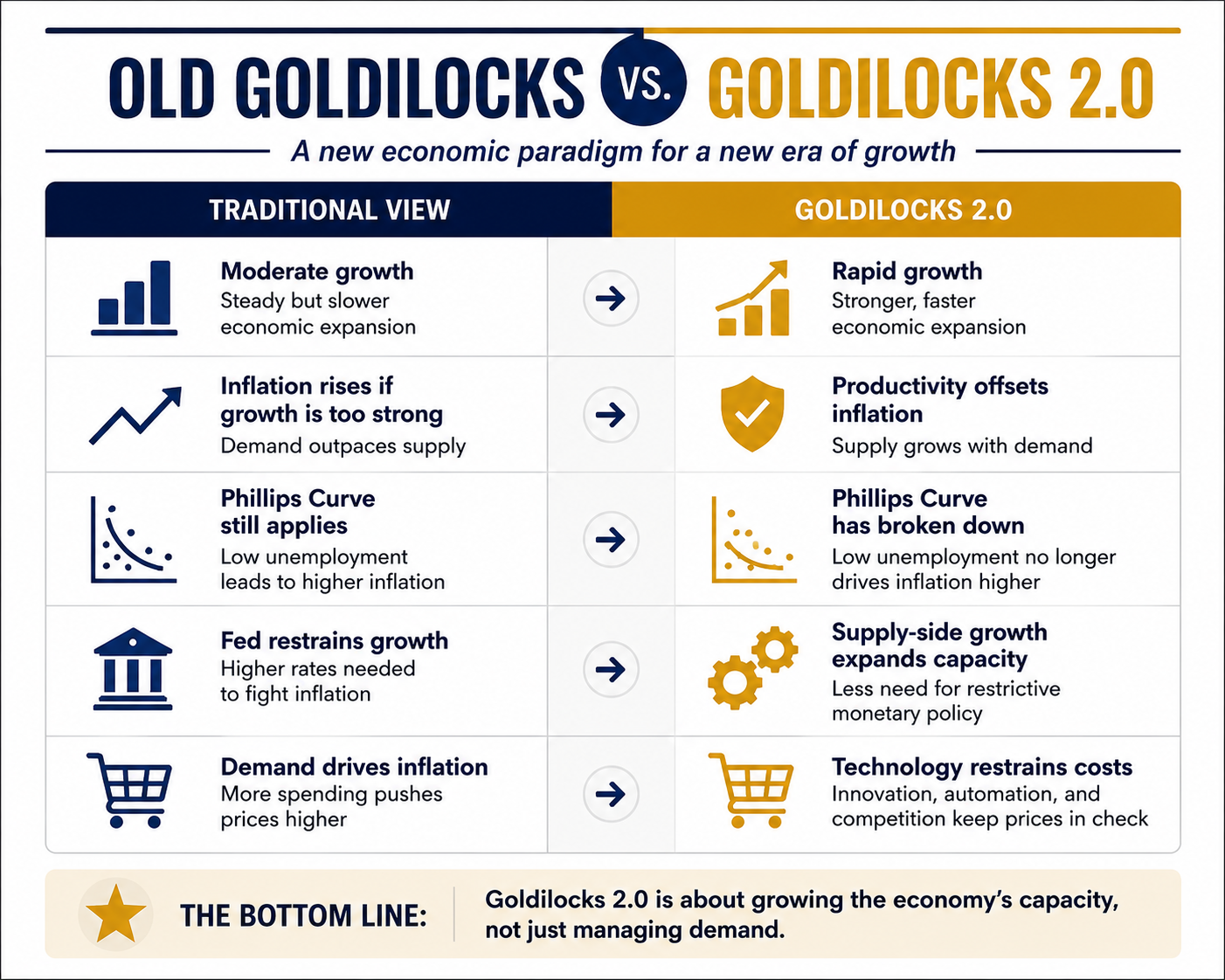

So allow me to modestly redefine the reemergence of a Goldilocks economy. It used to be not too hot and not too cold. Yet that was Wall Street, and I was guilty of it too, suggesting limits to growth that might cause inflation.

My new Goldilocks definition is rapid economic growth combined with stable or even disinflating prices.

That is to say, the Phillips Curve is dead. There’s no trade off between growth and inflation. Or between jobs and inflation.

Speaking of jobs, weekly initial unemployment claims are rock bottom. Nobody is getting fired, but plenty of folks are being hired.

This is a new Goldilocks, on the supply-side, technologically driven. We’re talking AI, quantum computing, advanced manufacturing, and space technology breakthroughs.

At the bottom of all of this is surging productivity — output per person — which is holding down business costs and consumer prices.

We saw some of this movie before during the 1990s. Yet we’re seeing it again right now even bigger time.

And we have pro-growth fiscal and monetary policies, including a strong dollar, and a new regime at the Fed, and lower taxes and fewer regulations from the White House. All this is nurturing the new Goldilocks.

Pessimists beware, you’re about to get whacked and you won’t even see it coming.

💡 TIPP Explains: What Is Goldilocks 2.0?

The phrase "Goldilocks economy" comes from the children's story Goldilocks and the Three Bears, in which Goldilocks chooses the bowl of porridge that is "just right."

For economists, a Goldilocks economy has traditionally meant one that is neither too hot nor too cold—strong enough to create jobs but not so strong that it sparks inflation.

Larry Kudlow argues that definition is evolving.

Rather than slow, moderate growth, today's economy may be capable of sustaining rapid expansion while keeping inflation under control through rising productivity, technological innovation, and expanding productive capacity.

Whether Goldilocks 2.0 proves durable remains an open question. But this week's economic data have strengthened the case that the traditional tradeoff between growth and inflation may be changing. If productivity continues to accelerate while inflation remains subdued, the economy could be entering a period that defies decades of conventional economic thinking.

Lawrence Kudlow is a Fox News Media contributor and host of both “Kudlow” on weekdays and the nationally syndicated “Larry Kudlow Show” each Saturday. This column is adapted from his monologues on “Kudlow.”

🌍 Global Affairs

The world's flashpoints, in motion.

🟥 Iran-U.S. Conflict Escalates With Fresh Overnight Strikes – TIPP News

🟥 7.4 Magnitude Earthquake Triggers Tsunami Warning Off Mexico – TIPP News

🟥 Xi Jinping Calls For Inclusive Global AI Governance – TIPP News

🟥 Iran No Longer Bound By MoU, Adjusts Tactics – Larry C. Johnson, Ron Paul Institute for Peace and Prosperity

🟥 What Happened In The World's First Humanoid Robot Fight – TIPP News

🏛️ National Affairs

The fights shaping America right now.

🟫 The 5 Dumbest Arguments Against The Sunshine Protection Act – Editorial Board, Issues & Insights

🟫 What Is The Reported $10 Million Reward Targeting Trump – TIPP News

🟫 Broadcast Dispute Escalates After Networks Skip Trump's Speech – TIPP News

🟫 ‘YOU COULD HEAR THE SOBS OF A WIDOW’: Inside Charlie Kirk’s Murder Trial – Bradley Devlin, The Daily Signal

🟫 FBI Investigation, Controversial Voter Solicitations, And Trump’s Endorsement Collide In Georgia – Rebecca Buis, The Daily Signal

🟫 Mullin Announces Major Steps for Election Security Following China Revelations – Fred Lucas, The Daily Signal

🟫 ‘We Are Not Defending What Biden Did’: Blanche Answers Hawley On Abortion Pills – Fred Lucas, The Daily Signal

🟫 Trump Endorses Lindsey Graham's Sister For Senate Race – TIPP News

🟫 ‘More Like A Third-World Country’: JD Vance Sounds Off On California With Joe Rogan – Angelina Delfin, The Daily Signal

🟫 The House Speaker’s Refashioned Red Scare – Kurt Nimmo, Ron Paul Institute for Peace and Prosperity

🟫 Virginia’s State Of Surveillance – Rich Tucker, The Daily Signal

🟫 Man Charged With Hate Crimes After NBC Studio Confrontation – TIPP News

🟫 Utah Mall Stabbing Suspect Charged With Attempted Murder – TIPP News

🟫 Trump To Attend FIFA World Cup Final In New Jersey – TIPP News

📈 Economy

Prices, policy, and the pressure on your wallet.

🟩 Trump Threatens Tariffs Over Canadian Wildfire Smoke – TIPP News

🟩 Rothbard’s Definition Of Government As Organized Crime: The Microsoft Antitrust Case – William L. Anderson, Mises Wire

🟩 America’s Gerontocracy Goes Deeper Than Aging Politicians – Connor O'Keeffe, Mises Wire

🟩 The Predatory Logic Of The State – Agustín Toptschij, Mises Wire

🟩 Foucault, Panopticism And The Carceral Society; The Rise Of The Surveillance State – Antony Sammeroff, Mises Wire

🟩 The Vendée: The French War For National Liberation – Ryan McMaken, Mises Wire

💼 Markets & Business

The deals and tickers making moves.

🟧 U.S. Judge Declines To Halt Meta Layoffs Amid AI Bias Lawsuit – TIPP News

Letters to the editor email: editor-tippinsights@technometrica.com

Subscribe Today And Make A Difference. Consider supporting Independent Journalism by upgrading to a paid subscription or making a donation. Your support helps tippinsights thrive as a reader-supported publication. Contact us to discuss your research or polling needs.

Reach our audience. For sponsorship and advertising opportunities, visit our Partner With Us page.

{kind=link}