Last month, the RealClearMarkets/TIPP survey was the first to offer a grounded reading: Consumer confidence softened, but panic was absent. In the weeks that followed, other surveys caught up to what we had already reported.

This month, consumer sentiment showed meaningful improvement, edging closer to the neutral 50.0 threshold. The RealClearMarkets/TIPP Economic Optimism Index, a key gauge of consumer sentiment, climbed from 47.9 in May to 49.2 in June, representing a 2.7% increase.

After hitting a 40-month high of 54.0 in December, the Index eased to 51.9 in January and 52.0 in February before falling below the 50.0 threshold in March. June's reading of 49.2 marks the fourth consecutive month in the pessimistic zone. After President Trump’s re-election in November 2024, the Index remained optimistic until February.

Coincidentally, June’s reading matches its 293-month historical average of 49.2.

The RCM/TIPP Economic Optimism Index is the first monthly measure of consumer confidence. It has established a strong track record of foreshadowing the confidence indicators issued later each month by the University of Michigan and The Conference Board. (From February 2001 to October 2023, TIPP released this Index monthly in collaboration with its former sponsor and media partner, Investor's Business Daily.)

RCM/TIPP surveyed 1,395 adults for the June Index from May 28 to May 30. The online survey used TIPP's network of panels to obtain the sample. A more detailed methodology is available here. The Index ranges from 0 to 100. Readings above 50 indicate optimism, while those below 50 signal pessimism. A score of 50 is neutral.

RCM/TIPP Economic Optimism Index

The RCM/TIPP Economic Optimism Index has three key components. In June, all of them improved.

- The Six-Month Economic Outlook, which measures how consumers perceive the economy's prospects in the next six months, gained 3.4%, from 43.6 in May to 45.1 in June.

- The Personal Financial Outlook, a measure of how Americans feel about their own finances in the next six months, improved by 2.5% from its previous reading of 52.5 in May to 53.8 this month.

- Confidence in Federal Economic Policies, a proprietary RCM/TIPP measure of views on the effectiveness of government economic policies, rose from 47.6 in May to 48.6 this month, reflecting a 2.1% gain. This component has been below 50.0 (pessimistic territory) for 46 consecutive months since September 2021.

Party Dynamics

With President Trump's election as the 47th President, Democrats' confidence tumbled from 62.9 in October to 43.2 in November. However, it increased in December to 47.6. It dropped again in January to 45.7. It further declined to 37.5 in February and 32.3 in March. In April, it increased a notch to 32.6, posted 32.4 in May, and settled at 33.1 in June.

Meanwhile, Republican confidence surged from 34.8 in October to 64.7 in November. It held steady at 66.4 in December, dipped slightly to 63.0 in January, then rebounded to 69.0 in February and 70.9 in March. However, it edged down to 70.6 in April and declined more noticeably to 68.6 in May. It edged up to 68.8 in June.

In November, independent voters' confidence jumped 8.6 points, or 20%, to 51.3, the Index’s first positive reading in nearly five years. The independents had remained in pessimistic territory for 56 consecutive months, starting in April 2020 following the pandemic’s onset. However, confidence fell to 44.1 in December and remained relatively flat in January (45.3) and February (47.0). It then dropped sharply to 43.8 in March, with the decline continuing in April (40.0) and May (39.6). It improved slightly in June to 42.1.

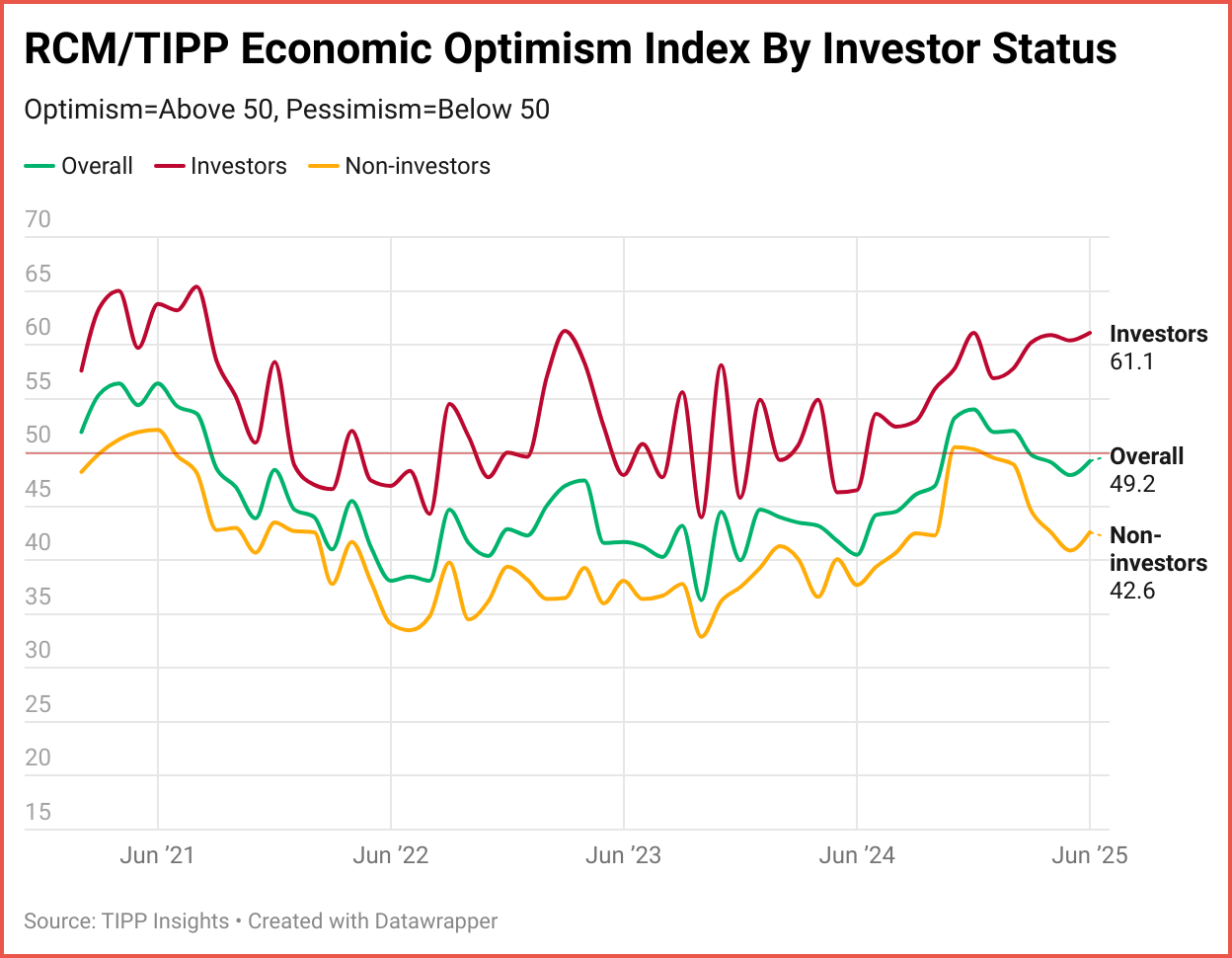

Investor Confidence

Respondents are considered "investors" if they currently have at least $10,000 invested in the stock market, either personally or jointly with a spouse, either directly or through a retirement plan. One-third (35%) of respondents met this criterion, and 60% were classified as non-investors. We were unable to determine the status of five percent of respondents.

Investors’ confidence gained 1.2% (0.7 points) to 61.1, while non-investor confidence improved by 1.7 points (4.2%) to 42.6.

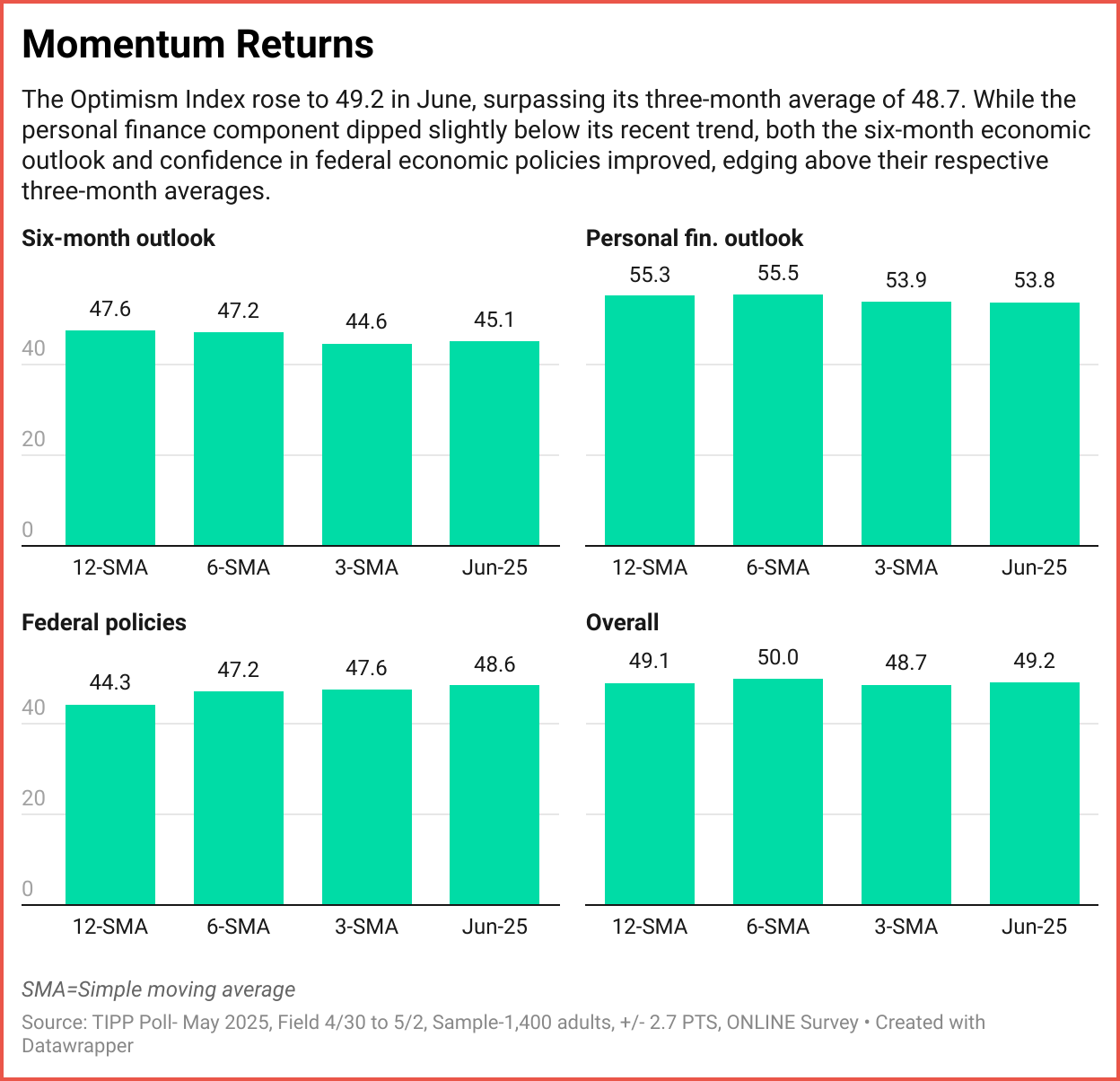

Momentum

Comparing a measure's short-term average to its long-term average helps gauge its momentum. If the 3-month average exceeds the 6-month average or the 6-month average exceeds the 12-month average, momentum is considered positive.

In June, momentum was mixed. The Six-Month Outlook rose to 45.1, slightly above its three-month average of 44.6, indicating modest positive momentum. The Personal Financial Outlook slipped to 53.8, just below its three-month average of 53.9, suggesting a minor loss of momentum. Meanwhile, confidence in Federal Economic Policies strengthened, climbing to 48.6 and exceeding its three-month (47.6) and six-month (47.2) averages—signaling upward momentum. The Overall Optimism Index increased to 49.2, surpassing its three-month average of 48.7, confirming a positive trend.

Demographic Analysis

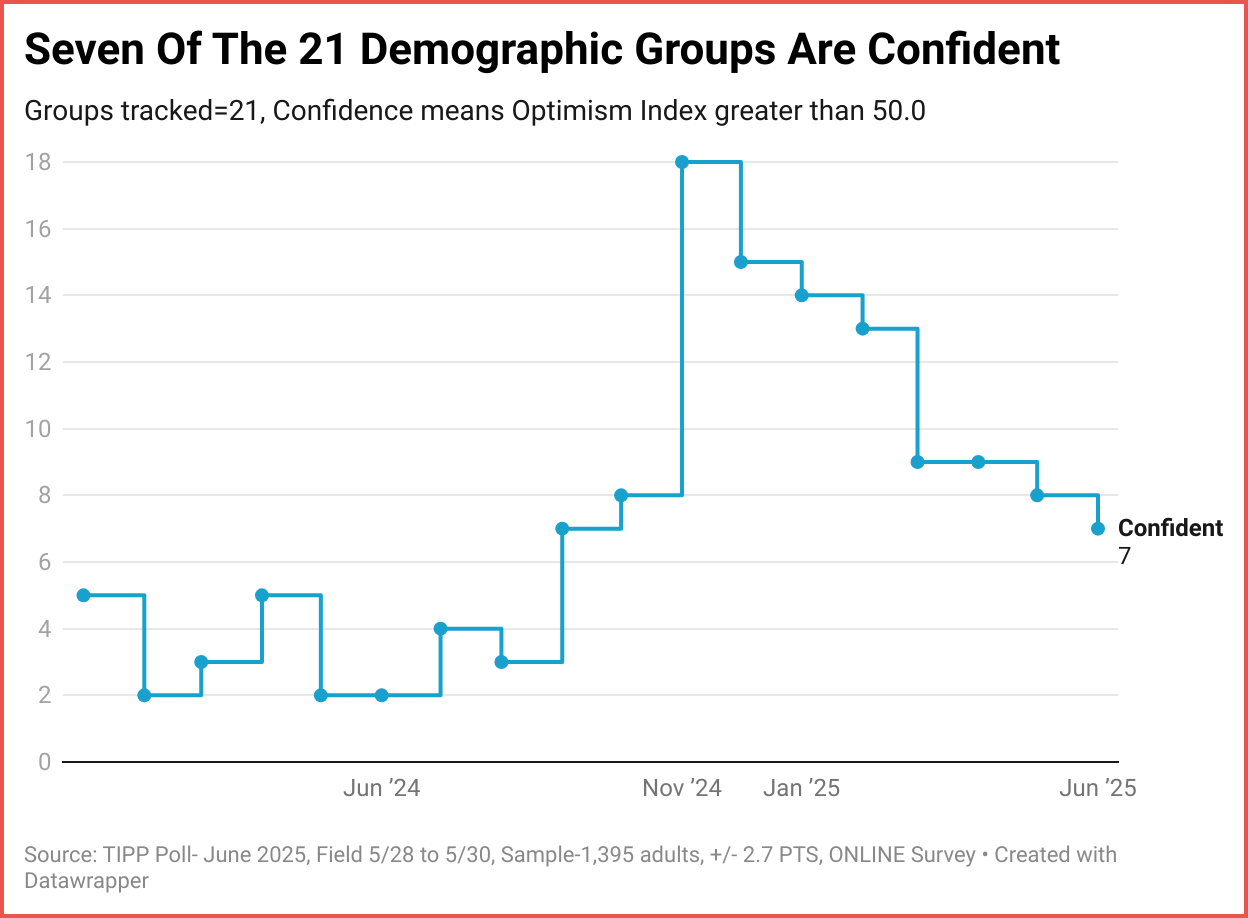

The number of groups in the positive zone indicates the breadth of optimism in American society.

This month, seven of the 21 demographic groups we track are in positive territory, with scores above 50 on the Economic Optimism Index. For comparison, there were eight in May, nine in April, and nine in March.

In the immediate aftermath of the election, the number of groups in the optimistic zone had jumped from eight in October to 18 in November, indicating widespread optimism.

Eighteen groups improved on the Index, compared to five in May, nine in April, and five in March.

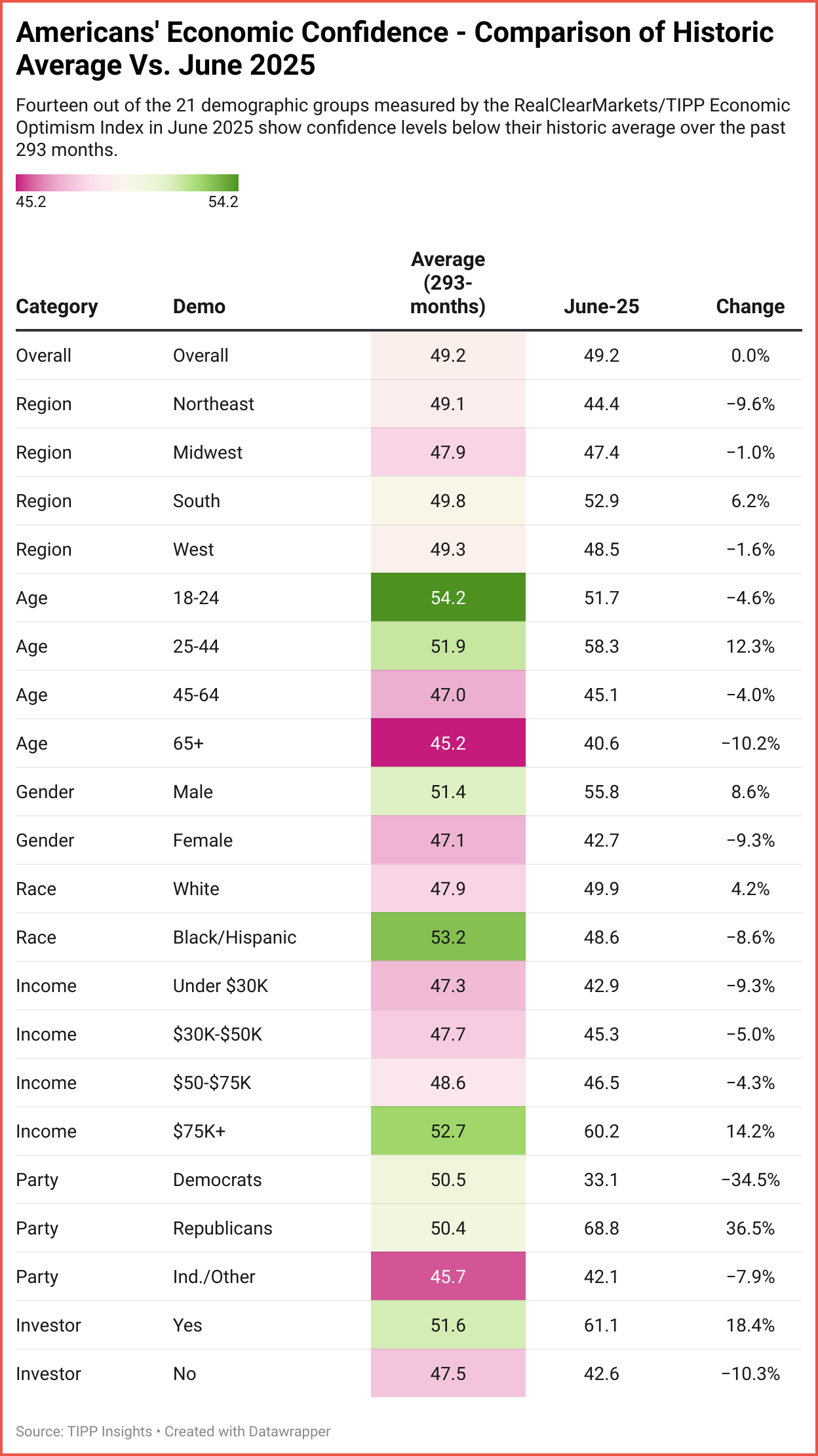

Economic optimism levels for 14 of 21 demographic groups are lower in June 2025 than the historical average of the past 293 months, since we began tracking in February 2001.

RCM/TIPP Financial-Related Stress Index

RCM/TIPP also releases our companion index, known as the RCM/TIPP Financial-Related Stress Index, the only metric to track the financial stress felt by Americans monthly.

The higher the number, the more stress. Readings above 50 signal increased stress, while those below 50 indicate lower stress, with 50 considered neutral.

The Index declined 3.7 points (5.5%) from 66.7 in May to 63.0 in June, echoing the easing of financial stress among Americans.

For context, the last time the Index posted below 50.0 was before the onset of the pandemic in February 2020, when it stood at 48.1.

The Index has averaged 60.4 since December 2007. June’s reading of 63.0 exceeds this by 4.4%, signaling heightened financial stress relative to the long-term average.

Inflation

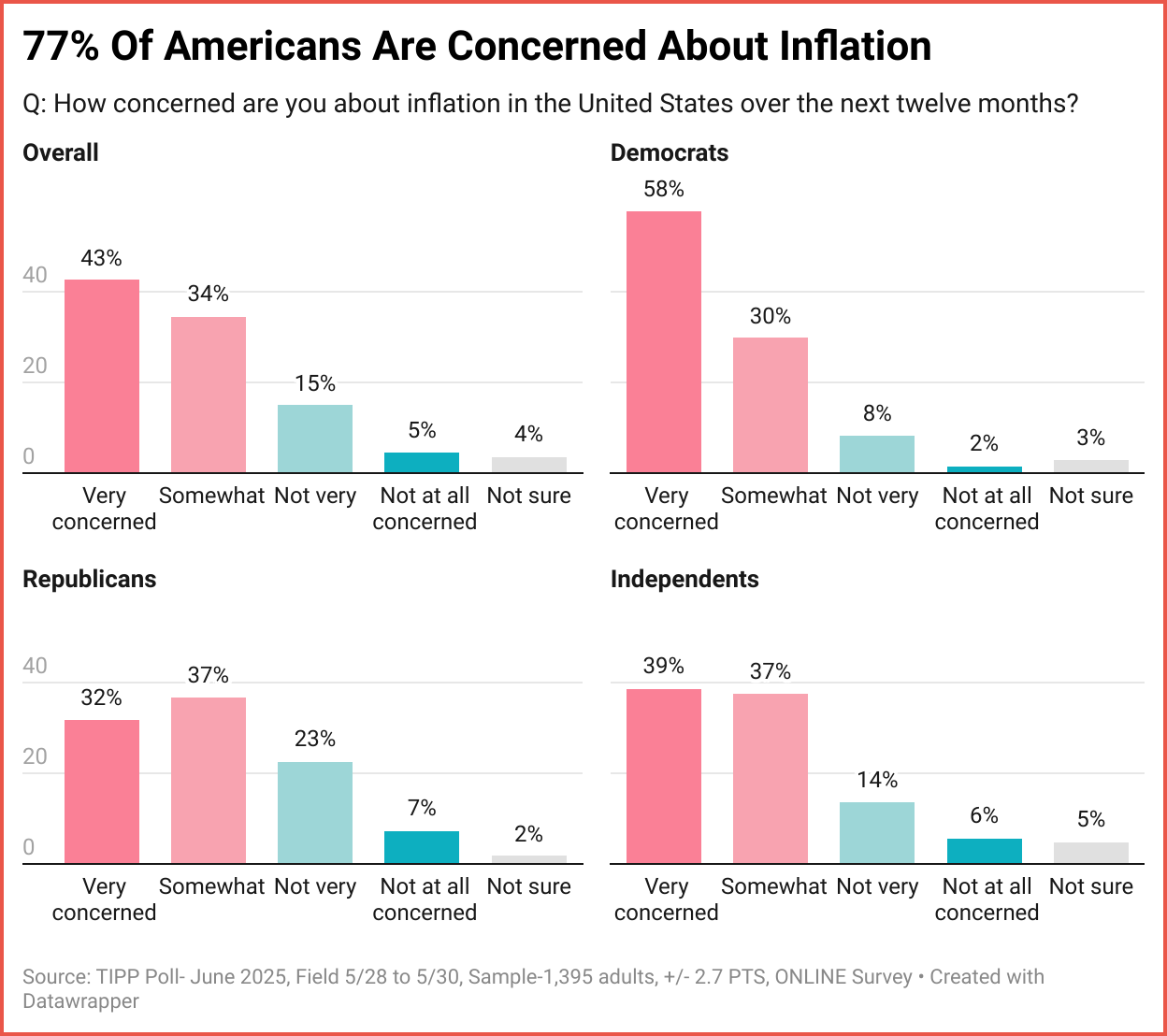

The survey showed that 77% are worried about inflation: 43% are very concerned, and another 34% are somewhat concerned.

Americans continue to suffer because real wages have not increased, despite the CPI rate falling from a 40-year high of 9.1% in June 2022 to 2.3% in April 2025.

The Federal Reserve believes that long-run inflation of 2%, measured by the annual change in the price index for personal consumption expenditures, is most consistent with its maximum employment and price stability mandate.

According to the USDA, the price of eggs has dropped more than 61% since President Donald Trump took office in January, from $6.49 per dozen to $2.52.

Recession

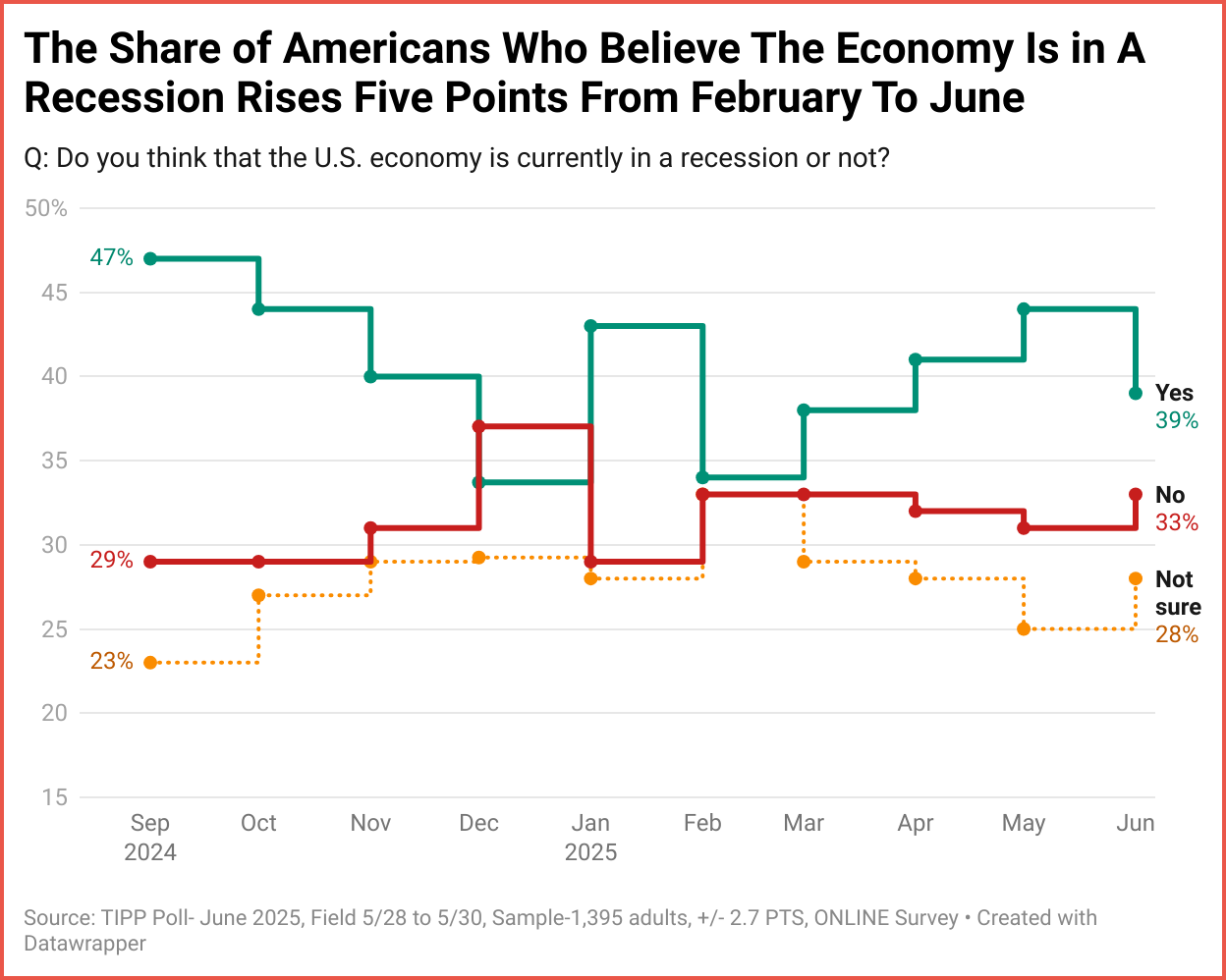

Nearly four-in-ten (39%) believe the United States is in a recession, while 33% think it is not. Another quarter (28%) is not sure.

Inflation is down, and incomes are up. That’s a strong result for President Trump, especially after the media ran dozens of stories predicting a recession this year.

The Atlanta Fed’s GDPNow model, which tracks real-time economic data, now projects 3.8% growth for the second quarter.

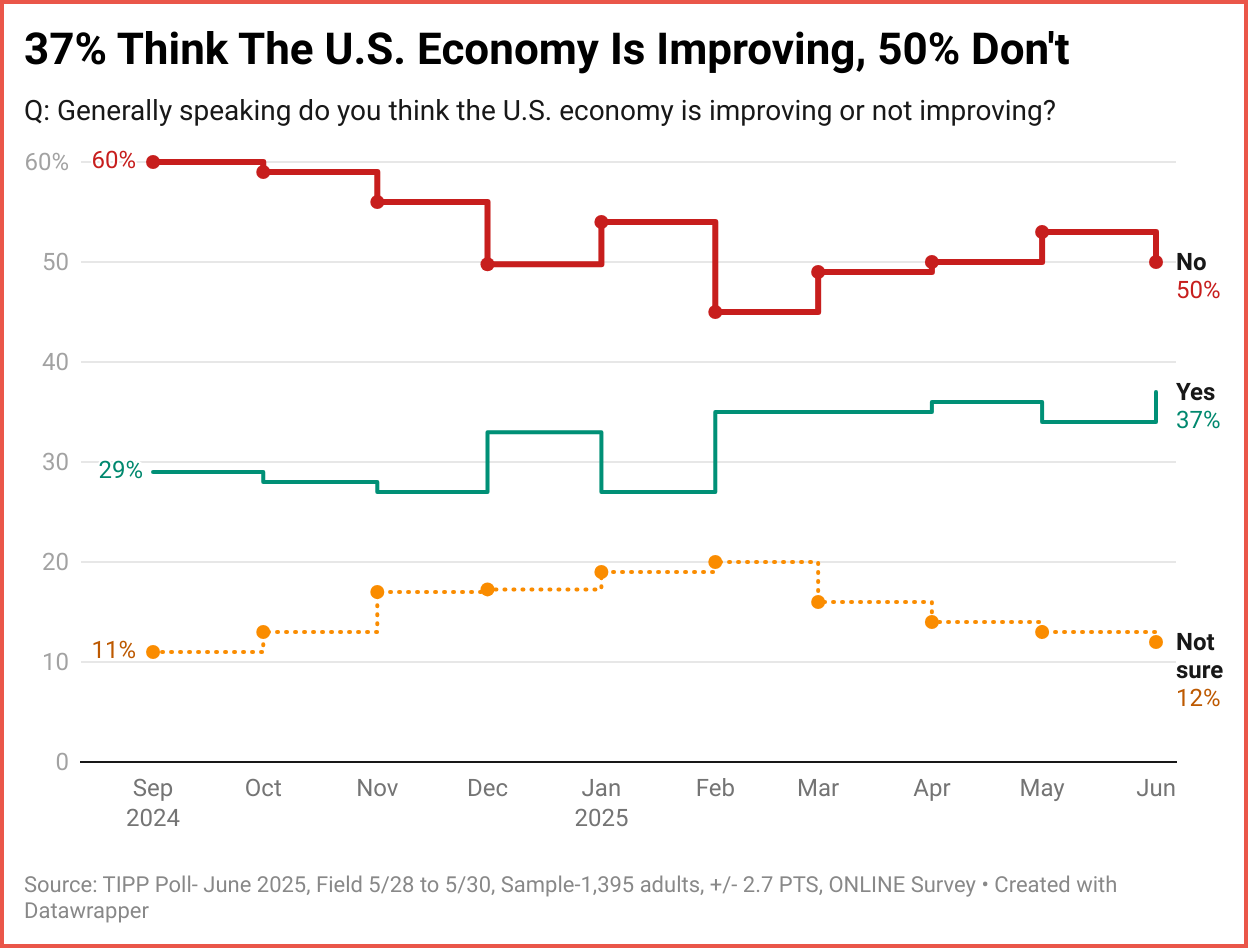

Meanwhile, one-half (50%) think the U.S. economy is not improving, while 37% believe it is improving. The percentage of Americans with a positive view increased from 27% in November to 37% in June.

John Tamny, the editor of RealClearMarkets, observed:

To export is to import. No economic school of thought can get around the previous truth. Which is why it's not too surprising that a pause on mindless tariffs (that would greatly hinder U.S. exports if implemented) has coincided with rising confidence. Producers are consumers, by definition. Which is why the only good tariff is no tariff. May the Trump administration recognize this universal truth and, in recognizing it, set the stage for Americans to flourish as best they can.

Release Schedule Of RCM/TIPP Indexes For the Rest Of 2025

The RealClearMarkets website releases the report at 10 a.m. EST on the release days.

- Jul 25: Tuesday, July 1

- Aug 25: Tuesday, August 5

- Sep 25: Tuesday, September 2

- Oct 25: Tuesday, October 7

- Nov 25: Tuesday, November 4

- Dec 25: Tuesday, December 2

Your feedback is incredibly valuable to us. Could you please take a moment to grade the article here.

TIPP Picks

Selected articles from tippinsights.com and more

1. The Trump Doctrine—Richard Haass, Project Syndicate

2. What The World Needs Now From Pope Leo XIV—Ryan McMaken, Mises Wire

3. Trump’s Ratings Edge Higher As Good News Eclipses Negative Media Coverage: I&I/TIPP Poll—Terry Jones, TIPP Insights

4. A Golden Share Will Not Make America Great Again—Ron Paul, The Ron Paul Institute for Peace and Prosperity

5. Putin Tells Trump Russia Will Strike Back Over Ukraine Drone Attacks—TIPP Staff, TIPP Insights

6. Trump Calls Fed Chair ‘Unbelievable’ After May Job Slump—TIPP Staff, TIPP Insights

7. Harvard Hits Rock Bottom—Carrie Sheffield, The Daily Signal

8. Putting Israel First, Rubio Victimizes Harmless Student Over Op-Ed—Brian McGlinchey, The Ron Paul Institute for Peace and Prosperity

9. Seattle’s Other Monorail: Some Lessons for California—Jane L. Johnson, Mises Wire

10. What Is The Optimal Growth Rate For The Money Supply?—Frank Shostak, Mises Wire

11. Illinois Dems Lay Budget Woes At Trump’s Feet After Taxing Their Citizens Into Ground—Melissa O'Rourke, DCNF

12. US Attorney Claps Back At Boston Mayor For ‘Inflammatory Statements’ Made Against Immigration Agents—Virginia Allen, The Daily Signal

13. Middle East Leaders Surprisingly Fine With Iran Enriching Uranium, Lankford Says—Tyler O'Neil, The Daily Signal

14. Speaker Johnson, Marjorie Taylor Greene At Loggerheads On Artificial Intelligence Regulation—George Caldwell, The Daily Signal

15. Israeli Mossad Named As Funder Of Gaza Humanitarian Foundation—Max Blumenthal, The Ron Paul Institute for Peace and Prosperity

16. Musk Doubles Down On Budget Bill: 'Kill The Bill'—TIPP Staff, TIPP Insights

17. Karine Jean-Pierre Turns Independent, Leaves Democratic Party—TIPP Staff, TIPP Insights

18. China Backs Pakistan-Afghanistan Move To Restore Diplomatic Ties—TIPP Staff, TIPP Insights

19. Trump Calls Xi 'Tough' Ahead Of The Phone Call With Beijing—TIPP Staff, TIPP Insights

20. Ukraine Says Ceasefire Ready, Russia Refuses To Engage—TIPP Staff, TIPP Insights

21. Miller Hits Back: Trump Budget Cuts $1.6 Trillion, Not Adds It—TIPP Staff, TIPP Insights

22. Republicans Say Musk’s Attacks On Budget Bill Are Self-Serving—TIPP Staff, TIPP Insights

23. Colorado Suspect’s Family Detained By U.S. Immigration Authorities—TIPP Staff, TIPP Insights

TIPP Market Brief – June 5, 2025

Your Morning Snapshot

📊 Market Snapshot

- S&P 500: ▲ 5,970.81 (0.01% )

- 10-Year Yield: ▼ 4.365%, (9.5 basis points)

- Crude Oil (WTI): ▼ $62.74 (1.06%)

- Bitcoin (BTC): ▼ $104,697.16

- US Dollar Index (USD): ▼ 98.82 (0.41%)

- Gold: ▲ $3,374.04 (0.61%)

Bigger Charts: $SPX | $TNX | $WTIC | $BTCUSD | $USD | $GOLD

📈 Featured Stock

Our pick for today’s featured stock

📰 News & Headlines

Jim Cramer on Aeva Technologies (AEVA): Its Recent "Airbus Contract That's Really Good"—Syeda Seirut Javed, Insider Monkey

AEVA's 4D LiDAR Solution Targets GPS-Free Navigation Needs—Nilanjan Choudhury, Zacks

⭐Recent Featured Stocks

Zscaler, Inc. (ZS) (6/4)

NRG Energy (NRG) (6/3)

Life360, Inc. (LIF) (6/2)

GE Aerospace (GE) (5/30)

Robinhood Markets, Inc. (HOOD) (5/29)

Carvana Company (CVNA) (5/28)

Hims & Hers Health, Inc. (HIMS) (5/27)

Roblox Corp (RBLX) (5/23)

Rubrik, Inc. (RBRK) (5/22)

Oddity Tech Ltd. (ODD) (5/21)

More here

🧠 Macro Insight

- → Futures flat as markets weigh Trump’s tariffs, soft U.S. data, and key jobs and inflation signals.

- ECB expected to cut rates, but debate grows over shifting to a neutral stance as eurozone inflation cools.

- U.S. jobless claims ahead, with eyes on labor market softness before Friday’s payrolls report.

- Broadcom (AVGO) will report earnings, offering a pulse check on AI chip demand and cloud spending.

- ▲ Oil rebounds slightly, but big gasoline and distillate builds raise summer demand concerns.

📅 Key Events Today

Thursday, June 5

● 08:30 AM ET – Initial Jobless Claims

Weekly read on unemployment claims and labor market stress.

{kind=link}