Second in the China in Decline series, a running examination of the structural strains beneath China's slowing economy. Part One, "The Pig Doesn't Lie," traced the same loss of confidence through the collapse in pork prices.

Earlier this year, the headlines finally turned hopeful. New-home prices in China’s biggest cities ticked up for the first time in ten months, and Beijing let the world know the corner had been turned. The analysts who watch the numbers were not convinced; one called it premature to read any of it as a genuine recovery.

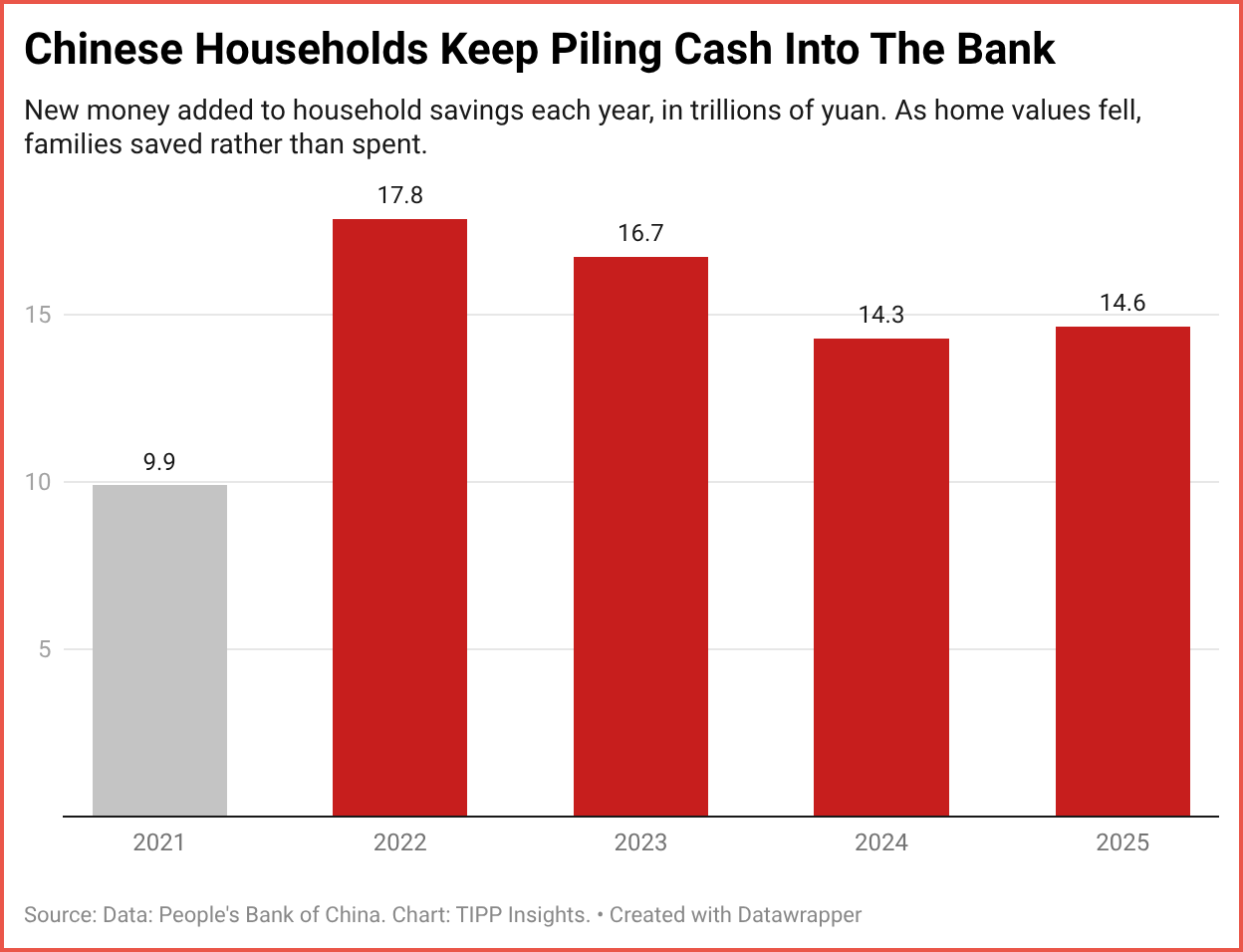

The Chen family would agree. They did everything the Party told them was safe. For fifteen years they saved, and they poured all of it into a single apartment on the edge of a Chinese city, because a home was the one thing that was supposed to never lose its value. Today, that apartment is worth about a fifth less than they paid for it, and it is still sliding. So they have stopped spending. Multiply the Chens by three hundred million households, and that is the real Chinese economy of 2026, the one beneath the recovery headlines. Beijing says the worst is over. The one man who could make it true has decided not to.

Nearly 70 percent of a Chinese household’s wealth is tied up in its home, unlike in the United States or Japan, where housing typically accounts for about a quarter of household wealth. The household has no pension system to fall back on, no reliable insurance against illness or unemployment, and no stock market it trusts. The home is the household’s savings account, retirement plan, and emergency fund.

Every home also feeds a long chain of industries. To build it takes concrete, steel, and glass, and people to design, finance, and construct it. Then come the roads, power lines, and water pipes that connect it, and after the keys change hands, the furniture and appliances that fill it. Add all of that to the apartments themselves, and real estate accounts for nearly a third of China’s economy. When housing sinks, it does not sink alone.

Rewind to August 2020. Beijing looked at the giant developers building those apartments and saw companies surviving on borrowed money, paying yesterday’s debts with tomorrow’s loans, much like a man covering one credit card bill with another. The debt pile had grown too large to ignore. So the government drew three red lines and imposed limits on how much a developer could borrow against its assets, its equity, and the cash it actually held. The more lines a developer crossed, the less it could borrow. It was a deliberate attempt to puncture a property bubble and, on its own terms, a sensible one.

Sixteen months later, the rules caught up with China’s biggest real estate developer. In December 2021, Evergrande, a company with more than $300 billion in liabilities, could no longer borrow to cover its obligations and defaulted. By early 2024, a Hong Kong court ordered the company into liquidation. Evergrande became the face of China’s property collapse, its unfinished towers and shuttered sales offices filling front pages around the world.

Research by Kenneth Rogoff, a former chief economist of the International Monetary Fund, and the IMF economist Yuanchen Yang showed that real estate’s contribution to China’s growth had been declining since 2018. The cause was a growing mismatch: too many apartments going up in too many cities whose populations were already shrinking. The property bust was already in the making. The new rules were only the trigger.

Rogoff and Yang went looking for a precedent and found Japan. When Japan’s property bubble burst in the early 1990s, home prices eventually fell by about 60 percent from their peak, and the adjustment took the better part of a decade to run its course. China’s official figures show a much milder decline so far, roughly 20 percent, though private realtor data suggest the true drop is considerably steeper. China is now in the sixth year of its own correction, and aging even faster than Japan did, with fewer young buyers to absorb the glut. The authors are careful: if China follows Japan’s path, they write, it has not yet reached the halfway point. Beijing is selling a recovery that the data has yet to show.

Here is the trap. When a family’s home loses value and little else stands behind it, the family does not spend its way back to confidence. It cuts spending and saves even harder, trying to rebuild the cushion the falling house has erased. Now imagine that happening on every street at once. Consumers spend less, so shops and restaurants earn less. Businesses respond by hiring fewer workers or paying them less, leaving families feeling poorer still and pulling back even further. Weaker demand then pushes the price of the next apartment lower, and the cycle begins again. Each turn of the cycle deepens the next.

This is the loop Xi’s stimulus tools keep missing. The obvious response, when people stop spending, is to encourage them to spend again. But waving a small voucher at a family that has just watched a fifth of its only nest egg disappear is unlikely to change its behavior. The voucher pulls toward spending. The fear of further losses pulls the other way, and the fear wins every time. Every yuan aimed at consumption is pushing against the much larger force of falling home values. The very lever needed to drag the economy out of its slump is consumer spending, yet it is the one that sinking home prices keep pinned down.

The same falling prices also drain the state. For years, local governments funded themselves by selling land to developers, and developers have stopped buying. That revenue has fallen for four straight years, sliding to 4.9 trillion yuan in 2024, down 44 percent from its 2021 peak, with a further drop of nearly 15 percent in 2025. The towns that once mopped up surpluses and paid for local services are now broke. Readers of the first piece in this series will recognize the symptom: this is the same cash-strapped local state that could not absorb the pork glut when prices crashed. The property bust and the cheap pig are two windows into one stalled economy.

The way out is well known, and Xi almost certainly understands it. The government would have to stand behind families directly: cash in hand, plus a real pension system, health coverage, and unemployment insurance. Then a falling home would no longer be the only thing between a household and ruin. The economists who diagnosed the trap put it plainly. Without a safety net, families treat their home as their last line of defense, so when its value falls, they hoard whatever they can rather than spend.

Economists estimate that the housing downturn could drain 2 to 4 percent of China’s annual economic output from consumer spending. What Xi offers households instead is revealing: consumption vouchers worth less than 10 billion yuan and trade-in subsidies of about 150 billion yuan. Those measures are a trickle against a problem of such magnitude. The money to break the cycle exists. What is missing is the willingness to put it directly into households' hands.

Xi has long warned against what he calls “welfarism,” arguing that giving people money breeds idleness and dependency. By that logic, helping homeowners directly is no different from subsidizing consumers to spend more. Both require the state to step in on behalf of households, and he has been unwilling to take that step.

Yet he treats the wrong patient, cutting interest rates so developers can borrow again and nudging state-owned firms to buy unsold apartment towers. He keeps the cranes moving and the construction machine alive, then waits for families to regain confidence on their own. But confidence is not something the government can summon by decree. It returns only when fear recedes, and he has done nothing to remove that fear. He is waiting for an outcome he has refused to create.

Xi’s failure was not the crash but his answer to it. A leader who could have lifted the families crushed beneath the collapse chose instead to shore up the developers and call the rubble a recovery.

📉 THE CHINA FILES · June 13, 2026

Xi's China is contracting at home and overreaching abroad. The TIPP editorial board tracks the decline, one front at a time.

THE SUMMIT THEATER

🔹 Mr. President, Don't Go to China: Beijing is funding a regime that is killing American troops. A state visit now rewards the patron.

🔹 The Handshake in Beijing: The summit is just a photograph, unless Trump forces Xi to move on Iran.

🔹 The 25th Visit: The price column is still blank.

🔹 To Be Continued: Trump asked Xi for the only thing that mattered. Xi said no.

🔹 Xi's Reelection Theater: Every concession since Busan was for one photograph. The photograph was for his fourth term.

BANKROLLING THE AXIS

🔹 The Quartermaster: The drone that downed an American helicopter is Iranian. Its supply chain is not.

🔹 The Denuclearization Surrender: China's demand that North Korea disarm was also its leverage. Xi gave up both, just as Kim turns to confront Washington.

TAIWAN AND A HOLLOW ARMY

🔹 The Boxed-In Giant: On the map that decides a war over Taiwan, China is the trapped one, and Xi tightened the trap himself.

🔹 Xi's Question: Taiwan?

🔹 Ambiguity Top and Bottom: Xi asked whether America would defend Taiwan. The President preserves the ambiguity by design; the public, by indecision.

🔹 The Death Sentence: Xi is purging the men he handpicked. The army he is left with cannot fight the war he keeps threatening.

🔹 One Child, One Soldier: The demographic curse haunting Xi.

THE JAPAN MISFIRE

🔹 The Home Front: Xi staged a year of pressure on Japan for an audience at home, and lost the one abroad.

🔹 The Backfire: A year of Chinese pressure left Japan's new prime minister stronger than it found her.

THE PENETRATION OF AMERICA

🔹 The American Kill Line: The viral Chinese meme that explains everything wrong with Beijing's reading of America.

🔹 Inside the Wire: Americans want China out of the land, the supply chain, and the phone. The agreement is broad, and it is defensive.

CHINA IN DECLINE

🔹 The Pig Doesn't Lie: The pig the Party once promised would stay cheap now costs more to raise than it sells for.

👉 The full China dossier, with new dispatches as the story breaks. Subscribe to TIPP Insights →

Letters to the editor email: editor-tippinsights@technometrica.com

Subscribe Today And Make A Difference. Consider supporting Independent Journalism by upgrading to a paid subscription or making a donation. Your support helps tippinsights thrive as a reader-supported publication. Contact us to discuss your research or polling needs.

Reach our audience. For sponsorship and advertising opportunities, visit our Partner With Us page.

{kind=link}